Challenges Facing the Thai Steel Industry in the Net Zero Era

What has been the situation of the Thai steel industry in the past and in 2022?

The price of steel in the first half of 2022 continued to rise from 2021 due to energy costs and lockdowns in China, while in the latter half of the year, steel prices are expected to decline. Steel prices surged dramatically over the past two years, with 2021 seeing a decrease in Chinese steel production due to environmental measures and quality control in China. In 2022, the escalating war between Russia and Ukraine led to a continuous rise in oil prices since the first quarter of 2022. The movement of Chinese steel prices is closely related to the movements of coal and oil prices in the global market, as these are significant costs in the steel industry. Additionally, China's Zero COVID measures, which included lockdowns to reduce the spread of the Omicron variant to zero, contributed to a decrease in steel supply from China due to the closure of iron ore and coal mines and steel mills. As a result, Chinese steel prices reached 6,000 yuan/ton in April 2022, increasing by an average of over 25-30% per year compared to early 2020 prices. Since Thai steel prices closely follow Chinese steel prices due to Thailand's reliance on steel imports from China, this has also led to increases in Thai steel prices, including scrap steel, billets, and flat steel (Slap) imports. In the latter half of 2022, Thai steel prices are expected to decline along with energy costs, coupled with a slowdown in steel demand in China and increased steel exports from Russia to Asia, which previously exported to the EU, further pressuring Chinese steel prices downward.

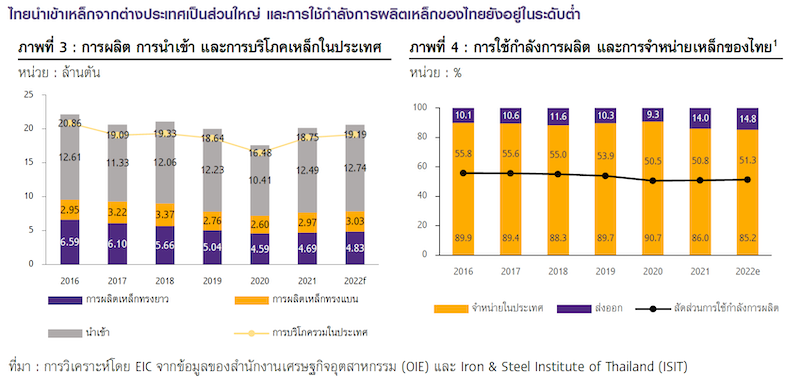

EIC predicts domestic steel consumption in 2022 will be 19.2 million tons (+2% YOY), primarily driven by imported steel, while domestic steel production capacity utilization remains low. In the first half of 2022, domestic steel production and consumption contracted by -6.4% YOY and -16.9% YOY, respectively, due to a slowdown in automobile production caused by semiconductor shortages and a slow recovery in private construction. Additionally, the first quarter of 2022 was further hampered by concerns over the uncertain COVID-19 outbreak. For the remainder of 2022, EIC believes that Thai steel production will be pressured by demand, particularly in the automotive sector, which has not fully recovered. This leads to an expectation that overall domestic steel consumption in 2022 will be around 19.2 million tons (+2% YOY), showing slight growth from 2021, driven by both imported and domestically produced steel.

Over 90% of steel production in Thailand is for domestic consumption, which is still insufficient to meet domestic demand. Moreover, Thailand can only produce medium to high-end steel, which means it remains reliant on imports from abroad, especially from China, the world's largest steel producer. Consequently, the utilization rate of domestic steel production capacity in 2022 is expected to remain low.

How does environmental issues relate to the steel industry?

