Decoding Consumer Insight: The Tangible Wellness Blueprint - A Strategy to Transform Housing Opportunities

In the highly competitive real estate business landscape, where economic conditions are fraught with challenges, a deep understanding of consumers is key to success and sustainability. TerraBKK.com, as a business research and real estate media consultant, recognizes the need to elevate standards and perspectives in the industry. Thus, it has organized the grand annual seminar TERRAHINT BRAND SERIES 2025 for the 8th time, under the main theme "The Wellness Blueprint #QualityLiving".

This seminar is not just a platform for exchanging business views but also a significant turning point in pushing housing development beyond traditional limits towards creating a better quality of life for people at all levels, offering consumers an experience that transcends mere living.

One of the highlighted topics of the seminar every year is "Consumer Insight: Understanding Modern Consumers through a Wellness-Centric Perspective to Build Strong Brands", presented by Ms. Sumitra Wongphakdee, Managing Director of Terra Media and Consulting Co., Ltd., who revealed research findings on BUILDING STRONGER BRANDS THROUGH WELLNESS INSIGHT.

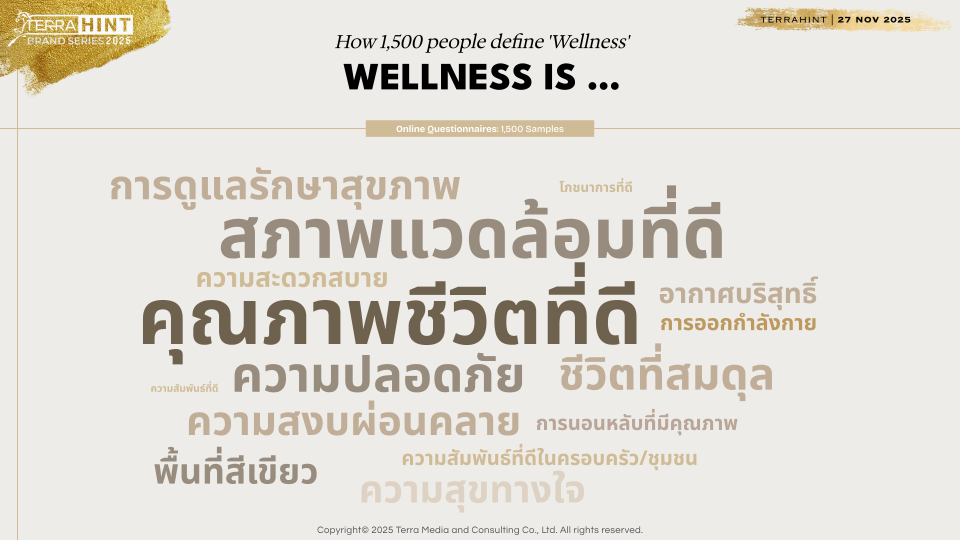

This year, we gathered in-depth insights from over 2,000 respondents, with 75?ing residents of Bangkok and its vicinity. The research unveiled significant changes in the attitudes and values of Thai consumers, particularly in how they define and prioritize the concept of "Wellness," which has unprecedented influence on real estate purchasing decisions.

Defining Wellness from the Perspective of Modern Consumers

Interestingly, the research shows that most Thais clearly define "Wellness" in alignment with fundamental life factors, namely "good quality of life, a good environment, and safety." This reflects that environmental factors have consistently been a top priority when seeking housing.

