The Internet Bond Market Being Built by Ethereum

This article analyzes the emergence of the Internet Bond, which allows ownership of a platform that will be used by over a billion users to exchange value and receive returns similar to holding bonds.

Ethereum (ETH) currently has a market cap of approximately $207 billion USD, making it the second-largest cryptocurrency after Bitcoin.

Internet Bond by ETH

Before the advent of blockchain technology, we could not receive financial returns from co-owning the internet or from having direct internet users. Internet protocols like TCP/IP are free for everyone to use, which means they do not generate direct revenue for the protocol.

The arrival of blockchain technology and smart contracts has enabled trustless value transfer between parties, allowing users to pay a small fee to cover transaction confirmation and settlement costs (known as gas fees in blockchain terminology). This fee is paid to the system's validators.

This marks the first time we can co-own and earn income from owning blockchain technology that has a large user base, with income derived from the fees paid by users.

Ethereum and the Internet of Money

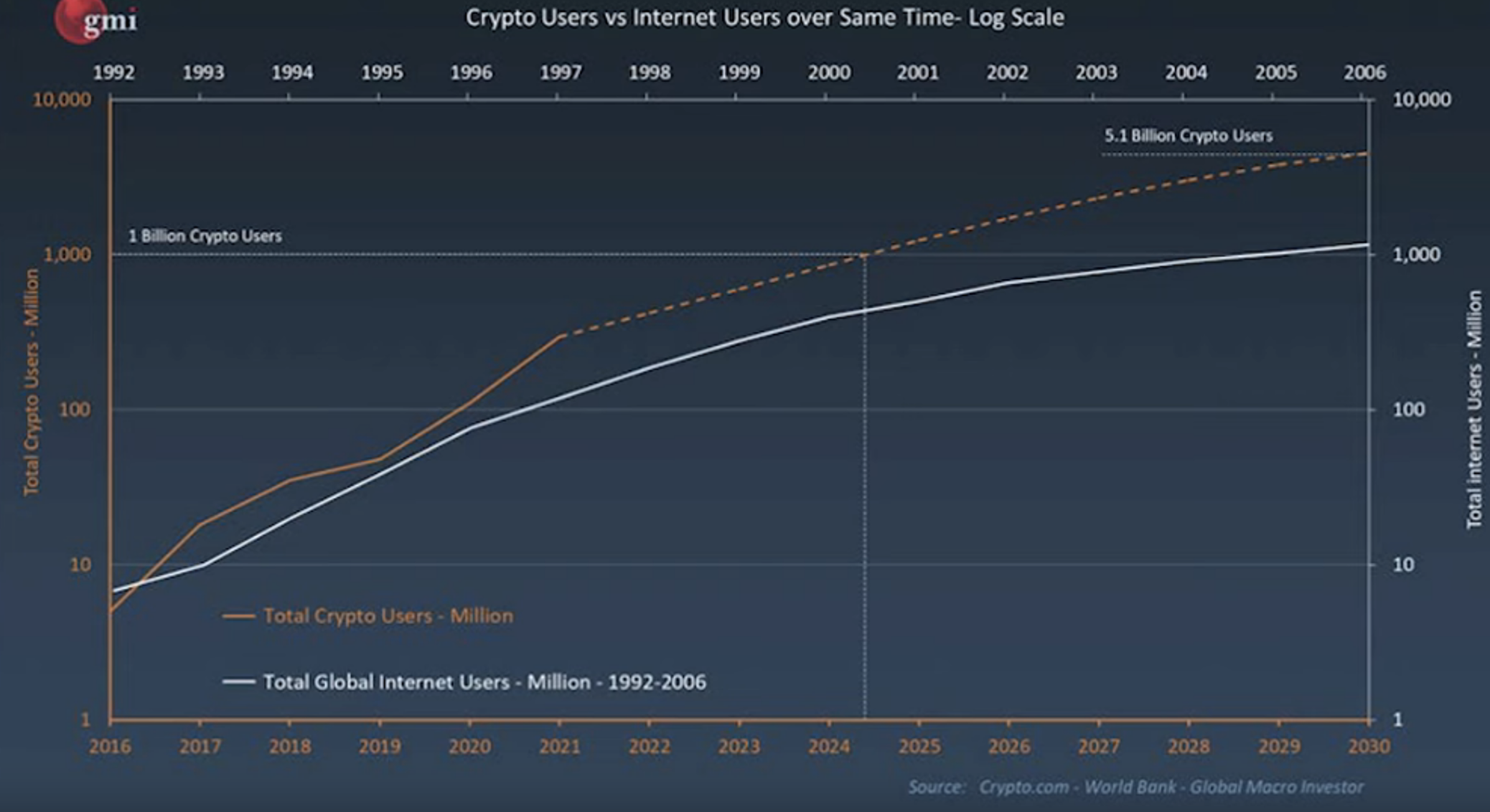

The growth of cryptocurrency users from 2016 to the present is remarkably similar to the growth of internet users from 1992 to 2006. The emergence of network effects (more users increase the network's value) has created a platform condition, meaning that as more users join, it attracts developers to create more websites, programs, or applications, which in turn attracts even more users.

