Business Recovery Post-COVID: Small Real Estate Concerns by SCB EIC

The COVID-19 crisis over the past three years has significantly impacted the Thai economy, particularly the business sector. Many companies faced challenges, leading to a substantial number of job losses and an increase in Thailand's unemployment rate from an average of around 1% before the pandemic to a peak of 2.3% in the third quarter of 2021.

Although the overall situation of COVID-19 is beginning to improve, the recovery of the business sector is still gradual and uneven. Businesses that align with consumer recovery or global trends are recovering faster, while some sectors remain at risk and are recovering slowly due to the global economic slowdown this year or changing mega trends. Small and medium-sized enterprises (SMEs) are likely to be more heavily impacted than larger businesses, indicating a slower recovery and a continued need for government assistance.

According to the SCB Economic and Business Research Center (SCB EIC), an analysis of the overall business recovery trends has been conducted to provide recommendations for business adaptation and appropriate public policy implications moving forward.

Overview of the Impact of the COVID Crisis on the Business Sector

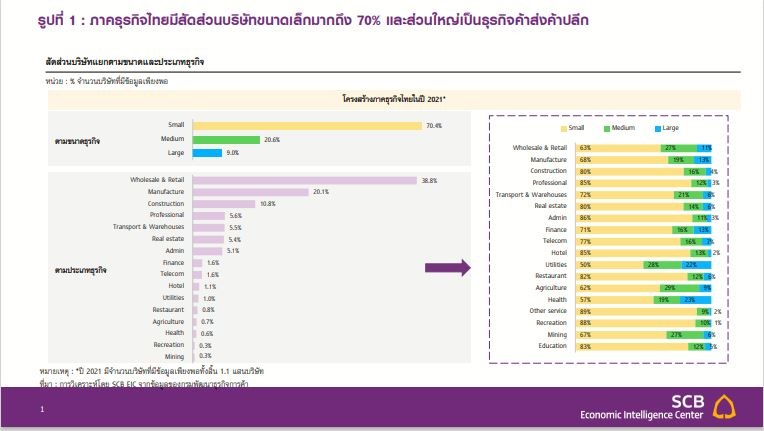

For this study, SCB EIC utilized data from registered companies in Thailand from the Department of Business Development, based on financial reports from 2017 to 2021. Approximately 110,000 companies with sufficient data throughout the study period were included, with very small businesses accounting for 70.4%, and the majority being wholesale and retail businesses, comprising 38.8% of the total sample.

The impact on the business sector was assessed in two dimensions: profitability and liquidity changes during the COVID crisis through financial data.

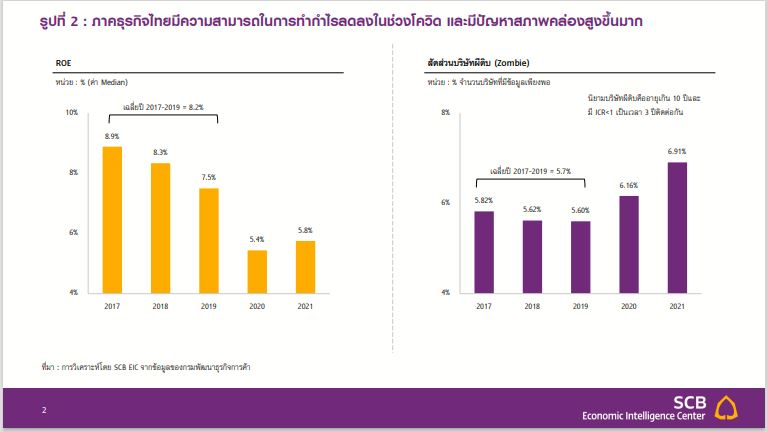

Analysis results indicated that the median ROE of the sampled companies decreased from an average of 8.2% during the three years before the pandemic (2017-2019) to a low of 5.4% in 2020, before slightly improving to 5.8% in 2021. Meanwhile, the proportion of zombie firms increased to around 7% from a pre-COVID average of 5.7%, reflecting the overall business sector's significant impact on both profitability and liquidity, which has not yet returned to pre-pandemic levels.