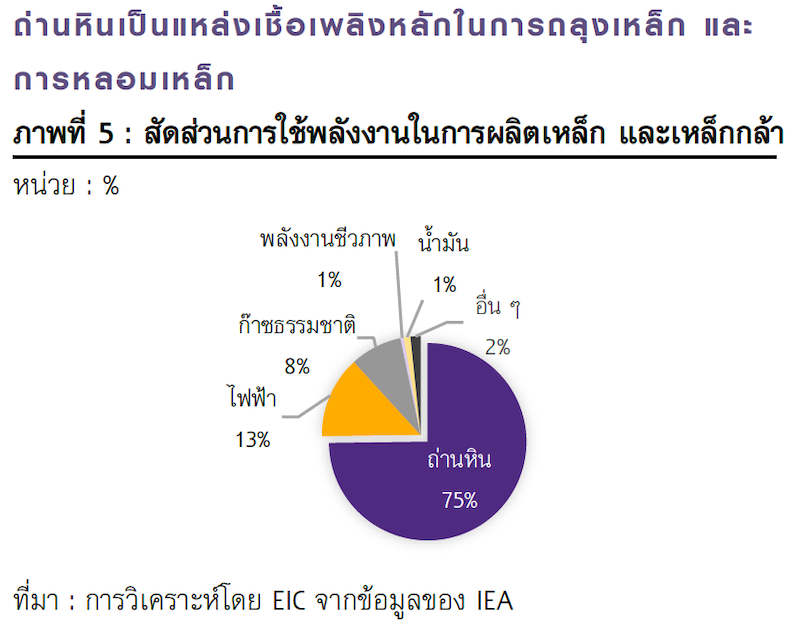

Global steel production relies heavily on coal, leading to significant GHG emissions. This is particularly true for the processes of smelting iron ore and steel melting, which require high temperatures, with coal being the primary fuel source, accounting for about 75% of total energy consumption. Following this, electricity and natural gas account for approximately 13% and 8% of total energy consumption, respectively.

Furthermore, data from the World Steel Association indicates that for every ton of steel produced, GHG emissions from energy combustion can reach as high as 1.85 tons, and over 128,704 liters of water are used in the cooling process. It is undeniable that steel production impacts the environment, particularly through GHG emissions. Therefore, major global steel producers are making efforts to reduce GHG emissions from production processes in various ways, including adjusting production processes, improving technology and production techniques by increasing the use of hydrogen and renewable clean energy. At the same time, governments in many countries are implementing various measures to encourage the steel industry to reduce GHG emissions, such as financial support and funding for technology upgrades and carbon pricing.

Major steel-producing countries such as China, the EU, and Japan are beginning to develop a more environmentally friendly steel industry. China has been actively promoting a more environmentally friendly steel industry since 2021 by implementing stringent steel and environmental standards, including shutting down steel plants using induction furnaces and increasing support for electric arc furnace (EAF) steel melting. This is due to the higher GHG emissions from induction furnaces compared to EAFs, and the quality of steel produced from induction furnaces depends on the quality of scrap steel, making it less consistent and harder to control than steel produced from EAFs. It is expected that these policies will enable China to reduce GHG emissions by approximately 0.5% of total industrial GHG emissions.

In the European Union (EU), measures have been established for carbon pricing at the border, known as Carbon Border Administrative Management (CBAM), which is a mechanism used by the EU to prevent carbon leakage from steel imports from countries without carbon pricing. This will make EU-produced steel less competitive due to higher carbon pricing costs. Steel and iron are among the top five products subject to CBAM, requiring non-EU steel producers to report both direct and indirect GHG emissions from production activities from 2023 to 2025. Furthermore, starting in 2026, steel importers in the EU will need to declare and purchase CBAM Certificates to cover GHG emissions from imported steel products. De Nederlandsche Bank (DNB) predicts that with the implementation of CBAM and carbon taxes, EU steel importers will see an increase in import costs of approximately 1.3%. However, this carbon tax cost will decrease if producers can reduce their carbon intensity in steel production.

Japan has established minimum lifespan standards for steel to promote recycling and has set up a fund for issuing Green Bonds to assist industries with high GHG emissions in raising funds for technology upgrades to reduce GHG emissions. The steel industry is one of the key sectors receiving this support. The Japan Iron and Steel Federation and several Japanese steel producers, such as Nippon Steel, Kobe Steel, and JFE Steel, aim to reduce GHG emissions by 30%-40% compared to 2013 levels by 2030 and strive for carbon neutrality by 2050.

Additionally, developed countries like Germany, New Zealand, and Australia are focusing on producing greener steel by developing hydrogen technology for clean energy production and increasing the use of Direct Reduced Iron (DRI) techniques in steel production combined with EAFs to achieve goals of reducing coal energy use and GHG emissions.

EIC views CBAM as the beginning of environmental awareness in the steel industry, as the costs associated with CBAM fees that EU steel importers will bear starting in 2026 will pressure steel producers exporting to the EU to accelerate reductions in carbon intensity to maintain competitiveness. As the EU has set CBAM measures, steel is one of the first products that must adapt to these measures, inevitably impacting steel producers exporting to the EU. Even in the near term, from 2023 to 2025, non-EU steel producers will still be required to report GHG emissions, but full implementation will begin in 2026 when EU steel importers must purchase CBAM Certificates, which will increase import costs and pressure steel producers in countries like China, Russia, and the UK to reduce GHG emissions in their steel production processes to maintain their export competitiveness in the EU market.