It is predicted that cryptocurrency users could reach as many as 5.1 billion by 2030.

Figure 2: Growth of Cryptocurrency Users Compared to Internet Users

Source: Real Vision Finance / Youtube

Thus, Ethereum acts like the Internet of Money or a network for exchanging value (compared to the internet, which is a network for exchanging information).

ETH Staking Industry

At this point, we must discuss Ethereum Staking, which involves staking Ethereum to become a validator for the system, akin to Proof-of-Work mining in Bitcoin, which is being a validator for Bitcoin. In Ethereum, this is referred to as Proof-of-Stake, and those who stake their assets (Stakers) receive Ethereum as a reward.

(For more details, visit https://ethereum.org/en/staking/)

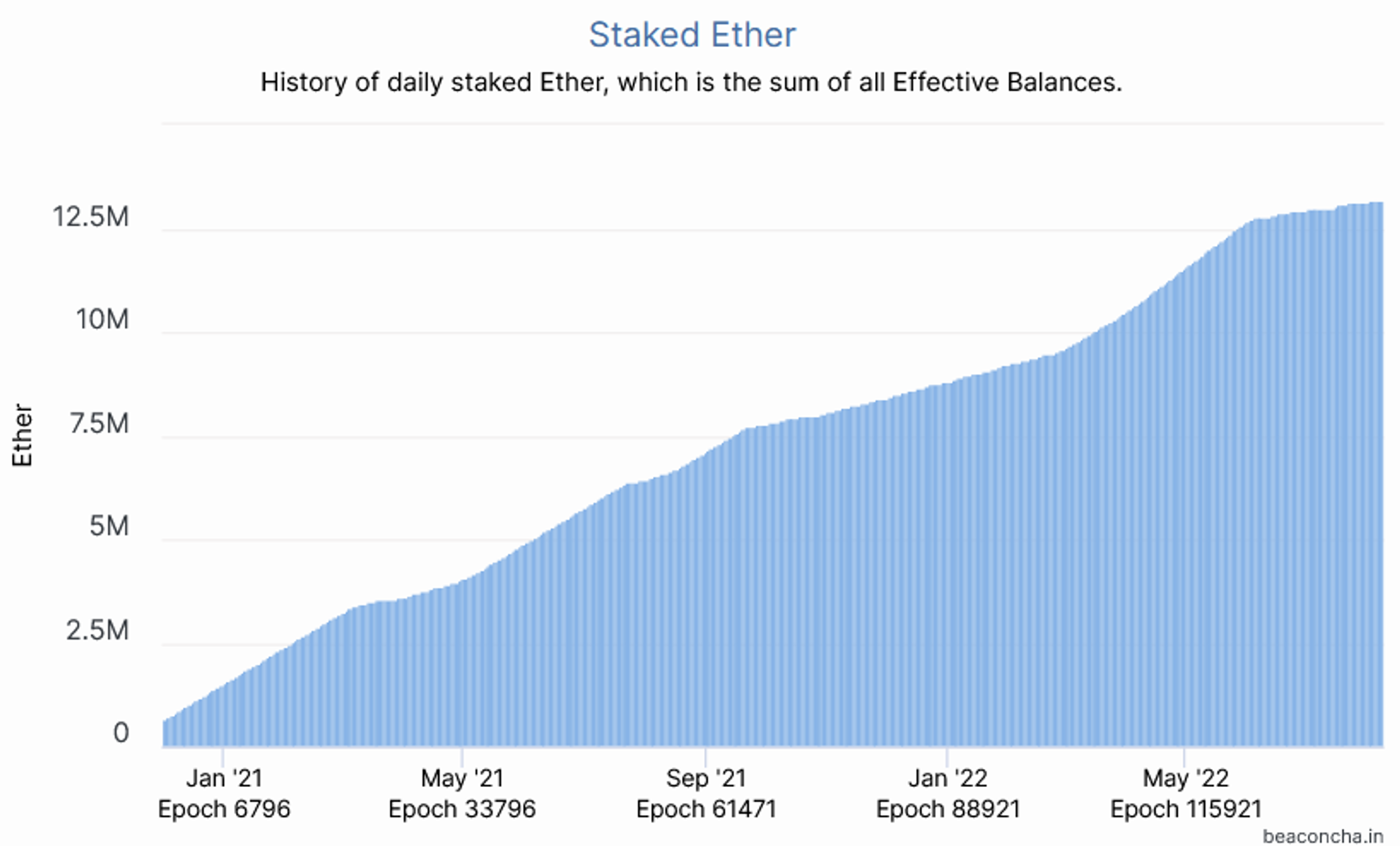

Since staking began on December 1, 2020, 13.9 million ETH have been staked, valued at approximately $24 billion USD, representing 12% of the total Ethereum supply, currently yielding about 4.2% annually (paid in ETH).

