New Trends in Bangkok's Commercial Real Estate Market

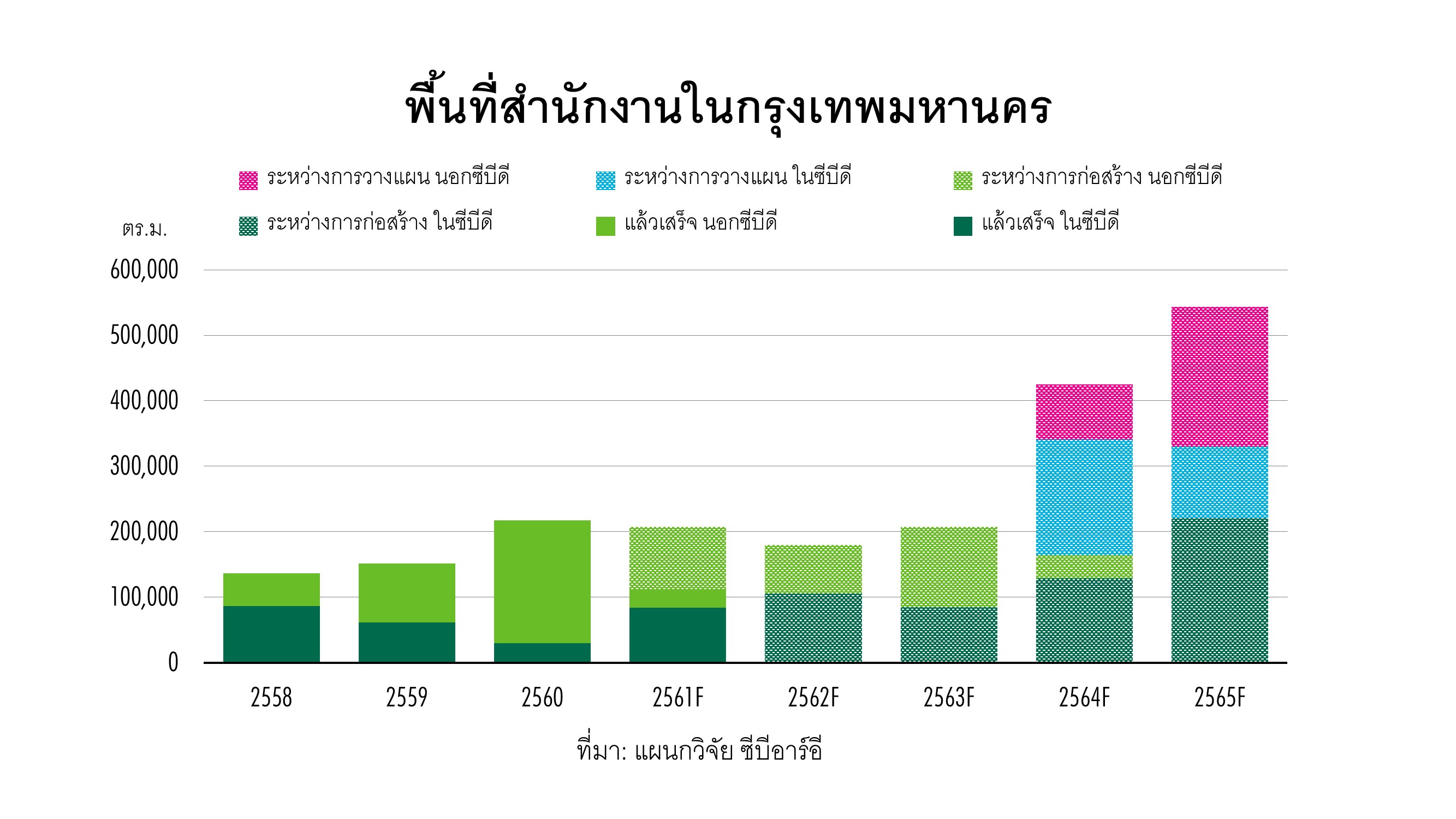

Bangkok, December 3, 2018 – CBRE, a global real estate consulting firm, reports that the office market in Bangkok continues to show positive trends with ongoing demand, resulting in higher rental rates for building owners. In the first nine months of this year, the total office space usage in Bangkok reached 140,000 square meters, and CBRE predicts that overall office space usage in the market will be close to 200,000 square meters by the end of this year.