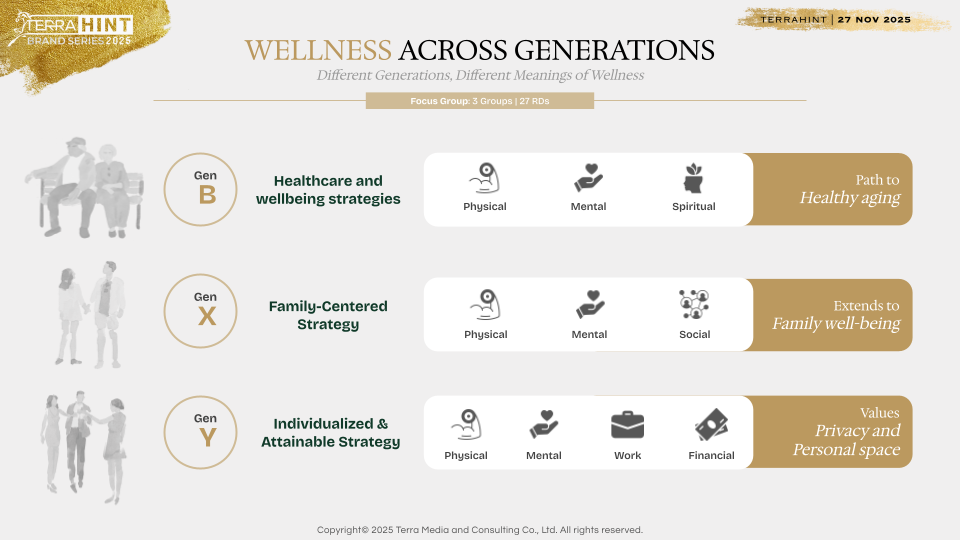

However, the context of the term "Wellness" is not static; it "changes according to life experiences and responsibilities at different ages." For example:

- Baby Boomers: Wellness is the balance of body and mind, a holistic view encompassing all aspects of life.

- Gen X: Wellness is the balance of body, mind, relationships, and family life. As this group is in the workforce and has multiple roles, they see Wellness as a balance between physical, mental, social, and environmental dimensions, considering family as well.

- Gen Y: Wellness is a holistic balance for oneself, covering physical, mental, work, and financial dimensions. They view Wellness not just as health but as inner peace, mental well-being, good social relationships, and the energy to pursue personal desires.

This presents a new challenge for marketers and real estate developers to deeply understand and design products and services that accurately meet specific group needs.

"We are no longer just selling bricks and mortar; we are selling a good quality of life and the assurance of building a secure future for consumers. This is the opportunity to transform economic challenges into sustainable growth for the real estate industry."

The insights shared by TerraBKK are therefore crucial for entrepreneurs, investors, and marketers seeking new strategies to build strong and sustainable brands in an era where consumers prioritize wellness and quality of life. This forms the essential foundation for delving into the second part, which will explore consumer behavior and needs across various dimensions.

Changing Social Context: Single, Divorced, and Not Wanting Children

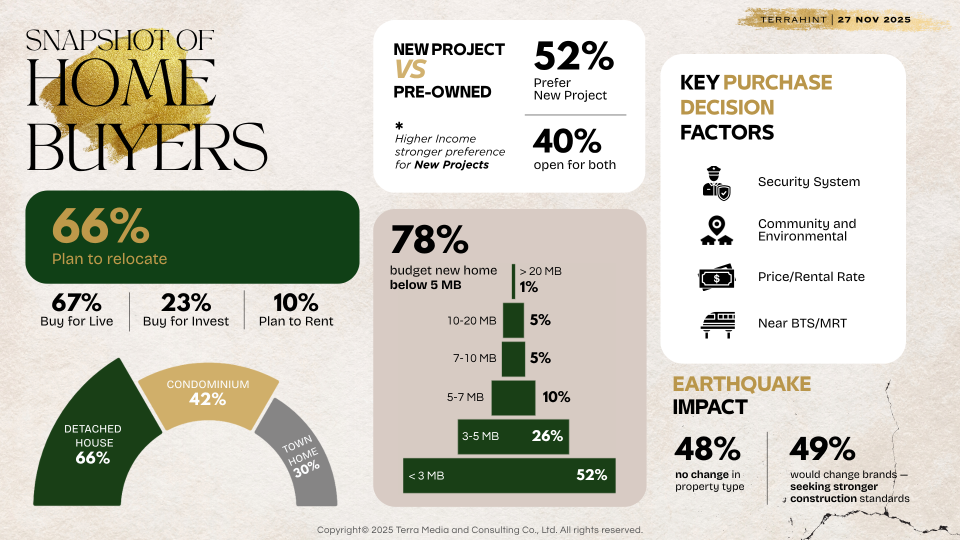

Before diving into Wellness, it is essential to understand the demographic structure and the surprisingly changing purchasing decision behaviors, particularly regarding marital status and childbearing. Research indicates that the proportion of people who are "single or divorced" has surged to 60%, while those who "do not have children and do not want children" account for 46%. These figures clearly signal a social and family structure change towards smaller sizes.