However, staked ETH cannot be withdrawn until the system undergoes an upgrade (Shanghai upgrade) after The Merge (when ETH transitioned to 100% Proof-of-Stake, expected in September 2022). This issue has been partially resolved through liquid staking (details in the next section regarding staking options).

(For more on The Merge: https://www.terrabkk.com/articles/201356)

(For more on the Ethereum timeline, visit https://ethereum.org/en/upgrades/merge/)

Figure 1: Amount of ETH Staked in the System

Source: beaconcha.in

In comparison to the traditional government bond market:

ETH Stakers are investors in internet bonds = investors in government bonds.

The Ethereum network issues bonds and owns the system = the issuer of bonds like the government in the case of Treasury and is both the borrower (and pays interest) simultaneously, as the government generates income from taxes and pays some of it as interest to bond investors.

Ethereum network users who pay gas fees = citizens of that country who pay taxes to the government, receiving benefits such as national defense, road use, public park access, etc.

Various Options for Staking ETH

Currently, there are various service providers, and those wishing to stake ETH can choose from the following:

1. Solo Staker

This involves staking on your own, with a minimum stake of 32 ETH, requiring the ability to set up a validator node and maintain it online and functioning properly (otherwise, you may incur penalties known as slashing).

Advantages:

- Self-managed, no trusted parties involved.

- No fees deducted.

Disadvantages:

- Requires knowledge to operate and continuous maintenance after installation.

- Cannot withdraw until the Shanghai upgrade (at least another year).

- Requires a minimum capital of 32 ETH.

2. Centralized Operators

Operated by centralized exchanges like Coinbase, Kraken, or Binance.

Advantages:

- Simple, provided by centralized exchanges.

- No minimum of 32 ETH required.

Disadvantages:

- Must trust the centralized exchange to perform effectively and not make mistakes leading to penalties (slashing).

- Fees deducted, approximately 10-15%.

- Cannot withdraw until the Shanghai upgrade.

3. Liquid Staking Providers

Operated by companies established specifically for staking services, such as Lido, RocketPool, and StakeWise.

When someone stakes ETH, a token is issued to represent ownership in the staked ETH, which can be sold or used as collateral in DeFi.

Advantages:

- Simple, with service providers available.

- No minimum of 32 ETH required.

- Receives tokens representing ownership of the staked ETH (can be sold or deposited in DeFi).

Disadvantages:

- May have smart contract risks or be subject to hacks.

- Service providers may make errors leading to penalties (slashing).

- Fees of 10-15% apply.

- Even if withdrawable (by selling tokens), there is no guarantee on the selling price, which may be lower than expected.

Figure 3: Ethereum Staking Platforms

Source: Moralis Academy

Why Internet Bond (ETH) is Attractive

1. High yield compared to US Treasury.

The yield from ETH Staking is currently at 4.2% and is expected to rise to 6-8% after The Merge is completed in September 2022, as some transaction fees will be redirected to stakers (previously paid to Proof-of-Work miners).

In comparison, the current yield on a 10-year US Treasury is approximately 2.8%.

2. Institutional investors prefer assets with yield over those without, such as gold or bitcoin.

3. The yield is generated directly from the protocol, eliminating the risk of non-payment compared to other lending forms where borrowers may default.

