Almost 1 Year with COVID-19 ... Are Mutual Funds and Real Estate Trusts Worth Considering?

Since the beginning of this year, the COVID-19 pandemic-19 has significantly impacted the performance of mutual funds and real estate trusts. Although the pandemic situation has eased, and the emergency decree. has not been extended since October 2020, real estate investments affected by COVID-19-19 are showing improved performance and trends, such as shopping malls, community malls that do not need to significantly reduce rents like during the lockdown, as well as exhibition centers, some hotels, and airports, which have resumed operations focusing on domestic market customers.

However, the prices of units in the market have significantly decreased, with the index for mutual funds and real estate investment trusts dropping (SETPREIT Index) by 25.2% in the first 11 months of 2020. While it is true that the performance of funds and real estate trusts will be affected in the short term, and/or cash may be retained to maintain liquidity in emergencies, this has led to a slight decrease in dividends per unit, but the significant drop in unit prices has resulted in some funds having dividend yields (Dividend Yield) that may even be higher than before COVID-19.

Changes in the SETPREIT Index during the first 11 months of 2020

Currently, interest rates are at a low level, as the Bank of Thailand has gradually reduced the policy interest rate from 1.25% in early 2020 to 0.50% in May 2020 and has maintained this rate until now due to the economic impact from the COVID-19 situation. Normally, a decrease in market interest rates supports an increase in the prices of mutual funds and real estate trusts, as investors tend to prefer investing in these funds due to their dividend yield being higher than interest rates.

However, the fact that the prices of mutual fund and real estate trust units have not increased, even though the COVID-19 situation seems to have passed its lowest point, may be partly due to investments flowing into other assets such as low-risk assets like government bonds, various debt securities, or foreign assets such as Chinese stocks, Vietnamese stocks, or stocks in the technology sector, because they are more attractive in terms of growth opportunities or less impacted by the COVID-19 situation.

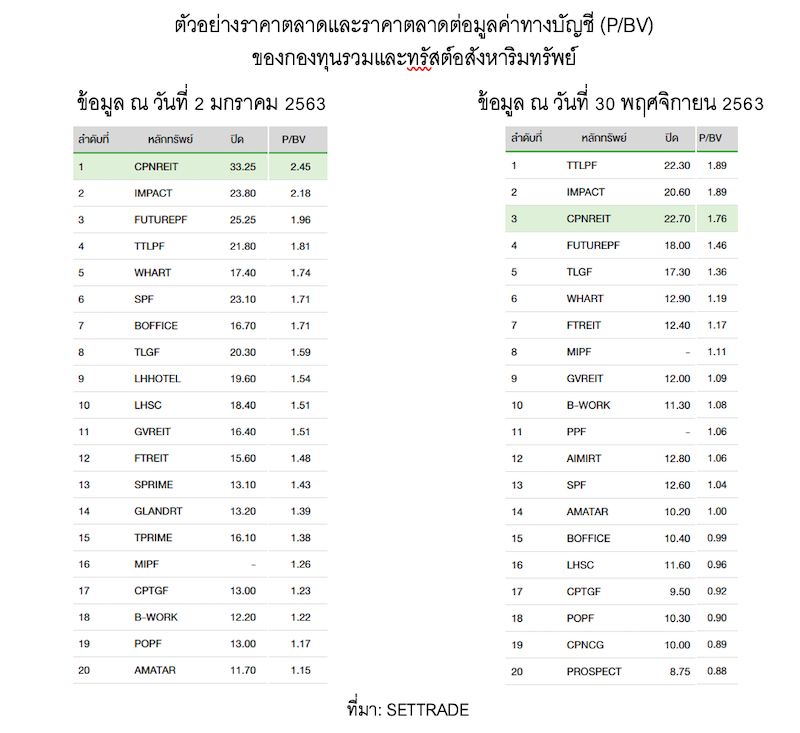

Although the investment trend in mutual funds and real estate trusts may face additional impacts from the second wave of outbreaks in Thailand since early December 2020 or risks from future outbreaks until vaccination coverage is achieved, if viewed as a long-term investment, considering that such situations are temporary negative factors and that performance is likely to recover in the future as it was before the COVID-19 event, the appropriate investment price assessment may consider comparing it with the accounting price (Book Value) based on the net asset value (Net Asset Value) of mutual funds and real estate trusts, which will have data released quarterly. For example, CPNREIT has a price-to-book value (P/BV) decreasing from 2.45 times at the beginning of the year to 1.76 times at the end of November 2020, or AMATAR has a P/BV decreasing from 2.45 times to 1.00 times at the end of November 2020.

In considering the accounting price, investors should consider the liquidity of the mutual funds and real estate trusts they intend to invest in, and examine whether the investment assets are leasehold rights or not. Because the accounting value of assets tends to decrease rapidly as the leasehold rights approach the end of the contract.