"As the number of consumers decreases due to the trends of being single and divorced, as well as not wanting children, it means that competition in the real estate market will intensify. We can no longer rely on population growth; we must focus on the existing market and truly understand their specific needs."

Despite criticisms that younger generations may shift towards renting instead of buying, research confirms that only "6% plan to rent exclusively without buying." This indicates that the desire for property ownership remains, but purchasing decisions will be more complex and involve more criteria.

Buying Behavior by Project Type

The real estate market still has a large interest group in "single-family homes," followed by condominiums and townhomes. The majority of purchasing budgets remain in the mid to lower range, with the market for properties priced over 20 million baht still accounting for only 1% as before.

Interestingly, this year, interest in "townhomes" has significantly increased, which may signal a positive trend for the Middle-to-Low market. There is a growing desire to own housing or seek space that better meets personal living needs compared to condominiums, especially after the economic crisis when concerns about purchasing property began to fade.

Factors influencing purchasing decisions have intensified, including: 1. Smart security systems and living in a good community 2. Good prices 3. Proximity to public transport (BTS), which had diminished in importance over the past 2-3 years but has regained significance.

Specific Insights by Project Type

- Single-family homes: Buyers focus on quality materials and value following social media information related to home improvement, reflecting a desire for long-term living and personal space adaptation.

- Condominiums: Brand reputation is crucial, as consumers believe that strong brands facilitate easier and quicker resale or rental. This group of buyers is also interested in technology and electronics content.

- Townhomes: A clear shift in demand is evident, as buyers no longer view townhomes for business purposes as in the past but seek more usable space for personal living without the burden of maintaining a large single-family home. Importantly, they are looking for health and wellness and life services, indicating a transition from commercial housing to wellness-focused living.

Understanding Consumer Spending through 6 Financial Lifestyle Groups

Additionally, the survey categorized consumers based on spending behavior, revealing clear differences in needs. The six main groups of interest are:

