Valuation of Property Funds and REITs

Property Funds and REITs are investments that stand out for their relatively consistent dividend returns, with an average Dividend Yield of about 5 – 6% per year. This yield comes from rental income generated by completed properties. Additionally, rental prices typically experience Rental Growth in line with inflation, making these investments a potential hedge against inflation, as rising prices diminish the value of money over time.

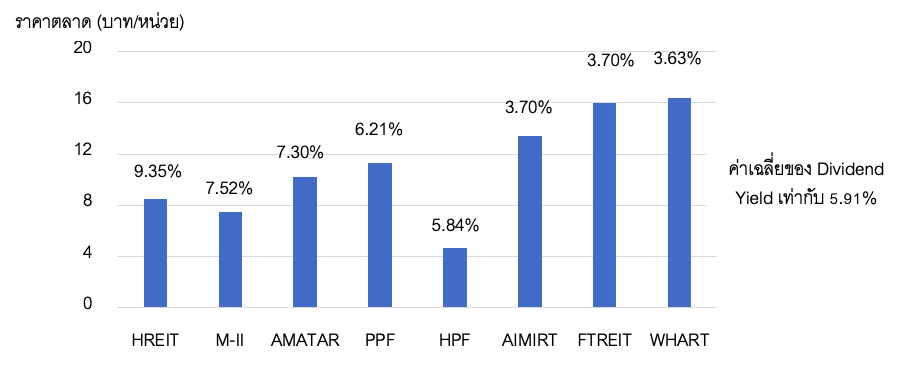

One common question I hear from investors considering investments in Property Funds and REITs is “The fund I’m investing in offers a high dividend yield, right?”, and they use this reasoning to make their investment decisions. While evaluating the dividend yield is one of the simplest ways to assess the value of Property Funds and REITs—by comparing the Dividend Yields of funds investing in similar asset types with similar income factors—this time, I will provide an example of funds investing in warehouse and factory rental spaces.

Example of Property Funds and REITs investing in warehouse and factory rental spaces from the previous fiscal year:

Source: SET (Data as of June 23, 2020)

From the example graph, readers will see that even though these investments are in funds that invest in the same asset type, HREIT offers a Dividend Yield of 9.35%, which is 2.6 times higher than WHART's Dividend Yield of 3.63%. Furthermore, when compared to the average Dividend Yield of similar funds in the industry, HREIT provides a return that is 1.6 times higher than the average of 5.91%.

Readers may wonder if a fund with a Dividend Yield higher than the industry average is a good investment or undervalued. First, it’s important to remember that while comparing Dividend Yields is a straightforward method for assessing investment prices by referencing the Dividend Yields of other funds and the industry, it has several limitations, such as:

- In cases where funds invest in leasehold assets, evaluating Dividend Yield may not be applicable, as it does not reflect that the investment value may become zero when the lease term expires, especially as the lease term approaches its end.

- If a fund has guaranteed returns or support from a sponsor to cover shortfalls when performance is below agreement, the Dividend Yield may only be high for a limited period and could decrease after the guarantee or support period ends.

- In cases where a fund faces special events that could significantly alter its income in the future, such as legal disputes or inability to renew contracts with tenants, past Dividend Yields may not accurately predict future performance, especially if the fund relies on a single tenant for its rental income, such as hotels or serviced apartments.

Therefore, considering a single year’s Dividend Yield may not accurately reflect the appropriate investment price, as the investment assets in each fund carry different risks, leading to varying Dividend Yields. From the example data above, it is evident that funds investing in similar warehouse and factory rental assets have Dividend Yields ranging from 3.63% to 9.35%.

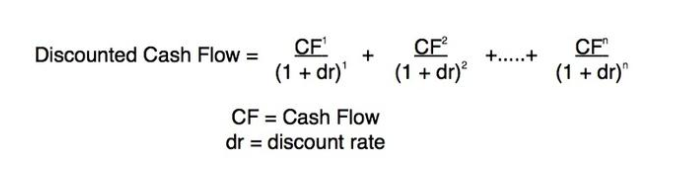

The valuation of Property Funds and REITs should consider the cash flows expected from the investment over the long term throughout the period the fund can lease the properties. Typically, large investors or institutional investors will assess the value of investments in funds using the Discounted Cash Flow method as follows:

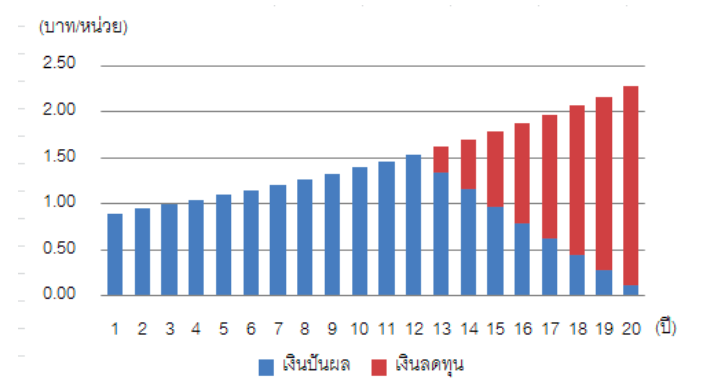

I will provide an example of a Property Fund and REIT that invests in leasehold assets with 20 years remaining and is expected to distribute returns, gradually reducing capital to return principal to unit holders in the last 8 years, as illustrated in the diagram.

By forecasting the cash flows expected over the next 20 years and applying the Discounted Cash Flow method, one can assess the appropriate investment value based on the current net asset value to determine whether the price is higher or lower than the market trading price, aiding in investment decisions. This method reflects a more accurate investment price than merely considering Dividend Yield, assuming the underlying assumptions are close to reality, especially during the COVID-19 situation, where fund profits may vary significantly compared to the past.