Preliminary Hotel Valuation #2

After understanding the key terms that affect hotel valuation from the previous article, this article will delve into the details of the valuation calculation.

The income approach is the most widely accepted method for hotel valuation (Rushmore and deRoos, 1999). Since hotels generate income from rental fees over several years, the technique used in conjunction is to estimate the future cash flows of the business, including revenues, expenses, and potential renovation costs, and then discount them back to present value using a specified discount rate. This method is known as discounted cash flow (DCF). Estimating future cash flows requires knowledge of the hotel's historical data, ideally for at least the past five years, to observe the growth in sales prices, expenses, and occupancy rates.

Example

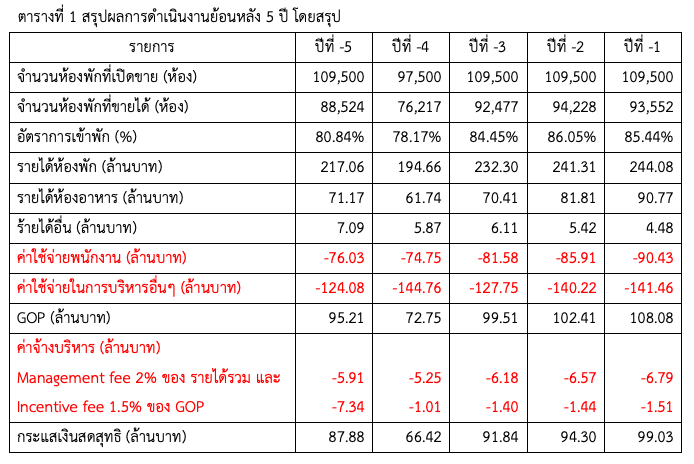

A hotel with 300 rooms, 15 years old, with freehold ownership of land and building, last renovated about 8 years ago, has operational results for the past 5 years summarized in Table 1 (with the current year designated as Year 0).

The data in the table can serve as important assumptions for preliminary valuation as follows:

- Revenue structure

- Room revenue accounts for approximately 72% to 75% of total revenue.

- Food and beverage revenue accounts for approximately 23% to 27% of total revenue.

- Other revenues account for approximately 2% to 3% of total revenue.

- The annual occupancy rate is approximately 80% to 85% of total available rooms.

- Room revenue is estimated at around 200 to 245 million baht per year, with the last two years not falling below 240 million baht. Therefore, combined with the occupancy rate, this hotel is expected to have an ADR (average daily rate) of approximately 2,600 baht/room/night, with a growth rate of about 2% per year.

- The operating profit margin is approximately 28% to 32%.

- Employee wages, which are fixed costs, were approximately 90 million baht in the most recent year, with a growth rate of about 5.5% per year.

- Since the hotel was last renovated about 8 years ago, renovation costs should also be considered.

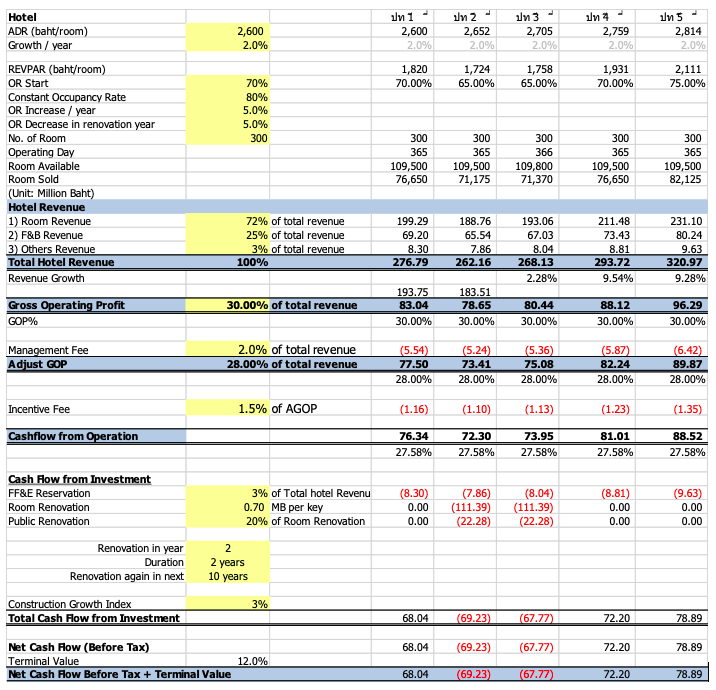

The next step is to use all the data to estimate the future cash flows of the business, both cash inflows and outflows, as shown in Figure 1, which provides a snapshot of the estimated cash flows over the next 5 years. It can be seen that the initial ADR is set at 2,600 baht/room/night, with a conservative occupancy rate of 70% in the first year, gradually increasing to a stable rate of 80% per year. Additionally, in the year of room renovations, the occupancy rate is reduced by 5% from the previous year. The revenue and expense structure still references past performance. However, the renovation assumptions provided are merely estimates; a thorough investigation is necessary to obtain accurate data for valuation calculations.