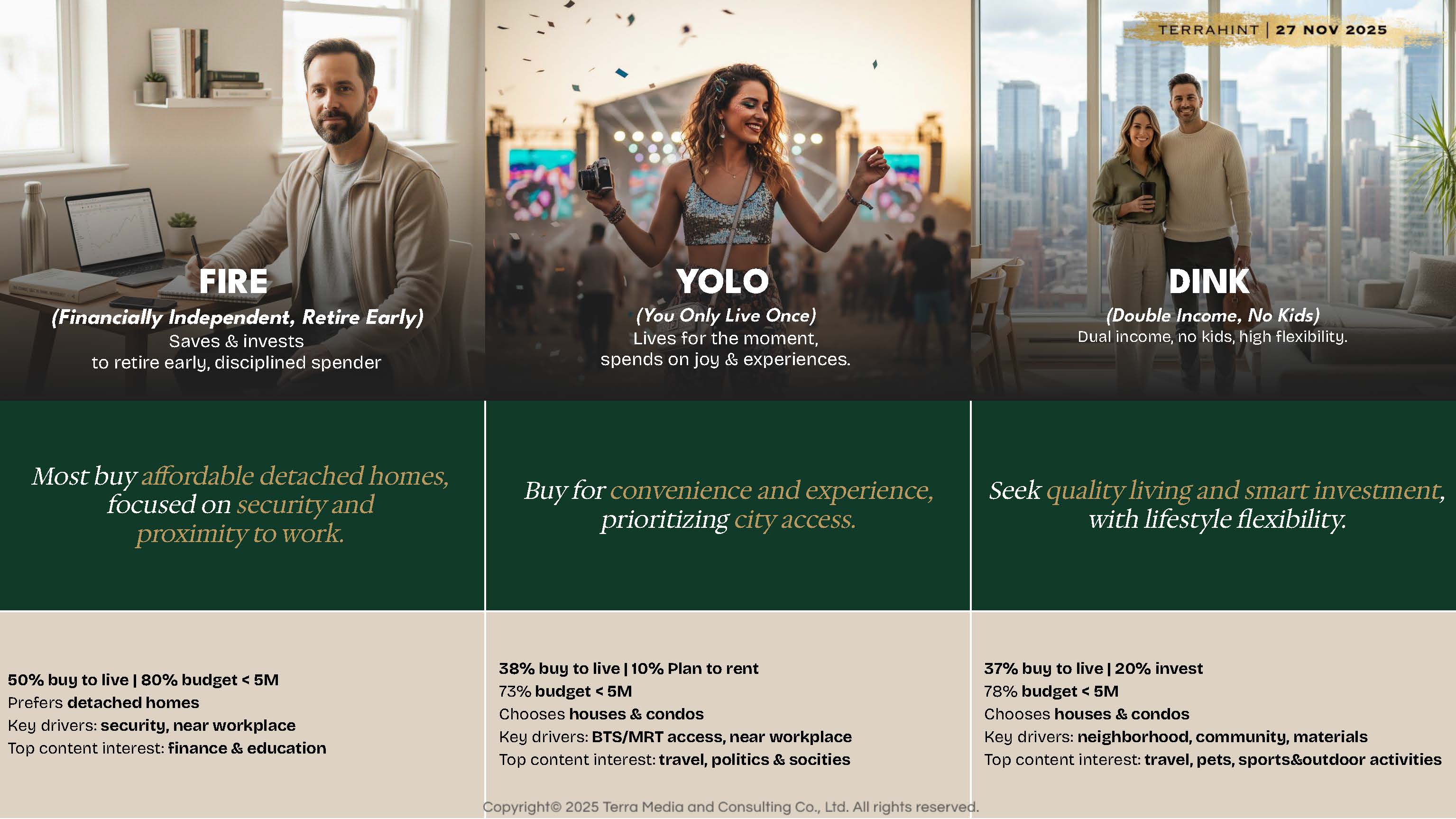

FIRE (Financially Independent, Retiring Early) Near retirement, no financial burdens, savings, interested in affordable single-family homes, and follow finance and education news.

YOLO (You Only Live Once) Enjoying life for oneself, focusing on convenience, interested in housing priced under 5 million baht (buy/rent), primarily concerned with personal matters, and following travel, politics, and society news.

DINK (Double Income, No Kids) Couples/LGBT with high income, no children, interested in good neighborhoods, and follow travel, sports, and outdoor activity news.