According to the latest survey from CBRE's research department, there are over 850,000 square meters of new office space currently under construction, scheduled to be completed between Q4 2018 and Q4 2025. More than half of this new office space is located in the Central Business District (CBD), with an additional 1.7 million square meters in the planning stages. CBRE expects further construction of new office buildings in 2019, which will increase the amount of office space completed in 2025 to over 500,000 square meters.

Mr. Nithiphat Thongpan, Head of the Office Space Department at CBRE Thailand, commented, “The trend in the office building market will remain the same, with steady demand for space growing at a rate of 200,000 square meters per year. Rental rates will continue to rise, albeit at a slower pace until 2025, when new office space will exceed average demand. Co-working spaces will become a new source of demand in the office building market, especially in new Grade A office buildings. In the past 18 months, 44,000 square meters have been leased for co-working spaces. The increasing number of co-working spaces will directly compete with traditional office spaces and may lead to a decrease in overall space usage.”

Meanwhile, Thailand's retail business continues to recover in line with economic growth, and consumer confidence is rising. However, the retail space market still faces challenges from declining domestic consumption and rapid changes in global retail business. According to the Bank of Thailand, the retail index in August 2018 was at 275.22, an increase of 17.74% from the same period last year, and the consumer confidence index in August 2018 rose by 9.73% from the previous year. However, household debt remains high at 78% of GDP, affecting consumer spending.

Thailand's retail market continues to face intense competition from new retail spaces and e-commerce. In 2018, there was 200,000 square meters of new retail space from four major projects: Icon Siam, Gateway at Bangsue, the second IKEA at Central Plaza Westgate, and The Marvel Experience Thailand at Mega Bangna. Although macroeconomic indicators show a positive trend, many major retailers report no growth in same-store sales due to slowing domestic consumption.

In the future, retail space in Thailand will continue to grow. As of Q3 2018, there were approximately 1.4 million square meters of retail space under construction and in the planning stages in Bangkok. With increasing competition, the challenge for retail project owners is to adapt their offerings from product sales to creating retail experiences that meet high customer expectations.

According to the Office of Electronic Business Development, Thailand's e-commerce market in 2018 was valued at 3.06 trillion baht. JD Central reports that e-commerce currently accounts for about 3% of total retail sales and is expected to rise to 10% within the next five years. The Bank of Thailand predicts that e-commerce in Thailand is growing faster than expected, but it still only accounts for 2-3% of total retail sales.

“As more consumers prefer to use services through both online and offline channels, store owners need to adopt an omnichannel strategy, offering products through various channels, integrating in-store and online shopping to create a 'shopping experience.' The rapid changes in the retail market indicate that shopping malls need to adapt significantly; otherwise, they will not survive,” said Ms. Jariya Tamtrongkijkul, Head of the Retail Space Department at CBRE Thailand.