Figure 1: Estimated future cash flows for Years 1-5

Furthermore, in valuing a hotel or any asset or business that generates recurring income, in the case of freehold, it is necessary to determine a value that assumes the business continues indefinitely (perpetual), known as Terminal Value. Conversely, if valuing a leasehold hotel, calculating Terminal Value is not necessary.

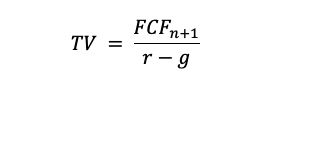

The formula for Terminal Value is as follows (Magnimetrics, 2021)

Where:

TV = Terminal Value

FCF = free cash flow

n = year at the end of the calculation

r = discount rate

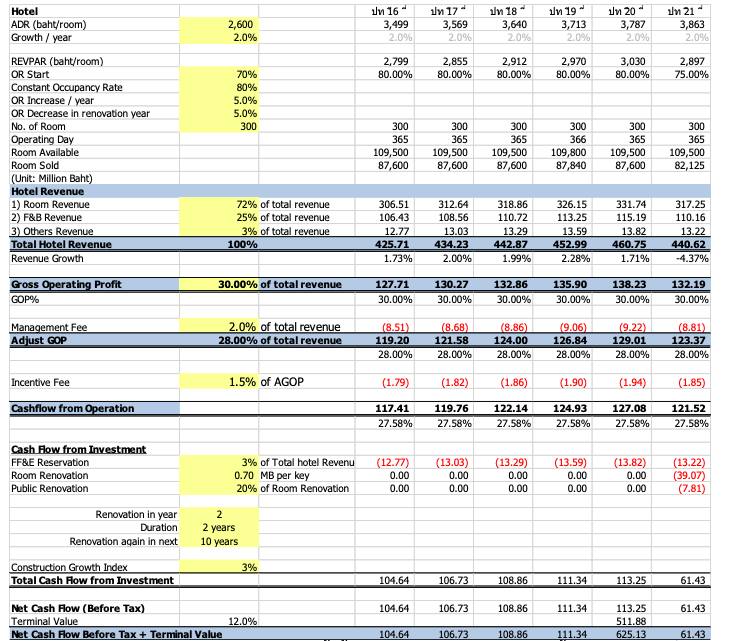

Figure 2: Estimated future cash flows for Years 16-20

In this valuation, the calculation is based on a 20-year timeframe. Therefore, the cash flows used to calculate Terminal Value must be calculated from Year 21. In Year 21, renovation costs are included, even though it may not yet be time for hotel renovations. This is to ensure that the calculated Terminal Value reflects the necessary future renovations; otherwise, the calculated value would be unrealistically high. The principle for including renovation costs is to calculate an average annual renovation cost. For example, if renovations are expected every 10 years at a cost of 100 million baht, then 10 million baht is included. In the case of the figures shown in Figure 2, the amounts of approximately 39.07 million baht and 7.81 million baht result from calculating the renovation cost per room at 700,000 baht, adjusted for a 21-year construction cost growth rate, divided by a 10-year period (700,000 x 1.03^21 / 10 = approximately 39.07 million baht), plus an additional 20% for common area renovations.

When combined with the cash flow in Year 21, it amounts to approximately 61.43 million baht (which is FCFn+1 from the Terminal Value calculation formula). This value is then divided by r-g, where r (discount rate) is set at 15% and growth at 2% (based on the expected growth rate of room prices). Thus, the Terminal Value equals 61.43 / 13% = 472.51 million baht. This value is then added to the estimated cash flows for each year. However, sometimes this Terminal Value may also represent the estimated future sale value of the business.

The cash flows from Year 1 to Year 20 are then used to calculate the NPV (Net Present Value) at Year 0 using the specified discount rate (15%), resulting in an estimated hotel value of approximately 293.16 million baht or about 0.98 million baht per room. The estimated value in this example is before corporate income tax, so it does not account for depreciation of the building and related equipment, net profit, and income tax payable each year, as well as any accumulated losses that may exist.

Another important point that significantly impacts the estimated hotel value is the discount rate. If the discount rate decreases, the hotel value increases, and conversely, if the discount rate increases, the hotel value decreases, or the hotel must be purchased at a lower price to achieve a higher return. This is illustrated in Table 2.

Table 2: Changes in hotel value with different discount rates

Finally, I would like to emphasize that all the examples described are based on hypothetical data. Therefore, in actual hotel valuation, it is crucial to gather reliable and accurate data to use as assumptions in the calculations, as well as to determine an appropriate discount rate based on individual circumstances.

For more in-depth details, there is a course on the feasibility study of real estate projects in the Master of Science program in Real Estate Development Innovation at the Faculty of Architecture and Planning, Thammasat University.

References

Rushmore, S. & deRoos, J. (1999). Hotel Valuation Techniques. Hotel Investments Issue & Perspectives, USA, Education Institute of the American Hotel & Motel Association.

Magnimetrics. (2021). What is Terminal Value?. Retrieved from https://magnimetrics.com/terminal-value-of-the-business/ on September 10, 2021.