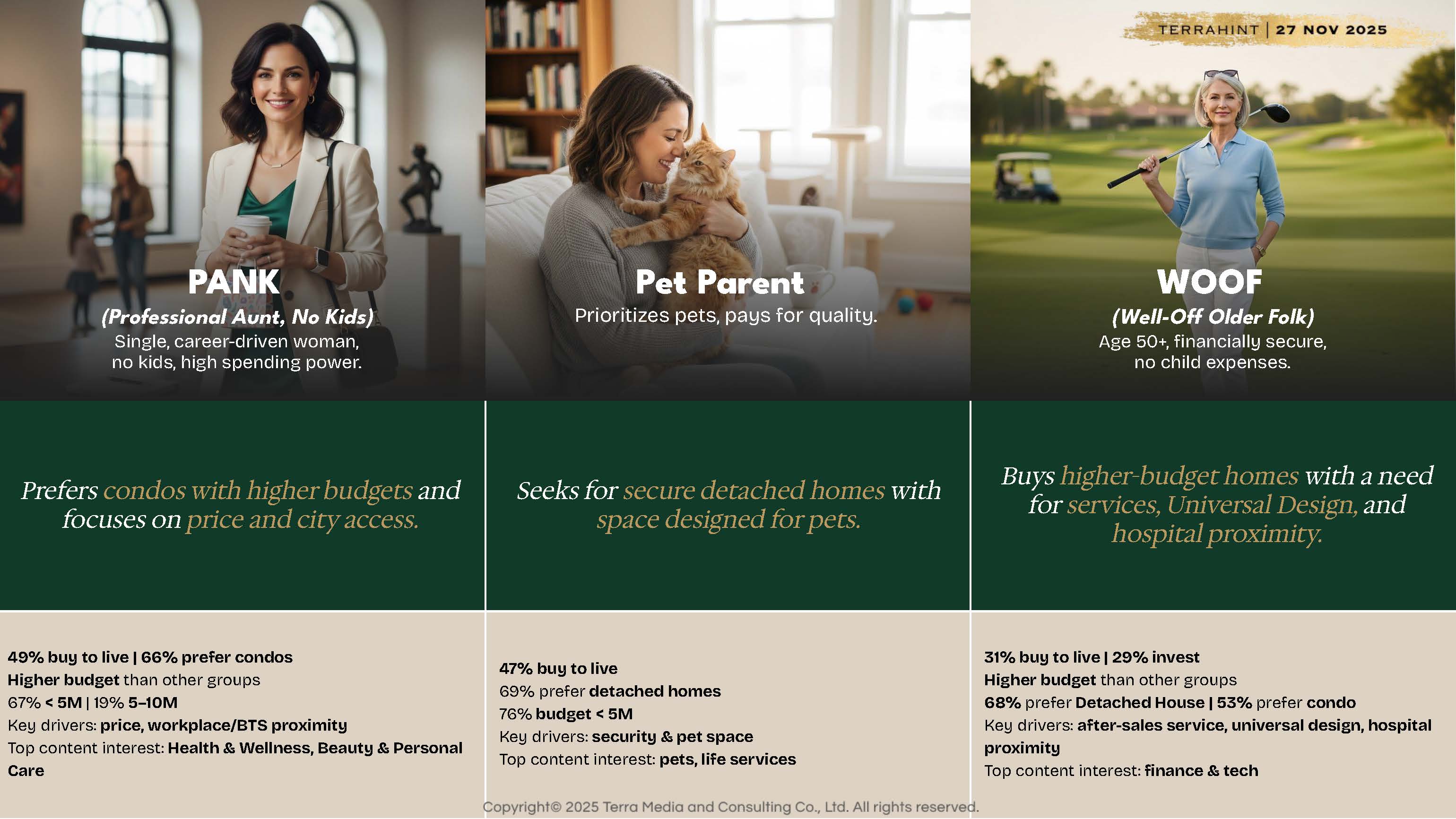

PANK (Professional Aunt, No Kids) Spending for themselves/nieces and nephews, high budget, unlimited spending behavior, focusing on image and spending, following health and wellness, beauty, and personal care news.

Pet Parent (Pet Owner, No Kids) Focusing on pets, needing space for pets, emphasizing private living, and following pet and life services news.

WOOF (Well-Off Older Folk) The wealthiest group, well-educated, living in an aging society, interested in universal design, proximity to hospitals, technology, and after-sales service, following finance and tech news.

