Happy Retirement Hub: Enjoying Retirement with Real Estate

According to research, Thailand fully transitioned into an aging society in 2022, with 20% of the population aged 60 and over. The United Nations defines an aging society as one where 10% of the population is aged 60 and above, and 7% is aged 65 and above. Meanwhile, Thailand's birth rate continues to decline, with a population growth rate of only 0.26% in 2022, equating to a birth rate of 10.25 per 1,000 people. It is projected that by 2033, Thailand will reach a super aging society, with 28% of the population aged 60 and over and 14% aged 65 and above. (Data from the Thai Institute for Research and Development of the Elderly) Similar to Japan, which has the highest elderly population in the world, Thailand's post-retirement savings rates are significantly lower, leading to a situation described as 'old and poor.' If we also consider health issues, we can define it as 'old, poor, and sick.' Therefore, we have three options: 1. Wait for government welfare support, but with the country's increasing public debt burden, relying on government assistance for a comfortable retirement seems unlikely. 2. Hope that children will take care of us, but many choose to remain single or have pets instead of children. For those with children, the hope is that they can support themselves and their families without tapping into their parents' retirement savings. This leaves us with the final option: 3. Self-reliance, as emphasized in Buddhism: 'One is one's own refuge.' This is likely the most stable solution.

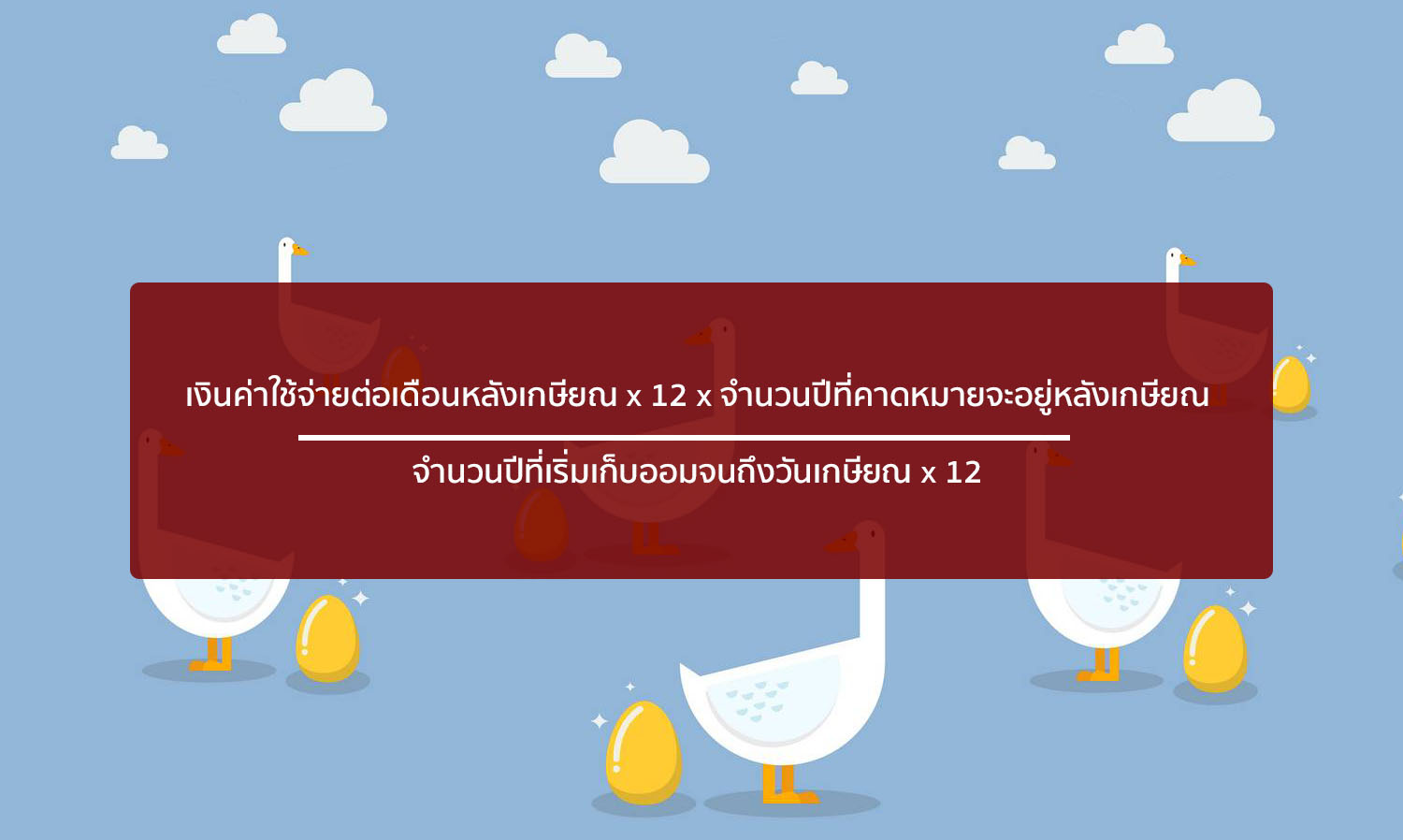

Many people study post-retirement financial planning through books, seminars, or podcasts (a combination of iPod and broadcast, meaning internet broadcasting), often via YouTube, where there are many skilled money coaches. Their main principle is to set a target for how much money is needed for post-retirement expenses, multiplied by the number of years after retirement, as illustrated in the formula below.

