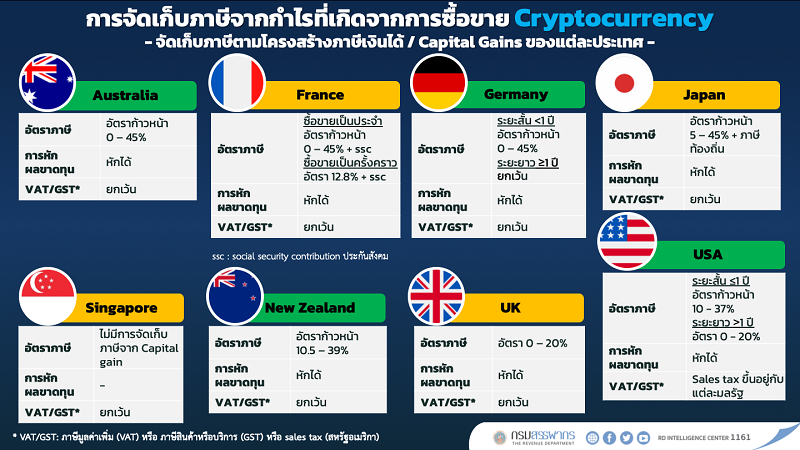

Revenue Department Sets Guidelines for Crypto Taxation, Allowing Loss Offsets Against Profits

After the Revenue Department held discussions to gather views, opinions, and suggestions from over 3,000 entities in both the public and private sectors regarding appropriate guidelines for digital asset taxation, they proposed beneficial ideas for both government and private sectors to collaboratively promote the Thai digital asset industry in the future.

Mr. Aekniti Nitithanprapas, Director-General of the Revenue Department, stated that the feedback and collaborative efforts from all parties, including relevant government agencies and private sectors, indicated the need to adopt a taxpayer-centric approach, ensuring clarity, flexibility, and a forward-looking perspective.

The “clarity” aspect will define the income tax structure under current laws, with the Revenue Department outlining the following guidelines:

1. Clearly define income by specifying types of income and benefits that encompass profits/income from transfers/benefits from digital assets.

2. Calculate costs using standard accounting methods, which can be done in two ways: the First-In, First-Out (FIFO) method or the Moving Average Cost method, with the option to change the calculation method in subsequent years.

3. Measure the value of digital assets at the time of acquisition or the average price on the acquisition date.

Details will be included in the Tax Payment Guide for Individuals Trading Digital Assets, which the Revenue Department is currently reviewing in collaboration with the Thai Digital Asset Association and the Thai Digital Asset Business Operators Association, with plans to publish it on Monday, January 31, 2022.

Regarding “flexibility”, the Revenue Department has several approaches to implement flexibility under current laws, which fall within its jurisdiction, categorized into income tax, withholding tax, and value-added tax (VAT) as follows:

1. For assessing taxable income (profits), the Revenue Department will propose a ministerial regulation to allow losses to offset profits within the same tax year, applicable only to businesses or Exchanges regulated by the Securities and Exchange Commission (SEC).

2. For withholding tax, in transactions conducted through Exchanges regulated by the SEC, the identity of the recipient cannot be determined, and the amount to be withheld is unknown, making it unnecessary to withhold tax.

3. For VAT, the Revenue Department will propose a royal decree to exempt VAT for transactions conducted through businesses or Exchanges regulated by the SEC and for digital assets issued by the Bank of Thailand.

Nevertheless, regarding “looking to the future”, the Revenue Department will consider discussions with the digital asset community and relevant agencies to explore future policy possibilities to amend necessary and appropriate laws, such as revising Section 50 of the Revenue Code related to withholding tax.

This would allow businesses or Exchanges to withhold and remit taxes to the Revenue Department, and consider changing the VAT collection type to a specific business tax (Financial Transaction Tax) for digital assets that are securities, among other considerations based on appropriateness and surrounding contexts.

In terms of business operations and investments in digital assets, there has been rapid development. In the past 1-2 years, the average daily trading value increased from 240 million baht to 4.839 billion baht, and the value of customer assets rose from 9.6 billion baht to 114.539 billion baht.

Additionally, the number of user accounts increased from 170,000 to 1.98 million, along with rapid evolution in technology, products, and transaction methods, which have become increasingly diverse and adaptable.