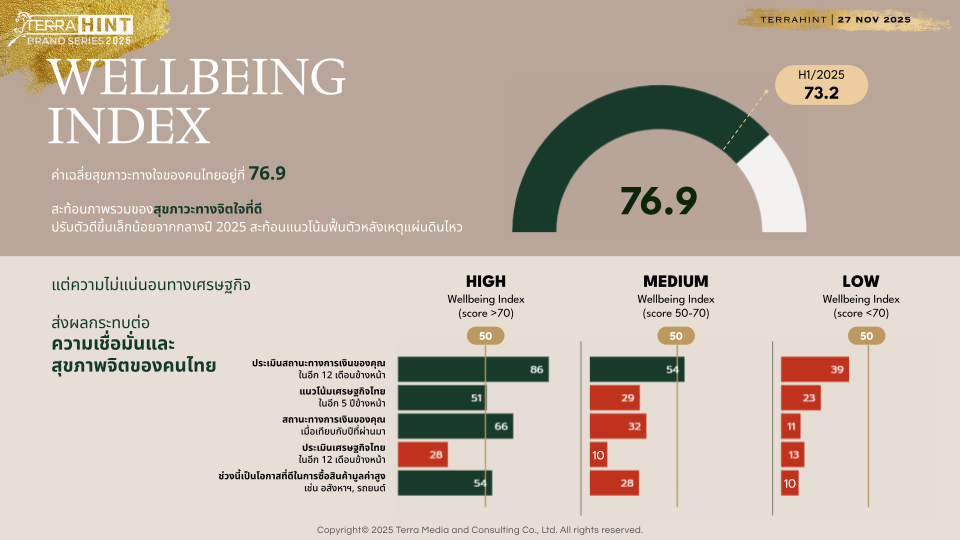

When Economic Confidence Aligns with Mental Well-being

Although the property purchase confidence index remains at a good level, it has slightly decreased compared to last year. However, considering the situation over the past six months, the index has improved, indicating hope for the upcoming year.

Interestingly, there is a disparity between views on "personal economy," where consumers feel optimistic, and their views on the Thai economy, which they still perceive as poor. This psychological contradiction reflects the reality that consumers are ready to spend but remain concerned about the overall national picture.

"We discovered that a good mental well-being index has a direct correlation with economic confidence. Those with a higher well-being index are more confident in spending than those with a lower index. Therefore, if we want our residents to buy our products, we must create well-being for them, making them feel secure and safe before they will dare to purchase our products or reach into their wallets."

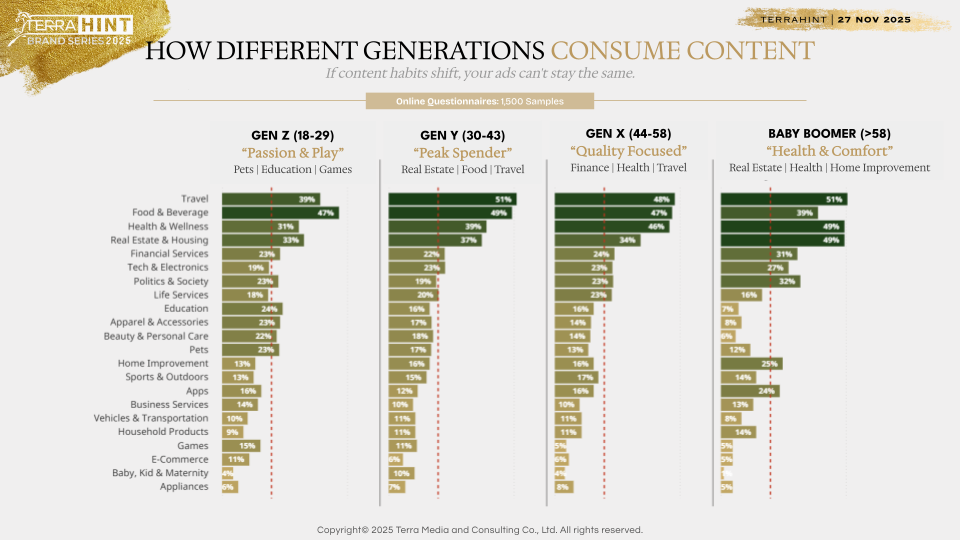

The Same Platform, but Different Content Consumption Behaviors

Furthermore, an analysis of Thai social media content consumption behaviors across four generations reveals that even on the same platform, the interests and content followed by each age group differ significantly. Baby Boomers and Gen X focus heavily on "health" as a major topic, with increasing concern for health as they age. Gen Y exhibits the highest content consumption behavior related to travel at 51%, followed by food and beverages at 49%, surpassing all other generations. Gen Z shows the highest interest in pet-related content at 23%, followed by education at 24% and gaming at 15%, with Gen Z ranking first in all three categories.

