When Over 1.4 Million GEN Y Are in Debt, with 7% Being Non-Performing Loans

In an era where “GEN Y over 1.4 million people are in debt, with 7% of the total NPL being non-performing loans”, data from the Bank of Thailand reflects that the GEN Y group (ages 23-38) has 7.2 million borrowers (accounting for 50% of the entire GEN Y population), with an average debt burden of 423,000 baht per person. Notably, 20% of GEN Y borrowers, or 1.4 million people, are in default, which represents 7.1% of all loans that are in default. The interesting aspect of the financial behavior of the GEN Y group is that they have a consumerist attitude—making impulsive purchasing decisions—believing that happiness can be bought through experiences, which leads to the phenomenon of #musthave. In reality, GEN Y has more complexities than you might think.

TMB Analytics, in collaboration with WiseSight (Thailand), studied the financial behaviors of GEN Y using social media data. Through the campaign #musthavebefore40, it was found that most have dreams of building a good and stable future, wanting to own a house, a car, and savings. However, this is in stark contrast to their financial behaviors, which hinder GEN Y from reaching their financial goals due to being trapped in the cycle of purchasing #musthave items.

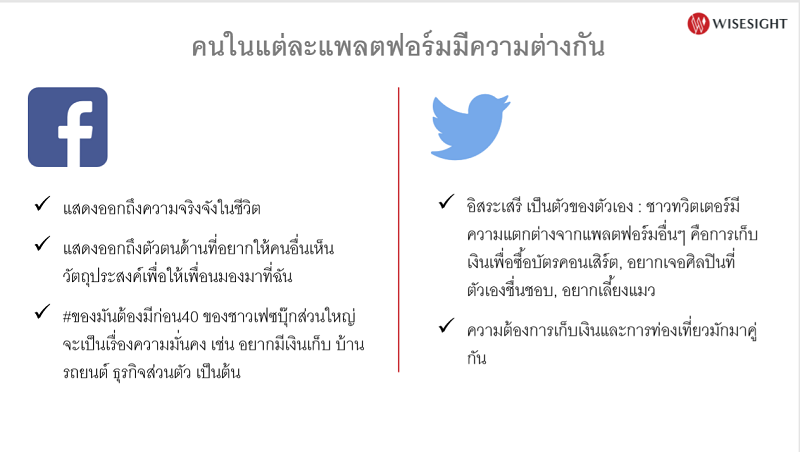

Currently, 74% of the Thai population uses social media, ranking 8th in the world. The most popular social media platforms among Thais today are Facebook, with over 56 million accounts, Instagram with 13 million accounts, and Twitter with 9.5 million accounts. On average, users spend 3 hours and 11 minutes per day on these platforms. Additionally, it was found that 80% of internet users in Thailand have purchased goods online, with over 50% being GEN Y individuals aged 28-38.

Each platform has different user behaviors. For example, Facebook tends to reflect seriousness in life and showcases aspects of identity that users want others to see. Thus, the #musthavebefore40 posts from Facebook users mostly revolve around stability, such as wanting savings, a house, a car, or a personal business. In contrast, Twitter reflects a more free-spirited lifestyle, with users expressing different opinions compared to Facebook, such as saving money for concert tickets, wanting to meet their favorite artists, or wanting to adopt a cat.

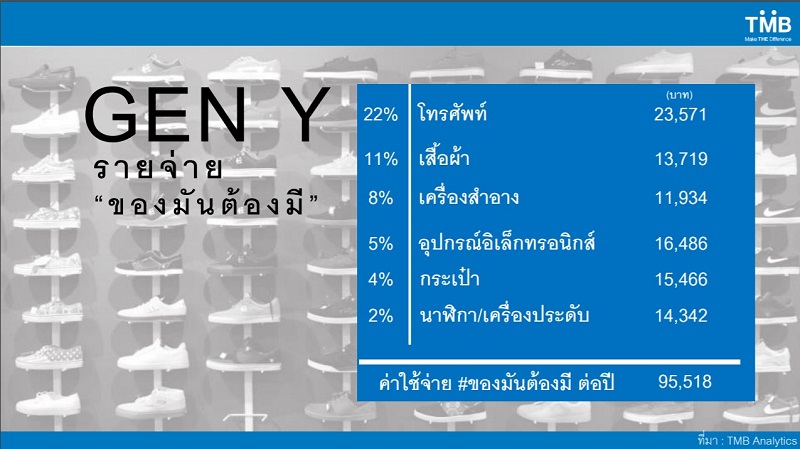

Survey results on GEN Y's social media behavior reveal that their hopes for #musthave before turning 40 include wanting a house (48%), a car (22%), and savings or other assets (13%). However, data analysis shows that GEN Y tends to dream big but fails to achieve those dreams. This is reflected in the fact that GEN Y, when starting their careers, aims to save 6 million baht but only plans to save an average of 5,500 baht per month. At this rate, it would take 90 years to reach their goal. Most GEN Y individuals are trapped in spending on “must-have” items, accounting for 69% of their expenditures, while their dreams of buying a house or car have significantly decreased, and their savings are less than 10%. In monetary terms, GEN Y spends approximately 95,518 baht annually on “must-have” items, which is about one-fourth of their annual income, primarily on phones, clothing, cosmetics, electronics, bags, and jewelry.