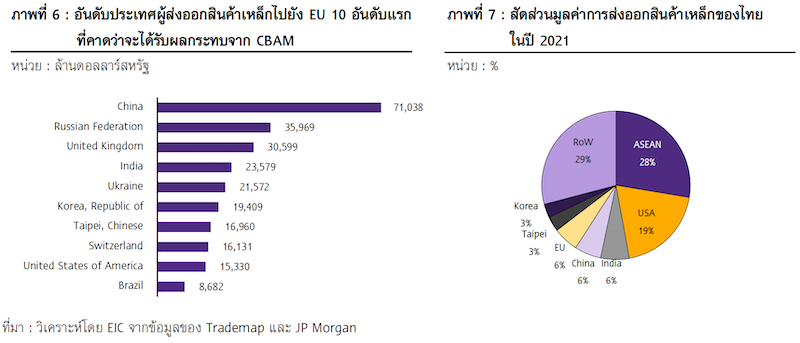

In 2021, Thailand exported steel products to the EU, accounting for 6% of the total value of steel exports. Thai steel exports to the EU may not be significantly affected by CBAM in the short term, as the value of steel products exported to the EU represents only 0.04% of Thailand's total exports, which is relatively low. However, in the future, if the Thai steel industry grows and upgrades to produce higher-quality steel for export, the EU may become an important export market for Thailand. If the Thai steel production process cannot reduce GHG emissions, it will impact competitiveness in exporting steel to the EU market and lead to lost trade opportunities in the future.

Moreover, the United States is also considering implementing CBAM measures for industries with high carbon intensity emissions per ton of production, including petroleum, natural gas, coal, aluminum, steel, cement, fertilizers, paper, and ethanol. In 2024, producers and importers of these goods in the United States will be subject to taxes, and by 2026, the measures will expand to final goods with raw materials that have high carbon intensity, starting from 226 kilograms and reducing to 100 kilograms by 2028. It is evident that steel is among the first products with high carbon intensity that will be subject to these measures. In 2021, Thailand exported steel products to the United States valued at 44.815 billion baht, accounting for 19% of Thailand's total steel exports, making the United States the second-largest export destination for Thai steel after the ASEAN region. This means that Thai steel producers exporting to the United States will also need to adapt to various measures that the U.S. may implement in the future.

EIC believes that steel production remains a crucial industry for Thailand, and amidst the Net Zero trend, the Thai steel industry must transition its production technology to reduce the carbon intensity of its products. Although Thai steel production focuses on medium and high-end steel, the production process still generates pollution. If Thailand aims to reduce GHG emissions from the steel industry by decreasing domestic steel production and relying more on imports, it will have widespread impacts, including leaving domestic steel producers with excess production capacity, as the current utilization rate remains low. Additionally, high reliance on steel imports increases risks for industries that consume large amounts of steel, particularly in construction and automotive manufacturing, leading to potential steel supply shortages that could halt construction and automotive production, as well as fluctuating import steel prices that complicate cost control in construction and automotive production.

Currently, Thai steel producers are turning to EAFs to make steel production more environmentally friendly. However, this technology is still relatively expensive, which could lead to higher steel prices and make it difficult to compete with imported steel. Thus, the transition to EAFs is still limited to large steel producers with sufficient capital. Meanwhile, recycling steel is a viable option that promotes the circular use of resources, but it remains insufficient to meet the increasing domestic steel demand driven by the country's economic development and expansion.

EIC sees another solution for environmentally friendly steel production as the improvement of production technology and techniques. EAFs can help overcome the challenges of sourcing quality scrap steel, allowing for the recycling of a larger volume of scrap steel with varying quality, as these furnaces are better at removing impurities from scrap steel. This will help reduce carbon intensity across the steel industry's value chain since EAFs consume less energy than induction furnaces, thereby alleviating energy cost burdens during periods of high energy prices. Additionally, using recycled steel will help reduce GHG emissions from upstream steel production and transportation of imported steel into the country.

Currently, developed countries worldwide, particularly in Europe, are developing green hydrogen to use as a clean fuel substitute for fossil fuels, which will significantly reduce GHG emissions in the industrial sector. Although this technology currently has high costs and may not be commercially viable or suitable for Thailand's context, it is expected that costs will decrease in the future and will be a key to achieving Net Zero. Thailand should closely monitor the development of the hydrogen industry and apply knowledge of this technology appropriately to create a future technology transition plan, which will lead to significant GHG emission reductions in steel production.