Wellness Vs Hospitality: The Greater Importance

The question posed to measure the importance between wellness and hospitality is: "Wellness" versus "Hospitality." It turns out that consumers place a higher importance on "Wellness" than "Hospitality." This includes:

- Quality of Life: Emergency and safety services.

- Large green spaces.

- Technology for convenience.

- And others in order.

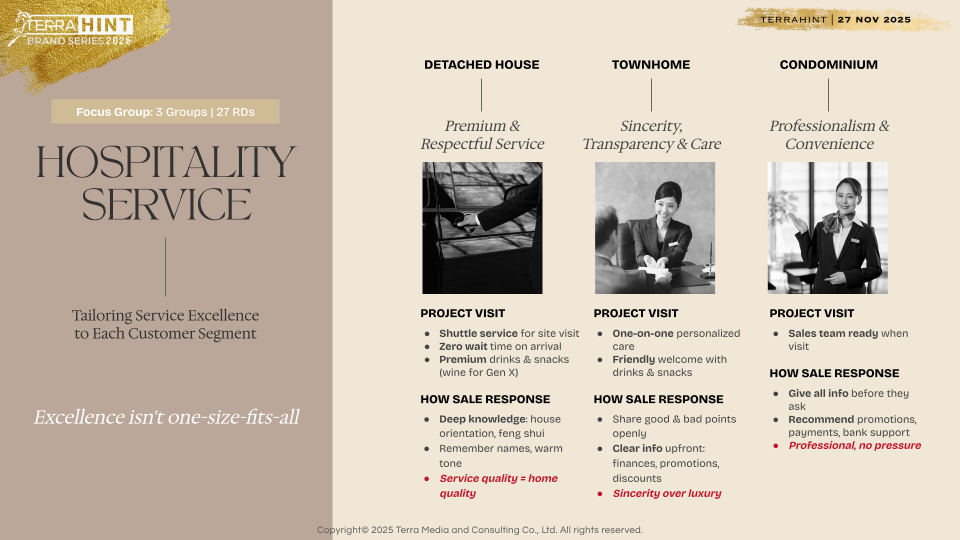

While consumers still desire hospitality services (such as room service, concierge, and property management) comparable to hotels, their expectations from developers have not yet met the set standards. This presents a gap or opportunity for operators to improve.

- Single-family homes: Require premium and respectful service, as customers believe that superior service should pay attention to every detail, from project viewing appointments with shuttle service to welcoming with carefully selected drinks and snacks, believing that "Service quality = home quality" reflects the quality of the home.

- Townhomes: Require sincere, transparent, and accessible service, not necessarily overly luxurious. “Sincerity and clear information” are desired, with salespeople expected to provide straightforward information about the project's strengths and weaknesses, believing that "Sincerity over luxury" is more valuable than luxury.

- Condominiums: Require speed and convenience suitable for a fast-paced lifestyle, emphasizing professionalism and comfort. They want a sales team ready to serve immediately when customers visit the project, providing complete information and recommending promotions - payment plans. Most importantly, they expect "Professional, no pressure" service, with professionalism and no pressure to book.