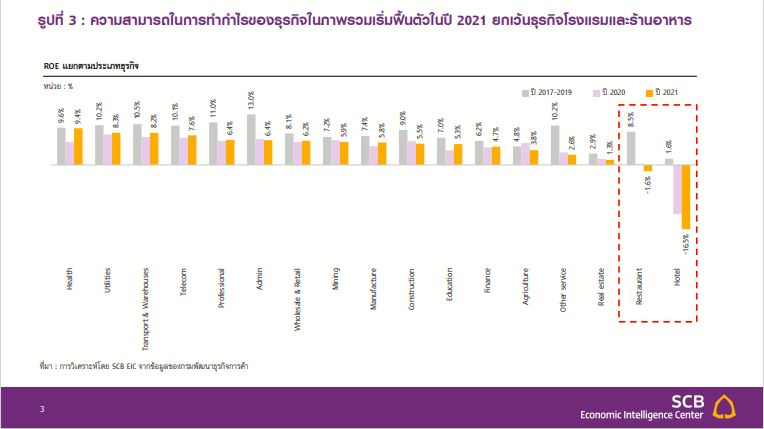

Hotels and Restaurants: The Most Affected by Profit Declines and Liquidity Issues

Due to lockdown measures and strict international travel restrictions, the hotel and restaurant sectors were severely impacted in 2020 and continued into 2021, with profitability clearly declining, as reflected in the average ROE for the hotel sector dropping to -16.5% in 2021 from -12.7% in 2020.

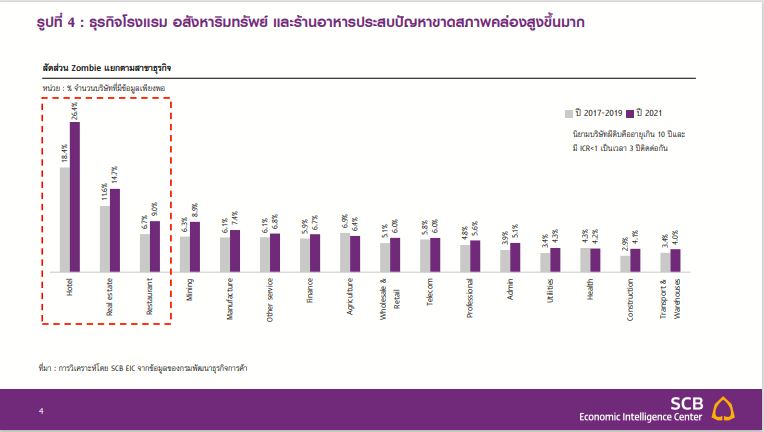

The restaurant sector also contracted by -1.6% in 2021 from 0.28% in 2020, indicating a slower recovery compared to other business types. This aligns with the increase in zombie firms in this sector, which faced significant liquidity shortages, with the hotel sector seeing the highest increase in zombie firms by 8 percentage points compared to pre-pandemic averages.

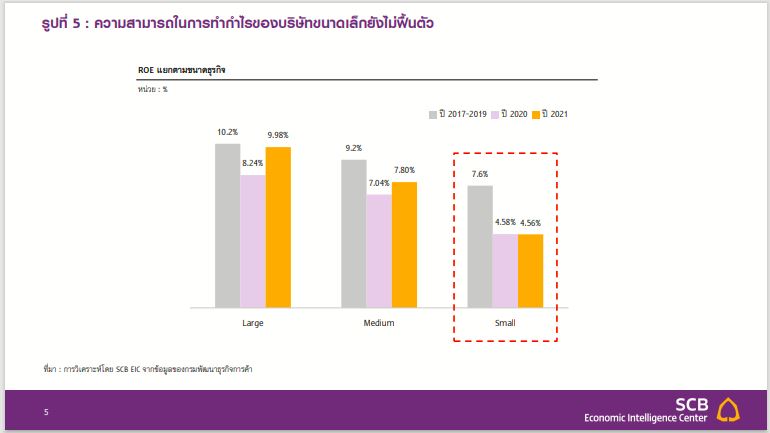

SMEs Suffer More Severe Impacts from the COVID Crisis than Larger Businesses

This is reflected in the ROE for 2021, which decreased by 3 percentage points compared to the pre-pandemic period, while the ROE for large and medium-sized companies began to improve from 2020, with large companies' ROE recovering close to pre-COVID levels.