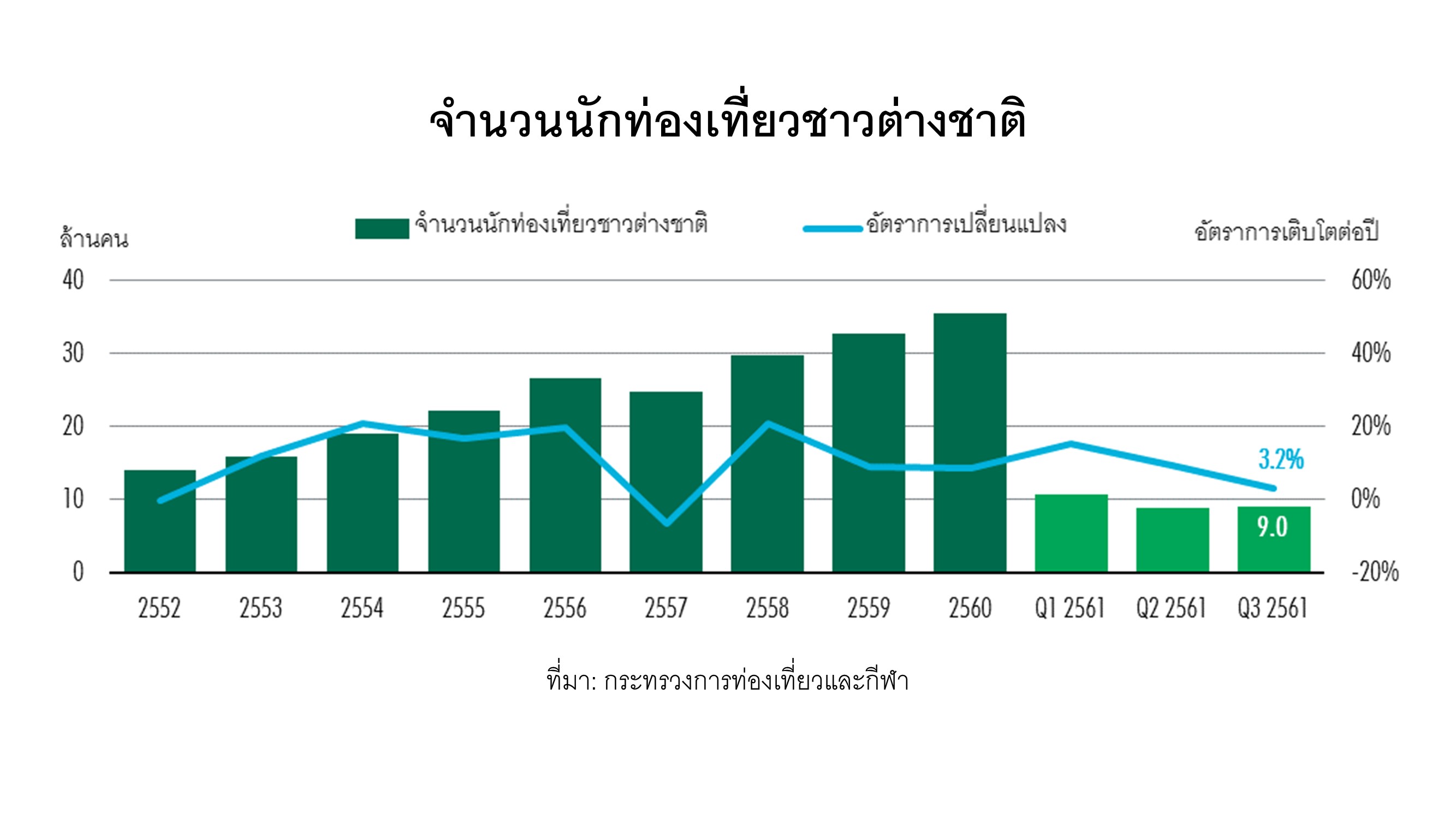

As for Thailand's tourism market, it continues to grow, with China being the largest market, accounting for about 30% of all foreign tourists. After a significant increase in Chinese tourists in recent years, Thailand's service industry is gradually slowing down following the boat capsizing incident in Phuket last July, resulting in an 8.8% year-on-year decrease in Chinese tourists in Q3 2018. However, CBRE believes that Bangkok has been less affected, as evidenced by the number of foreign tourists arriving at Don Mueang and Suvarnabhumi airports, which has not decreased from last year.

Data from STR Global shows that the average occupancy rate of hotels in central Bangkok has remained high since the beginning of the year, currently at 80%. Over the past two years, various hotels have achieved record-high occupancy rates and are confident in raising room rates. In Q3 2018, the average daily rate (ADR) increased by 4.3% year-on-year, while the occupancy rate remained stable. The revenue per available room (RevPAR) also increased, indicating a positive trend in Bangkok's hotel market.

According to a survey by CBRE's research department, by the end of 2018, there will be a total of 46,800 hotel rooms in central Bangkok, an increase of 4.6% from last year. With various projects announcing development plans, CBRE's research department predicts that there will be an additional 11,000 hotel rooms by 2025, bringing the total number of hotel rooms in Bangkok to 58,000, an increase of about 25%. Most of the new rooms will be in mid-range hotels. The challenge remains in attracting Chinese tourists to match the increased number of rooms expected in the near future.

“As Bangkok is the most popular overnight tourist destination in the world, according to Mastercard's 2018 Global Destination Cities Index, we expect to see strong hotel performance in Q4 this year, which is the peak tourist season around Christmas and New Year,” said Mr. Attakavi Chusaeng, Head of the Hotel Business Department at CBRE Thailand.

