How to Plan for Retirement to Enjoy a Comfortable Life

When we talk about retirement planning, many people might think it's a distant issue or that retirement is still far away. They may forget to consider how many years are left to save money, whether the time spent earning will be enough to cover expenses in retirement, and how much money needs to be saved to ensure a comfortable retirement. Therefore, we should start preparing and planning our finances for retirement today.

Things We Need to Know Before Planning for Retirement:

- What will our life in retirement look like? Who will we live with? Where will we live?

- At what age do we expect to retire?

- How long do we expect to live?

Another important aspect is to explore the sources of income available, including studying the terms and conditions for withdrawing funds in detail. We should categorize income sources into lump-sum or regular income to plan our finances effectively.

Additionally, we need to assess post-retirement expenses based on our planned lifestyle or compare them with current expenses. Let's take a look at what these might include.

- Daily expenses such as food, clothing, household items, etc.

- Housing-related expenses such as water, electricity, and repairs.

- Health-related expenses such as medical care, health check-ups, and life insurance.

- Expenses for lifestyle and activities in retirement such as charity, donations, and travel.

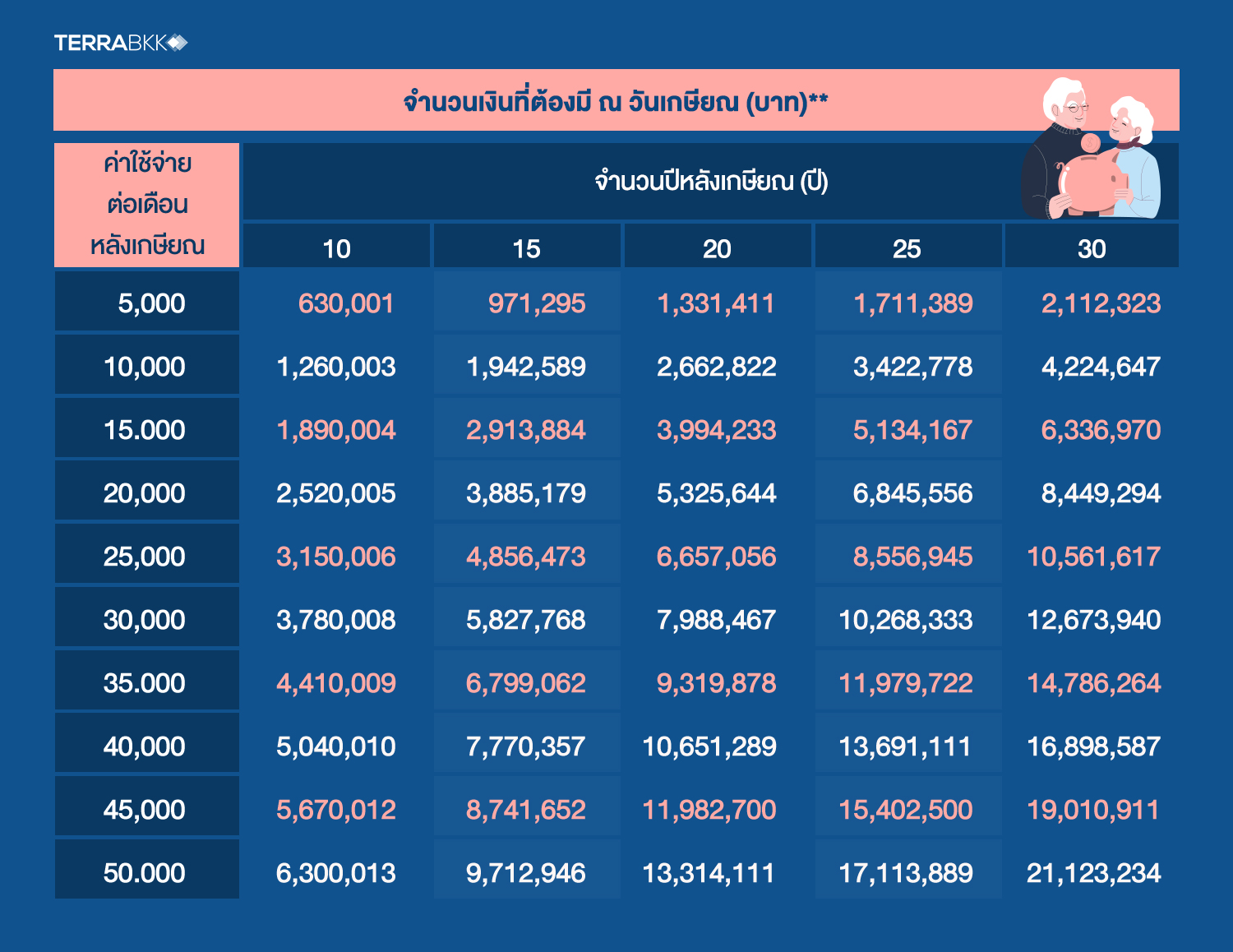

Alternatively, we can estimate monthly expenses after retirement, calculate them against the number of years planned for retirement, and compute the compounded annual return based on a post-retirement return rate of 1.90% per year (average fixed deposit interest from 2003 to 2018), while deducting an inflation rate of 3% per year. This will give us the amount of money needed at retirement as shown in the table below.

Furthermore, if we have a large sum of money from various funds or savings, we can invest it to generate returns for use in retirement. We can calculate the average return rate needed from our investments as follows:

After retirement, we want to have 10,000 baht per month.

We have a lump sum of 3,000,000 baht for retirement.

Calculating annual expenses after retirement equals 10,000 x 12 months, which equals 120,000 baht per year.

Calculating the average return rate equals (120,000 / 3,000,000) x 100, which equals 4% per year.

To have 10,000 baht per month after retirement from investments, we need to invest the 3,000,000 baht to achieve an average return rate of 4% per year.

Investment Options After Retirement

Investing after retirement is also essential because once retired, we no longer have a regular job, and income does not come in every month. We need to manage the lump sum from our savings to ensure it grows. Therefore, we should look for and plan investments, which can take various forms depending on the risk tolerance of each individual.

The future is uncertain, and having insufficient funds poses a significant risk in life. "Financial planning for retirement is crucial to ensure we have enough money to live comfortably in our later years."

Discussion

Follow breaking news Investment property articles on Facebook, click here.