Analysis of the proportion of zombie firms in 2021 showed that small companies had a significantly higher increase in zombie firms by over 1.5 percentage points compared to pre-COVID averages. It is evident that, in terms of both profitability and liquidity, small businesses overall have been more heavily impacted by the COVID crisis, partly due to limitations in accessing working capital and credit, even with government or financial institution support. In contrast, larger companies may have better access to funding sources and diversified risks across various markets, resulting in less severe impacts.

Small Companies in Hotels, Restaurants, and Real Estate Face the Most Severe and Concerning Impacts

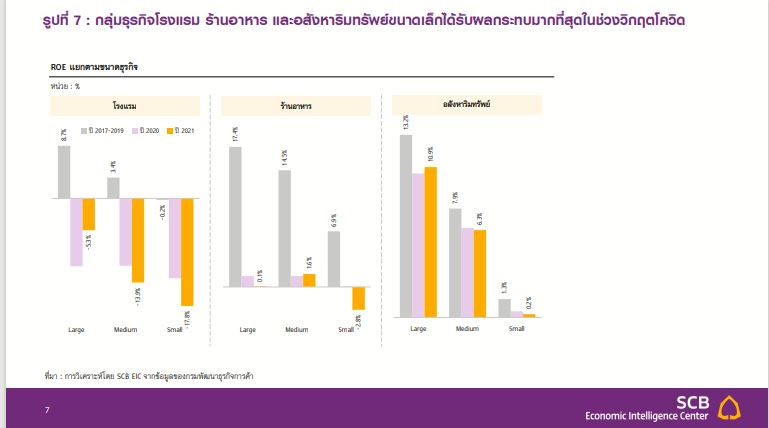

Small hotels saw their ROE drop to nearly -20% in 2021. The higher impact on small hotels compared to medium and large hotels may stem from tourists' significant health concerns, with a limited number of small hotels certified under the SHA+ standard. The first tourists returning to travel, both Thai and foreign, are primarily those with higher purchasing power, benefiting larger 4-5 star hotels. Additionally, promotional room rate reductions under government tourism stimulus measures or marketing strategies of large hotels have attracted more budget-conscious travelers.

However, it is expected that in 2022, all sizes of hotels will improve from the low point in 2021 as most have announced the reopening of the country and gradually relaxed international travel measures, leading to an increase in tourist numbers and a gradual recovery of the hotel business.

Meanwhile, small companies in the restaurant and real estate sectors are also more affected than larger companies, as reflected in their ROE dropping into negative territory in 2021. In the real estate sector during COVID, operators had to delay new project launches due to significantly reduced purchasing power, leading small companies to face further declines in capability and an inability to offer price promotions to clear inventory against larger or medium-sized companies due to inferior cost management, limiting their ability to reduce prices while maintaining profit margins.

In contrast, larger and medium-sized companies can afford to lower prices more or accept losses from sales to improve cash flow, while consumer confidence in their brands or products is lower, leading to cash flow issues and subsequent debt repayment problems.

Interestingly, medium-sized restaurants have been less affected compared to larger and smaller companies, possibly due to their better adaptability by offering more consumer choices and joining delivery platforms at lower costs than larger companies.