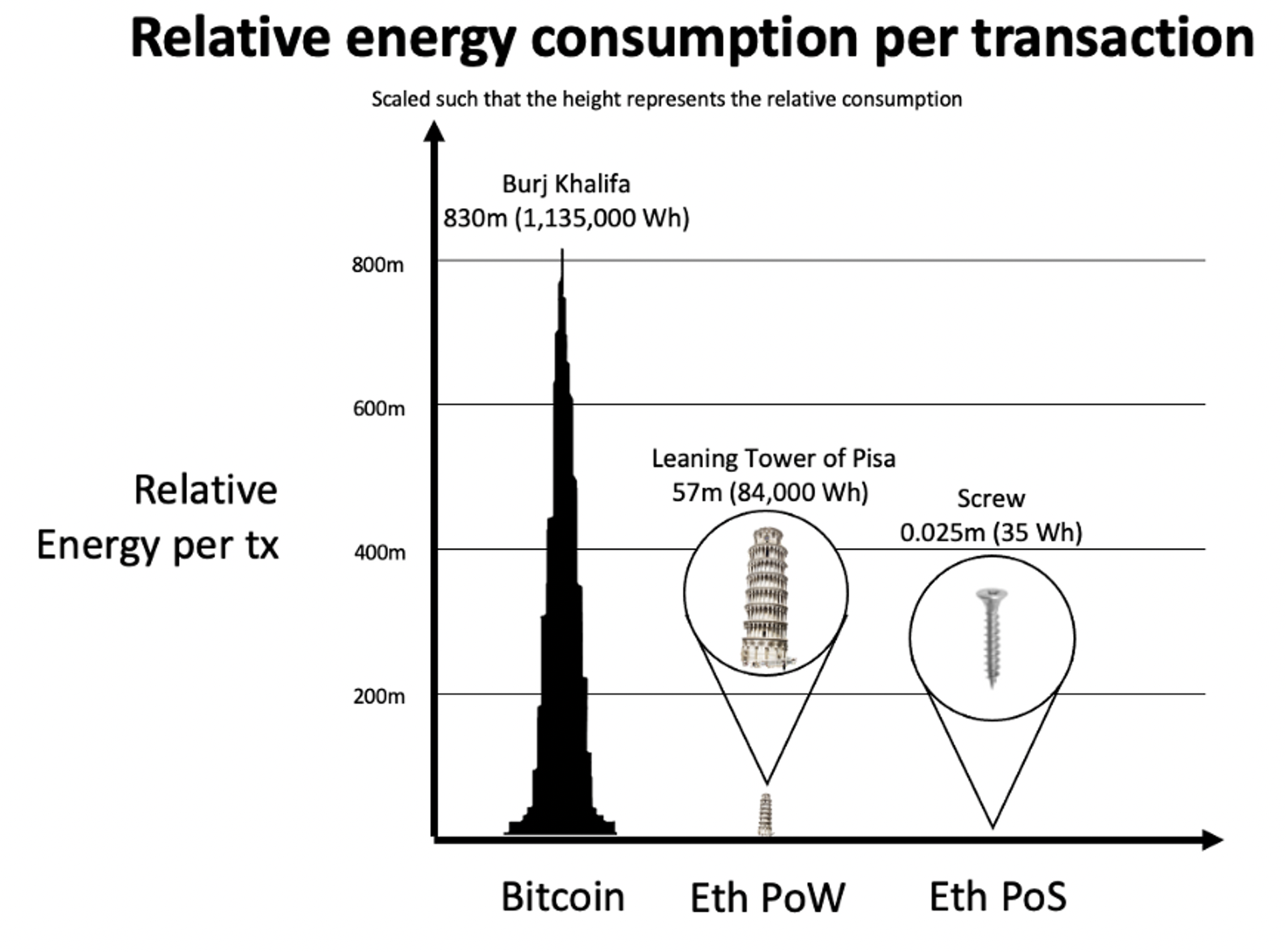

4. The Ethereum network will become environmentally friendly, as it reduces energy consumption by over 99.5%, making it easier for companies or funds with ESG mandates to invest.

Figure 4: Comparing energy consumption of networks; if Bitcoin consumes energy equivalent to the height of the tallest building in the world (Burj Khalifa), Ethereum Proof-of-Stake consumes energy equivalent to the height of a single screw.

Source: Lincoln Murr

5. Potential upside from rising ETH prices.

(For more on how The Merge will affect ETH demand/supply: https://www.terrabkk.com/articles/201356)

Risks of Internet Bond by Ethereum

Ultimately, we must consider the risks involved, as the Internet Bond by Ethereum carries significant risks as well.

1. Volatility of ETH prices

As seen from past cycles, price drawdowns from peak levels of 80-95% are common. For example, from 2017 to 2019, ETH dropped from $1,450 to around $80, and from 2021 to 2022, it fell from $4,800 to about $800.

2. The Merge may fail

While the risk is low, there is a chance that The Merge may not succeed or may be delayed. Currently, it is expected to occur in September 2022, or there may be bugs in the code that prevent the network from functioning.

3. Delay in the Shanghai upgrade

Staked ETH cannot be withdrawn until the Shanghai upgrade, which may take another year and could be delayed further.

4. Issues with the staking platform we choose

For instance, bugs in smart contracts may lead to hacks or errors resulting in penalties (slashing), causing a loss of some ETH.

Conclusion

The emergence of the Internet Bond allows us to co-own a platform with hundreds of millions or even billions of users while generating returns from ownership.

The Ethereum blockchain and smart contracts facilitate value exchange over the internet without intermediaries, marking another significant financial transformation in the internet era through ETH Staking.