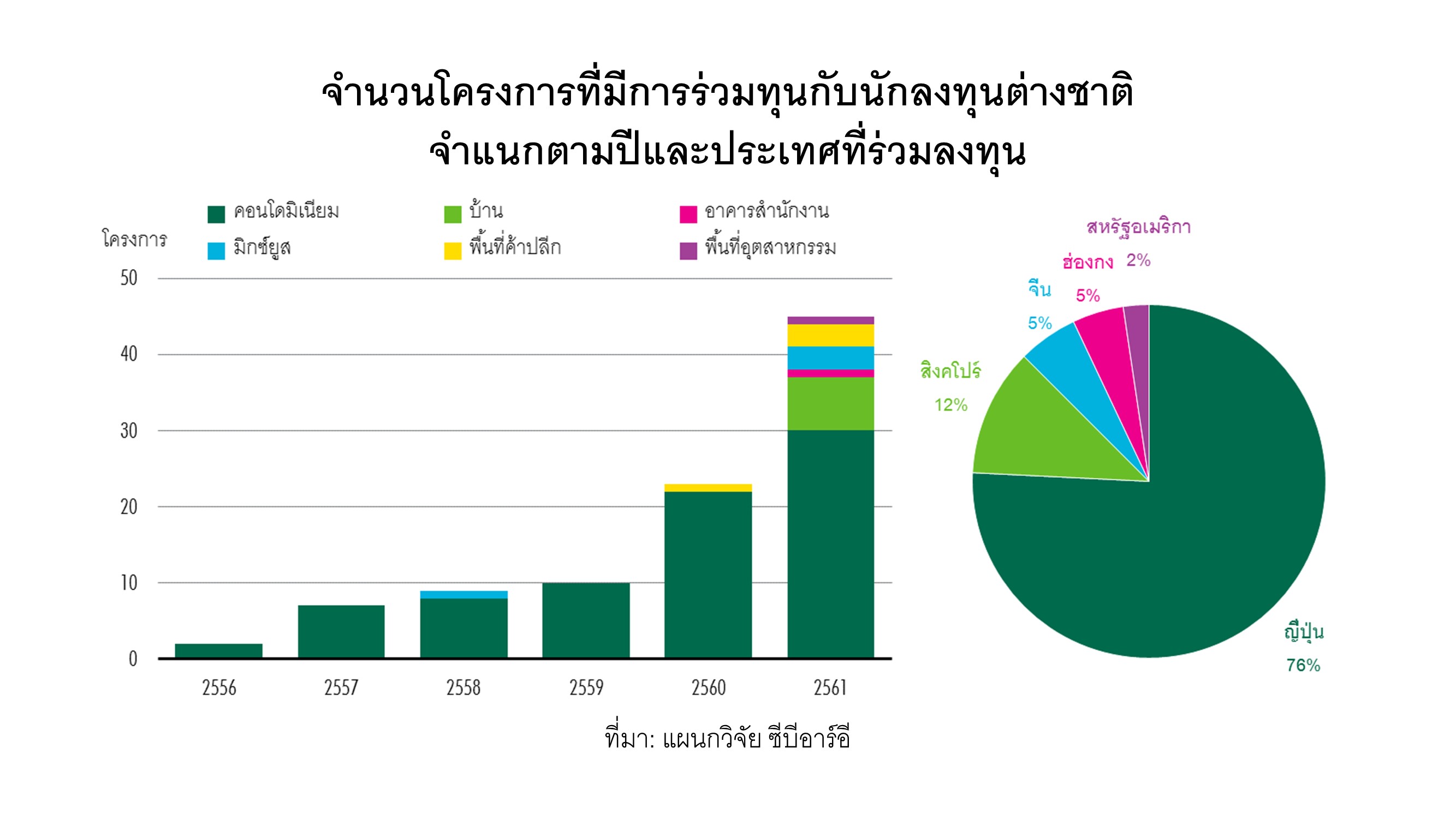

Bank lending for real estate projects remains strict for both developers and buyers. Concerns about increasing housing loan debt have led the Bank of Thailand to lower the loan-to-value (LTV) ratio for second homes to 80-90% and 70% for third homes, which will deter speculators and investors in the real estate market. The strict lending policies of various banks have pushed developers to seek funding from abroad in the form of joint ventures. Since early 2018, there have been more than 15 joint ventures between Thai companies and foreign companies, with at least 75% of these joint ventures involving partnerships with Japanese developers.

Ms. Kunwadee Sawangsri, Head of the Investment and Land Department at CBRE Thailand, added that the demand for freehold land in the city center remains high, but developers are becoming more selective and find it increasingly difficult to accept rising land prices, as land prices directly affect project feasibility. Some developers are turning to leasing land instead, with lease terms of 30 or 50 years, and only a few locations are considered capable of generating sufficient returns within the lease period. Many developers are diversifying their investment portfolios from residential projects for sale to continuous income-generating projects, such as serviced apartments, office buildings, and hotels.

Thank you for the information from www.cbre.co.th