The trend of reducing GHG emissions throughout the supply chain, both domestically and globally, in industries that incorporate steel, such as environmentally friendly building construction, electric vehicle production, and consumer goods with low carbon footprints, aligns with consumer trends that prioritize environmental concerns, especially in European countries that are increasingly aware of the severe impacts of climate change and are importing high-quality steel for use in automotive and aerospace manufacturing. This presents opportunities for businesses that can adjust strategies to reduce GHG emissions to become part of the supply chain, such as leading automotive manufacturers like Volvo and Mercedes-Benz, which currently seek partnerships with high-quality steel producers to procure carbon-neutral steel or fossil-free steel, with top-tier steel producers like SSAB from Sweden capable of supplying such steel, thus expanding business opportunities in the Net Zero carbon supply chain.

EIC believes that the trend of reducing GHG emissions throughout the supply chain is pressuring the Thai steel industry to accelerate its production processes to lower GHG emissions. If steel producers do not invest in changing production technologies, they will have to bear the increasing costs of GHG emissions in the future, impacting their competitiveness. Additionally, steel producers in various countries are gradually adjusting their steel production processes to reduce GHG emissions. If Thai steel producers do not adapt their production processes, they will face lost trade opportunities in the future and miss out on being part of the global Net Zero carbon supply chain.

Government support will be a crucial driving force for the Thai steel industry to reduce GHG emissions. The constraints of transitioning steel production technology to reduce GHG emissions lie in the technology costs, particularly for EAFs, which remain relatively high. Therefore, the government should play a significant role in implementing measures to facilitate technology changes for both large and SME steel producers, such as providing tax incentives, financial support, and exemptions on imports for operators investing in machinery upgrades, and promoting funding mechanisms through green bonds or sustainability bonds.

Moreover, the government should establish clear criteria for what constitutes green steel based on the GHG intensity emitted from steel production, such as setting carbon intensity limits for steel production per ton to create clear environmental standards for green steel and facilitate the implementation of measures based on the defined GHG emission levels. This includes clarifying the definition of green steel in Thailand.

Additionally, the government may implement measures to stimulate the use of environmentally friendly steel concurrently, such as promoting the procurement of steel from operators that can reduce GHG emissions in public construction projects. The costs of purchasing environmentally friendly steel, which has low GHG emissions, could be tax-deductible for corporate income tax and personal income tax for construction and renovation projects. There could also be reductions in corporate income tax for producers based on the amount of GHG emissions reduced. If the use of environmentally friendly steel becomes more widespread, it will encourage steel producers to adopt technologies that reduce GHG emissions. Furthermore, promoting the ability of Thai steel producers to produce high-quality steel will enhance attractiveness and business opportunities as suppliers to high-tech industries that require high-quality steel, such as modern automotive, aerospace, and defense industries, which are targeted for development in the government's economic development plan.

However, the implementation of various measures should be approached cautiously, especially regarding subsidies that may be perceived as unfair support, leading to complaints from export destination countries. Although Thailand's steel exports currently represent a small proportion compared to domestic production and other export categories, it could still impact the export capabilities of Thai operators. For example, U.S. steel producers have accused the Thai government and agencies of providing subsidies for steel nails through various programs, resulting in the U.S. initiating an investigation into countervailing duties (CVD) on steel nails from Thailand. However, preliminary investigation results indicated that the level of subsidies for Thai steel nails was minimal, suggesting no actual subsidies.

In addition to government support, cooperation from operators is also crucial for enhancing the development of the industry. One key factor in determining the direction of GHG emission reduction efforts for Thailand is the collection of GHG emission data, which should be modern, detailed, and reflect the actual values occurring in the production activities of the Thai steel industry. This requires serious oversight and verification by government agencies, along with cooperation from operators to provide sufficient data for analyzing current environmental situations and establishing clear GHG emission reduction targets for the steel industry, as well as formulating policies and measures for implementation.

If there is genuine cooperation between the government and the private sector in implementing measures that promote the Thai steel industry to reduce GHG emissions, it will help Thailand achieve its GHG emission reduction targets as expressed in the 26th UN Climate Change Conference of the Parties (COP26). Currently, many countries are beginning to implement measures to protect the environment from further degradation. However, this process still includes a transition period before full enforcement.

Therefore, Thai steel producers should seize the opportunity during this transition period to plan their business operations to prepare for more environmentally friendly steel production and elevate the Thai steel industry to align with the Net Zero trend. For SME steel producers, forming networks will strengthen their ability to raise funds and transfer technology, supporting their adaptation and business operations amidst the pressures of the steel industry that must become more environmentally friendly.

Analysis by...https://www.scbeic.com/th/detail/product/steel-230822