Recovery of the Thai Business Sector and Challenges

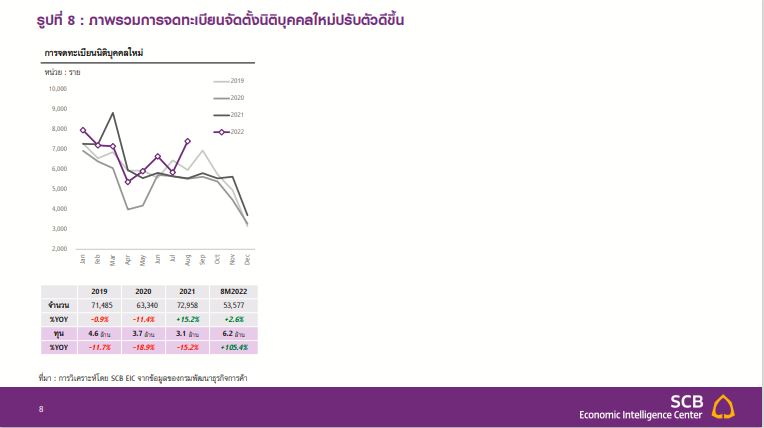

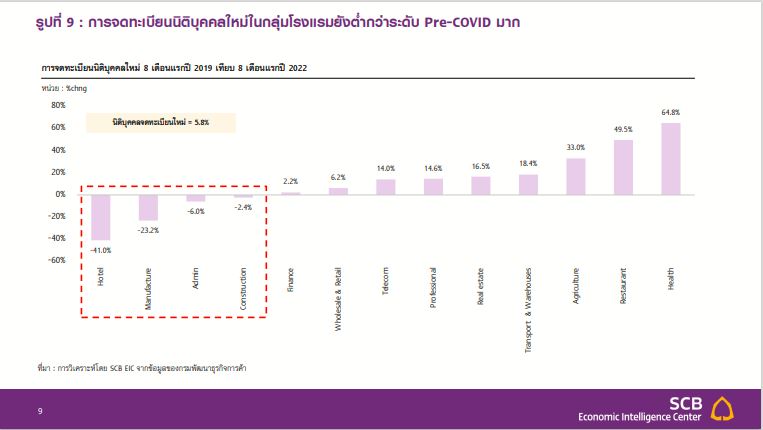

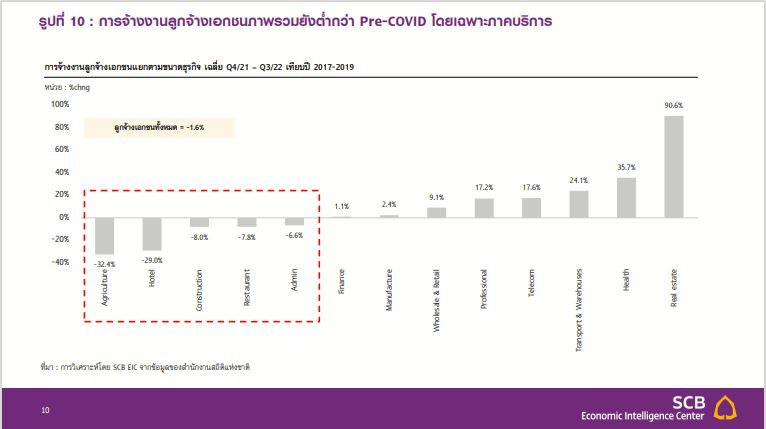

In 2022, Thai businesses began to recover from the lowest point, with the number of new registered companies in the first eight months of the year continuing to grow from 2021, along with an increase in the value of new registered capital. However, when considering the types of businesses, the service sector, particularly hotels, still has a low number of new registered companies and employment that has not fully recovered.