The reason GEN Y desires must-have items is largely due to following trends and fearing being left out, with over 42% viewing them as essential compared to 37%. Naturally, when purchasing trendy items, over 70% report not having enough money, leading them to borrow from banks and use credit cards and cash cards for spending. It was found that 74% of GEN Y are making payments with interest, while 26% are not making installment payments, resulting in bad debts.

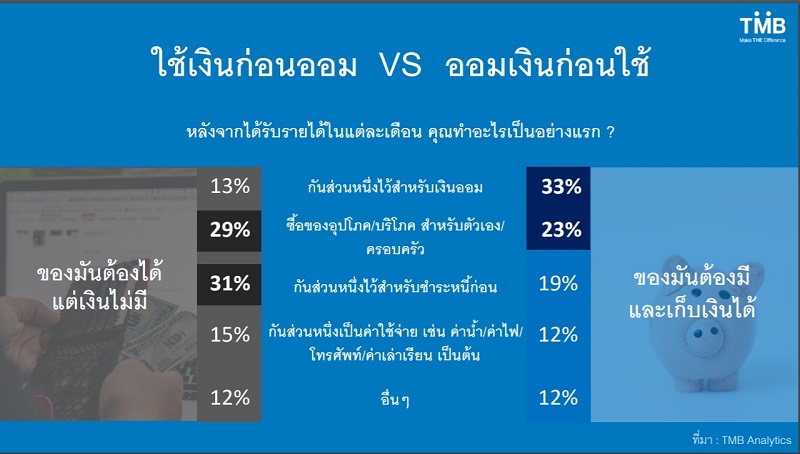

The underlying implications of the spending behavior of “must-have” among GEN Y reveal that over 6.8 million GEN Y individuals have spending behaviors that exceed their savings, with 47% falling into this category. If we delve deeper into the financial structure of GEN Y, we can categorize them into two groups based on their spending behaviors:

- “I want it, but I have no money” - This group prioritizes spending before saving. When they receive their monthly income, they first pay off debts and buy consumer goods (60%), saving the remainder. They often save in the wrong places, keeping large amounts in regular savings accounts.

- “I want it and can save money” - This group behaves oppositely; they allocate a significant portion of their income for savings (33%) before spending, indicating they have financial discipline. They also plan their savings and investments, reflected in having funds in high-interest savings accounts and investing in stocks or other financial instruments, which is a higher proportion compared to the first group.

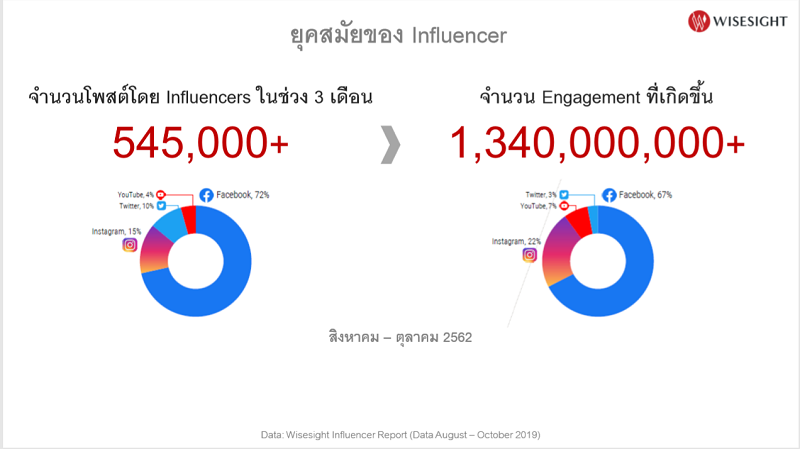

The in-depth behaviors of GEN Y, influenced by various influencers, show that their opinions and shares often align with those of the influencers they follow, making it easy for followers to be swayed. Therefore, when influencers take action, it creates a trend and social voice that encourages imitation. This campaign has sparked questions among GEN Y about their financial goals, leading them to consider better life planning.

The spending behavior of GEN Y is highly individualistic. Therefore, GEN Y must adjust their financial spending habits. If we zoom in on the figures, GEN Y spends approximately 1.37 trillion baht annually on “must-have” items, which is equivalent to 13% of the country's GDP or eight times the value of the high-speed rail project connecting three airports, or 91% of the investment value in the EEC project over five years.

So, what can be done to help GEN Y improve their financial behavior or develop better financial discipline to create financial stability and encourage more savings? The first recommendation is to reduce spending on “must-have” items by just 50% (as reducing it by 100% is likely unrealistic). Alongside this, they should plan their finances better by increasing savings and investing wisely. By doing this, GEN Y could accumulate an additional 43,000 baht per year. Over 10, 20, or even 30 years, they could easily purchase the assets they once hoped for. Mr. Naris concluded with suggestions for GEN Y to effectively plan their finances and achieve their set goals.