Which Type of Multi-Purpose Loan Secured by Real Estate is Right for Us?

In an era where the economy is struggling, compounded by the spread of the COVID-19 virus, income has become increasingly uncertain. For some, this has led to business closures and job losses, resulting in many individuals facing insufficient income to cover their expenses, forcing them to take on debt. However, some are fortunate enough to own their own homes, providing at least a place to stay and the option to secure loans using their property as collateral.

Currently, almost every bank offers a type of loan for those who already own a home and need financing (not for purchasing a new home). The names for these loans vary by bank, but commonly heard terms include multi-purpose loans and home equity loans. In this article, we will refer to them as loans secured by real estate.

Loans secured by real estate generally fall into two main categories: 1. A lump sum loan that is repaid monthly to the bank over a specified period (depending on the appraised value of the property, the borrower's repayment ability, and the loan amount the bank is willing to provide). This is essentially a fixed-term loan (Fixed Loan or Loan). The second type is 2. A credit line set by the bank, which the borrower can draw upon as needed (possibly using checks or a debit card issued by the bank). When the borrower has funds, they can reduce the outstanding debt, and after reducing the debt, they can still access the credit line again, which is known as an overdraft loan (Overdraft or O/D). Overdraft loans do not require repayment at specific times and have no minimum payment requirements.

This article will explain the differences between loans secured by real estate in detail, especially regarding how banks calculate interest. Many borrowers may know the interest rate charged by the bank but may not fully understand how it is calculated. Importantly, borrowers often only remember that the bank charges interest rates of 6% or 7%, which is an incorrect way to remember interest rates.

Generally, banks have two types of interest rates: 1. Fixed Rate, meaning the borrower will receive this interest rate for the entire loan term, commonly found in auto loans with shorter repayment periods, and 2. Floating Rate, meaning the interest rate can fluctuate based on a reference rate, which includes:

2.1 MLR. (Minimum Loan Rate) is the minimum interest rate for prime borrowers

2.2 MOR. (Minimum Overdraft Rate) is the interest rate for overdraft loans for prime borrowers

2.3 MLR. (Minimum Loan Rate) is the interest rate for retail prime borrowers

Therefore, when a borrower receives a loan from a bank, they must know which reference interest rate the bank uses to calculate their interest. Generally, for loans related to real estate and long-term loans, banks tend to use floating interest rates based on the reference rate provided to the borrower. For example, MRR.+2% means that when the reference interest rate (MRR.) changes, the interest the borrower must pay to the bank will also change. This is because if the bank's costs increase, they will raise the reference interest rate, and conversely, if the bank's costs decrease, they will lower the reference interest rate.

Next, I will explain each type of loan: 1. Loans secured by real estate as a lump sum loan. In this type of loan, the borrower receives a lump sum and repays the principal and interest monthly as specified by the bank. The bank will assess the borrower's repayment ability. This type of loan is suitable for borrowers who have a specific purpose for the funds, such as home renovations. Interest is calculated daily based on the remaining principal, meaning that as the principal decreases, the interest will also decrease, known as reducing principal and interest. This results in the effective interest rate (Effective Rate or Effective Annual Rate: EAR) being lower than what the bank specifies due to the decreasing principal. Therefore, if the borrower makes additional payments or uses bonuses to pay down the debt, it will expedite the repayment process. However, any repaid loan amounts cannot be reused. The advantage of this type of loan is that interest does not compound, so even if the borrower is slightly late on payments, there will be no compounding interest.

For example, on March 20, 2021, the borrower received a multi-purpose loan secured by real estate for 2,000,000 THB at an interest rate of MRR.+2% (currently, MRR. is 10%). The borrower is to repay the principal and interest at 45,000 THB per month. Then, on April 3, 2021, the borrower made a payment of 45,000 THB. The method of calculating the principal and interest repayment is shown in the following table:

From the table above, it can be seen that even though the borrower did not make a payment at the end of March 2021, the loan interest did not compound. Interest continued to be calculated normally every day. In the early stages of repayment, the borrower may feel that the principal is decreasing slowly despite making regular payments to the bank. This is because the large principal amount results in a high interest amount. Borrowers must understand that every time they make a payment to the bank, the bank will first apply it to the interest accrued up to that point, and the remaining amount will go toward the principal. The repayment amount set by the bank considers the borrower's repayment ability because the bank only wants the principal returned along with the return on investment; they do not intend to seize the collateral.