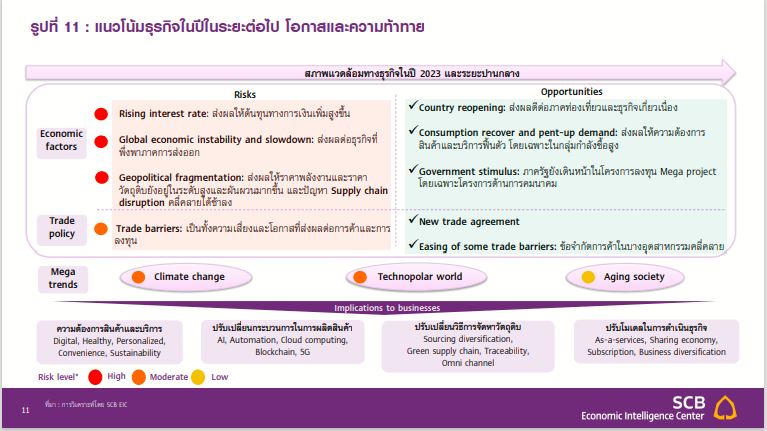

Nonetheless, the recovery of the Thai business sector remains fragile due to ongoing economic uncertainties and unevenness from rising financial costs, the trend of increasing interest rates, the global economic slowdown affecting export-dependent businesses, geopolitical conflicts leading to high and volatile energy and commodity prices, and slow resolution of supply chain disruptions.

However, the improving COVID situation presents an opportunity for the Thai business sector to recover, as high purchasing power groups demand goods and services, and the government continues to push forward with mega project investments, particularly in transportation.

Businesses likely to grow include those that respond to consumer recovery or align with global trends or are related to mega project investments, while some businesses face risks from the global economic slowdown or are affected by mega trends such as climate change, technological innovation, and an aging society.

Implications for Public Policy and Business Adaptation

In the near future, public policy should be adjusted to focus more on addressing specific issues, as some companies can return to normal operations and their revenues are beginning to recover. Public policy should aim to reduce costs while increasing revenues, especially for small businesses in the service and real estate sectors that have been more affected, through examples of measures such as:

(1) Support Measures for Business Costs

In the past, operators have had to bear costs from fluctuating energy prices, which are expected to remain high, along with increased minimum wages and labor shortages in the service sector. In the short term, the government should implement measures to subsidize energy prices and wages, especially for small operators, to ensure business survival. In the long term, it should provide knowledge on cost management planning and promote energy efficiency improvements through tax incentives and financial subsidies to encourage investment decisions and effective energy management.

(2) More Targeted Economic Stimulus Measures instead of broad measures to align with reduced spending stimulus budgets following the expiration of the COVID emergency loan act. For example, the next phase of the “We Travel Together” project should still be utilized to assist hotels and the service sector but may provide greater subsidies for small hotels or allow the purchase of goods or services to be used as personal income tax deductions, such as the “Shop Dee Mee Khuen” initiative that offers tax benefits to consumers for spending on small business goods and services.

Importantly, beyond government assistance, operators should understand the issues and prioritize adaptation to overcome this crisis as well, considering the following factors:

(1) Maintain Business Viability Alongside Risk Management

Focusing on financial management by reducing unnecessary operational costs and mitigating the impact of cost fluctuations, such as improving production processes, enhancing machinery efficiency, and increasing business flexibility to adapt quickly post-crisis.

(2) Focus on Customer Needs by monitoring changes in consumer behavior, possibly using data analytics to track evolving consumer demands or creating customer journeys considering new normal requirements and developing products and services that address customer needs or pain points, such as designing new products to offer customers more choices in a high-price environment, emphasizing best value for money.

(3) Transform Business Models to Align with Changing Environments according to consumer behavior and market conditions, such as adjusting sales models to direct-to-consumer, subscription models, or as-a-service models, and expanding opportunities into other businesses to reduce risks from reliance on a single income source and increase long-term growth opportunities.

(4) Invest for the Future through investments in technology to enhance production efficiency (e.g., AI automation), improve energy efficiency, and research and develop products to meet market demands and address production issues, such as developing products that can flexibly adapt to changes in raw materials and investing in retraining and reskilling/upskilling employees to enhance workforce skills, which will help reduce overall business costs in the long term and align with new technologies and trends.

Thank you for the information from: SCB Economic and Business Research Center (SCB EIC)