Formula for Monthly Savings for Retirement

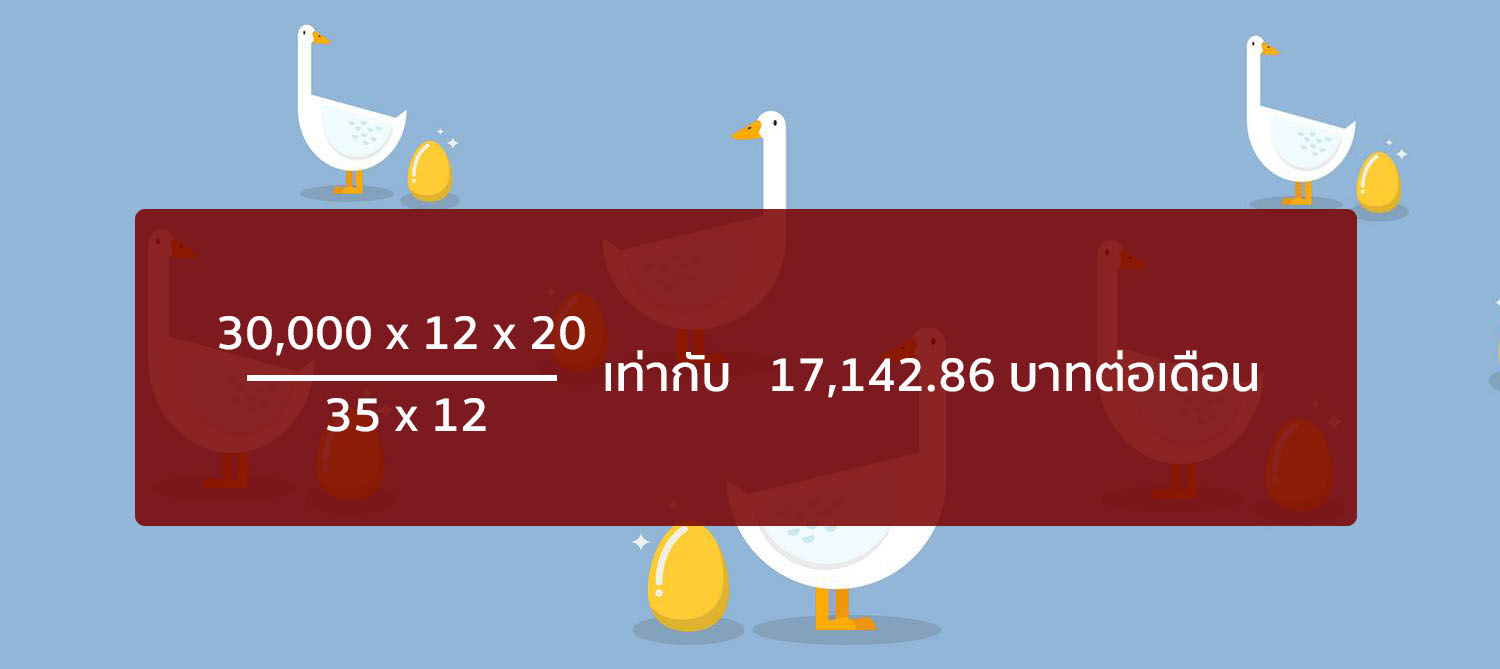

For example, if you want a monthly income of 30,000 baht, retiring at age 60 and living until 80 means you need 30,000 x 12 x 20, totaling 7,200,000 baht for the 20 years after retirement. Dividing this by the remaining working years shows that those who start saving early have a significant advantage. For instance, if you start working at age 25, you have 35 years left until retirement, which equals 420 months.

Indeed, you would need to save 17,142.86 baht per month, which is not easy to maintain for 35 years. If you start later at ages 35, 45, or 55, the monthly savings requirement increases, along with various obstacles such as personal desires for luxury items, travel, and borrowing money from friends or relatives in need. Even if you manage to follow the plan, without effectively managing the growth of your savings, by age 79, your funds may be nearly depleted, yet you may still not be ready to retire. So, exploring alternative options like investing in real estate to generate income becomes essential. This is akin to creating a 'golden goose' that lays eggs for you to enjoy, and the goose itself often appreciates in value. Let me share my own case study.

In 2022, I invested in a three-story commercial building with two units, purchasing it at a friendly price of 3.25 million baht, while the market price was around 3.5 million. This aligns with the theory of buying good real estate, as I made a profit immediately upon transfer. Before purchasing, I had already lined up potential tenants, allowing me to secure tenants just one month after the transfer at a rental price of 15,000 baht per unit, totaling 30,000 baht. My monthly mortgage payment to the bank is 44,000 baht, meaning I need to contribute an additional 14,000 baht from the rental income (since I bought it later in life, my monthly payments are higher; had I purchased it 10 years earlier, the payments might have been comparable to the rent). The mortgage term is 10 years, but I plan to pay it off in 5 years. Once the mortgage is paid off, the rent will convert into passive income of 30,000 baht per month. However, not every 'goose' lays eggs consistently, so I recommend creating a 'farm' of golden geese—having more than one income-generating property. Commercial properties in prime locations typically outperform residential rentals. This example is just the beginning of planning a happy retirement through income-generating real estate. If your income goal is in the hundreds of thousands or millions, the story will be much more complex. For now, I will conclude with these initial thoughts and options, and in the future, I will discuss in detail how to create golden geese.

Veerapol Jongjareonjai, Executive Director of the Thai Real Estate Association (2015 - Present)

Chairman of the Isaan Architects Committee, Association of Siamese Architects under the Royal Patronage (2018 - Present)

President of the Real Estate Association of Nakhon Ratchasima (2015 - 2017)