The advantage of this type of loan is that interest will not compound, so the debt will not increase even if payments are slightly late. However, it will affect the borrower's credit history or credit bureau. Additionally, if payments are missed for more than 90 days, it will be classified as a Non-Performing Loan (NPL).

2. Loans secured by real estate as a credit line or overdraft loans. This type of loan is suitable for daily expenses or normal business operations (not for long-term investments). The bank provides net working capital since this type of loan is a revolving credit. The bank sets a credit limit for the borrower, meaning that if the borrower does not use the credit line, they do not incur interest. However, whenever the borrower utilizes the credit line, interest will be charged based on the amount drawn. When the borrower makes a payment to reduce the debt, the credit line can be reused (it is important to note that the funds deposited into the account are not considered debt repayment like the first type of loan but rather a reduction of the outstanding balance, as the borrower can withdraw the funds again). Revolving credit does not require the borrower to make payments every month or meet minimum payment requirements as long as the credit line remains active. However, the downside of revolving credit is that interest compounds at the end of the month since the funds deposited only reduce the outstanding balance, and interest continues to accrue daily. At the end of the month, the interest accrued during that period will be added to the principal, resulting in a higher principal for the following month, thus increasing the interest (Interest on Interest). See the following table for an example.

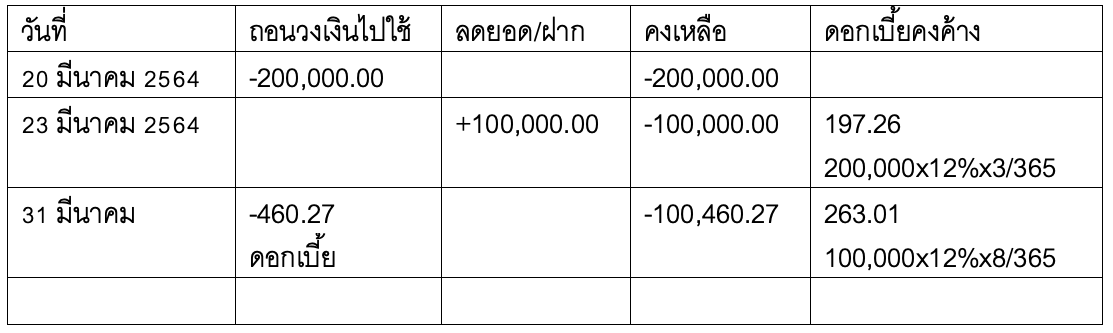

Mr. Somchai received a multi-purpose credit line of 1,000,000 THB at an interest rate of MRR.+2% (currently, MRR. is 10%).

From the example above, interest on revolving credit is charged when funds are drawn. When the borrower made a payment to reduce the debt on March 23, 2021, it was merely a reduction of the outstanding balance (unlike a loan where payments first go toward interest and the remainder goes toward the principal).

Revolving credit is quite convenient for accessing funds; borrowers can simply write a check or withdraw from an ATM, as they incur interest only when they use it. When they reduce the outstanding balance, they can reuse the credit line. However, borrowers must exercise financial discipline because misusing the funds can lead to problematic debt, such as using revolving credit for non-revolving assets like purchasing land or vehicles, ultimately resulting in unmanageable debt. Conversely, if revolving credit is used for non-revolving assets, such as using the credit line to buy a car for 950,000 THB on March 20, 2021, and not being able to reduce the balance, refer to the table below.

From the table above, if the borrower cannot find funds to reduce the balance, the account will soon become unmanageable, ultimately leading to debt restructuring.

The examples provided aim to guide borrowers in using the appropriate source of funding for their intended purpose. This means that if you need funds for long-term assets, such as purchasing land or renovating a home, you should use long-term financing sources, such as loans with a fixed term. However, if you need funds for daily expenses or business operations and plan to reduce the debt when income comes in, revolving credit can be suitable. In other words, revolving credit is designed to maintain financial liquidity.