Are Property Funds and REITs Attractive Amid Inflation and Rising Interest Rates?

Currently, as the COVID-19 pandemic situation improves, people around the world are beginning to return to business activities and normal life, leading to a positive trend in the overall economy, particularly in developed countries like the United States and Europe, which have high vaccination rates. The real estate sector has also benefited from the economic recovery, as reflected in the returns of the global income-generating real estate index (FTSE EPRA NAREIT Global Real Estate), which yielded a return of 23.0% in 2021.

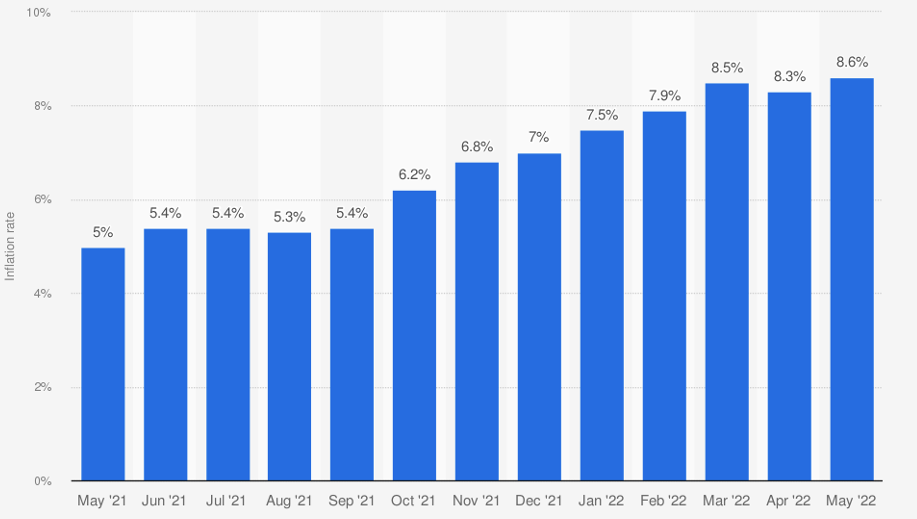

During the COVID-19 pandemic, the Federal Reserve (Fed) implemented monetary measures to support the economy by lowering the policy interest rate to 0 – 0.25% and injecting liquidity into the economy through Quantitative Easing (QE). Coupled with the ongoing war between Russia and Ukraine, inflation in the United States has continued to rise, reaching 8.6% in May 2022, significantly above the target inflation rate of 2.0%.

Table 1: Monthly Inflation Rates in the United States from May 2021 to 2022

Source: U.S. Bureau of Labor Statistics

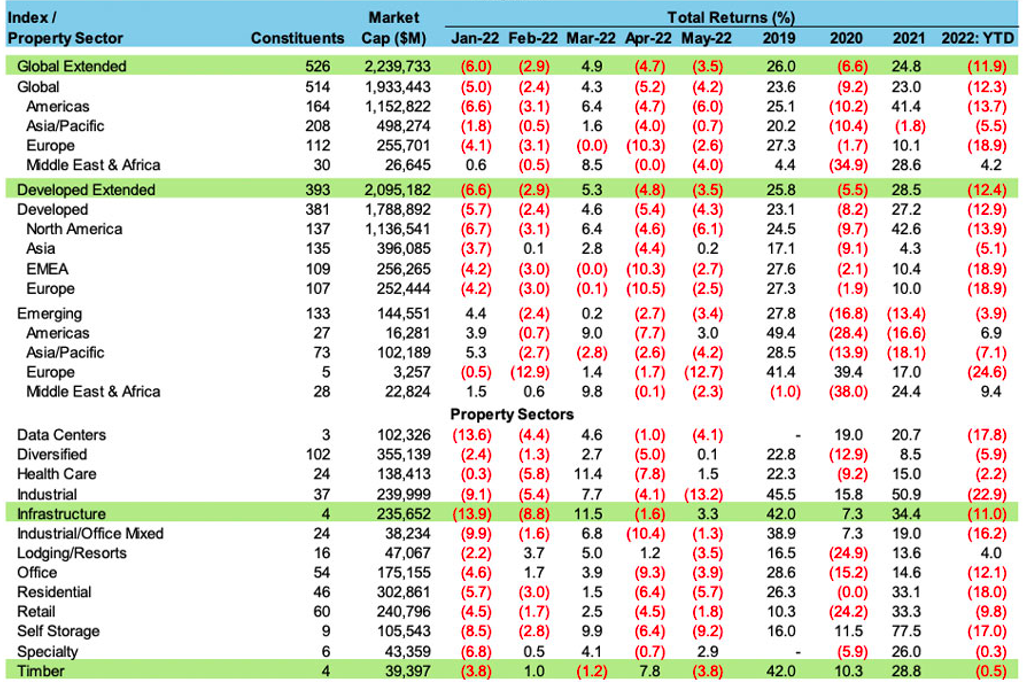

To control inflation, which has reached its highest level in 40 years, the Fed has raised policy interest rates and reduced the money supply, putting the economy at risk of slowing down. This has contributed to the FTSE EPRA NAREIT Global Real Estate index yielding a return of -12.3% in the first five months of 2022, with returns in the Americas and Europe at -13.7% and -18.9%, respectively, due to high inflation.

Table 2: Summary of FTSE EPRA NAREIT Global Real Estate Index Returns in May 2022

Source: FTSE Russel, EPRA, and NAREIT

In Thailand, although the COVID-19 situation is beginning to ease, with the government designating COVID-19 as an endemic disease and lifting mask mandates in open areas, the country is still in a phase of business recovery. It is anticipated that the Bank of Thailand will likely raise the policy interest rate to 0.75% in the third quarter of 2022 from the current rate of 0.5%, which has been in place since the onset of the pandemic, to control rising inflation. In May 2022, inflation was recorded at 7.1%, driven by rising food and energy prices, exceeding the target inflation rate of 1 – 3%.

At this point, one might wonder how investments in Property Funds and REITs will trend in 2022. Will they yield -13.7% like in the Americas? Certainly, the increase in the Bank of Thailand's policy interest rate will impact market interest rates and the returns investors expect to compensate for the increased risks in high-risk assets, potentially affecting the trading prices of Property Funds and REITs. However, if inflation decreases due to the easing of the war between Russia and Ukraine, market interest rates may rise moderately, having a limited impact on investments in Property Funds and REITs. Additionally, the returns of Thai Property Funds and REITs have not yet recovered significantly, with a return of 5.1% in 2021, recovering from a return of -22.8% in 2020, indicating a low downside risk. In the first five months of 2022, the returns of Property Funds and REITs stood at -4.1%, reflecting some negative factors already.

It is important to remember that the investment assets of Property Funds and REITs are real estate, which has the advantage of serving as an inflation hedge if rental prices can be adjusted upwards. If Property Funds and REITs can increase operational profits, they may offset the rising required returns. However, the ability to adjust rents varies by property type, influenced by several factors:

- Different Recovery Directions for Various Property Types: For instance, retail spaces largely depend on domestic customer usage, allowing for quicker rent adjustments compared to hotels that rely on international tourists.

- Different Competitive Landscapes for Various Property Types: For example, the supply of office buildings in Bangkok is likely to increase more than rental demand, unlike rental warehouses where supply and demand are more balanced, limiting the ability to raise rents for office buildings compared to the past.

- Timing of Rent Adjustments: Generally, property leases last for three years, meaning that even if inflation rises, rent adjustments cannot be made immediately; they must wait until the lease expires to negotiate new rental rates, except for leases tied to tenant performance, such as retail spaces often having leases based on gross profit shares or hotels having variable leases based on net operating income.