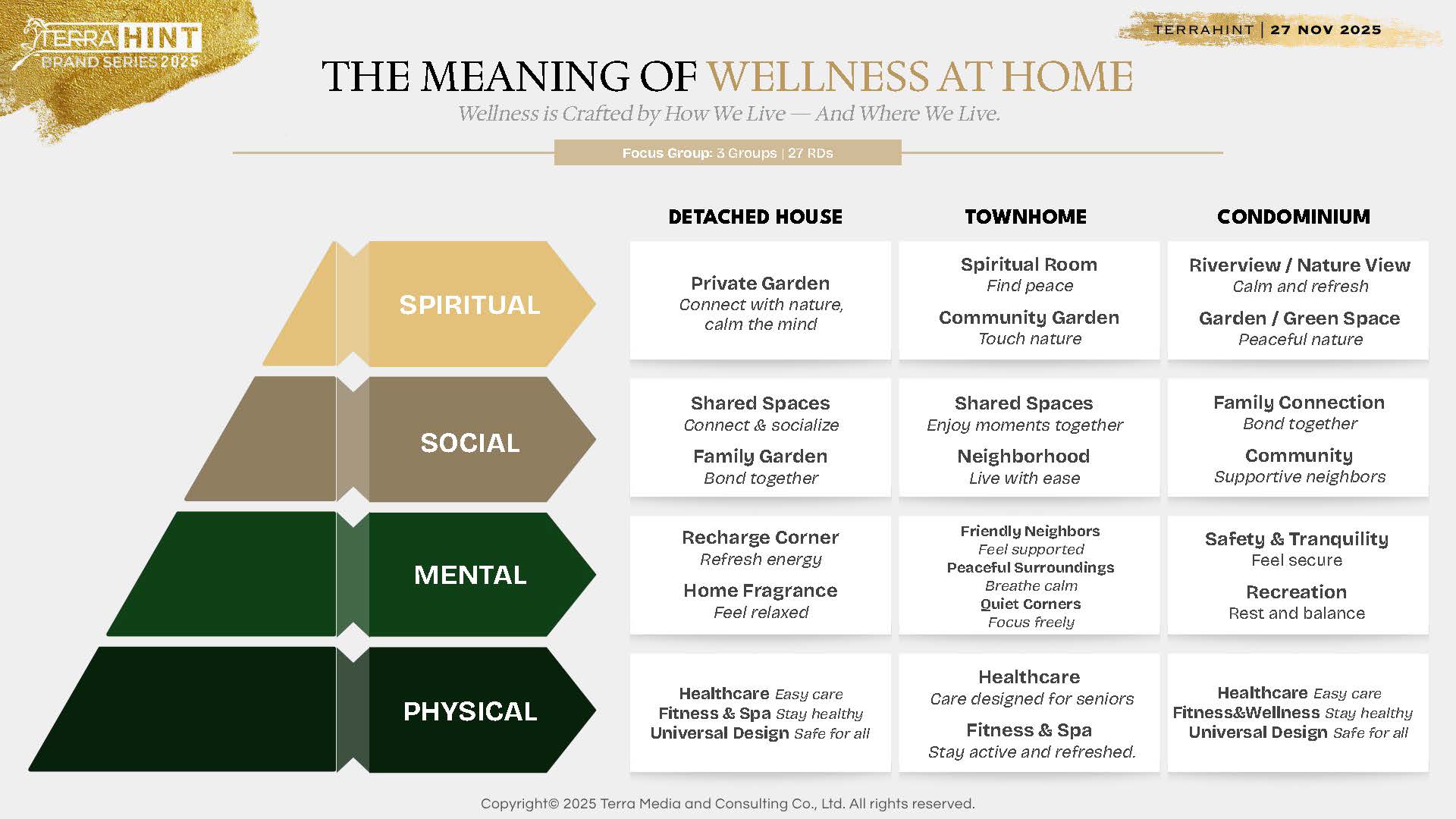

Concrete Needs for Wellness at Home

Consumers are not just looking for exercise spaces; they want "Meaningful Wellness at Home" that is tangible and connects with daily life, which can be categorized as follows:

Physical Wellness Dimension: Single-family homes require universal design, overall health; townhomes require fitness and spa; condominiums require universal design and health-tech.

Mental Wellness Dimension: Single-family homes require private corners for recharge/retreat; townhomes require friendly neighbor management; condominiums require family connection through private spaces or phone calls, or spaces to accommodate additional family members.

Spiritual Wellness Dimension: Single-family homes require private gardens with complete green spaces; townhomes require areas for small group activities/meditation; condominiums require rooms with good views/increased privacy or views that promote spiritual energy.

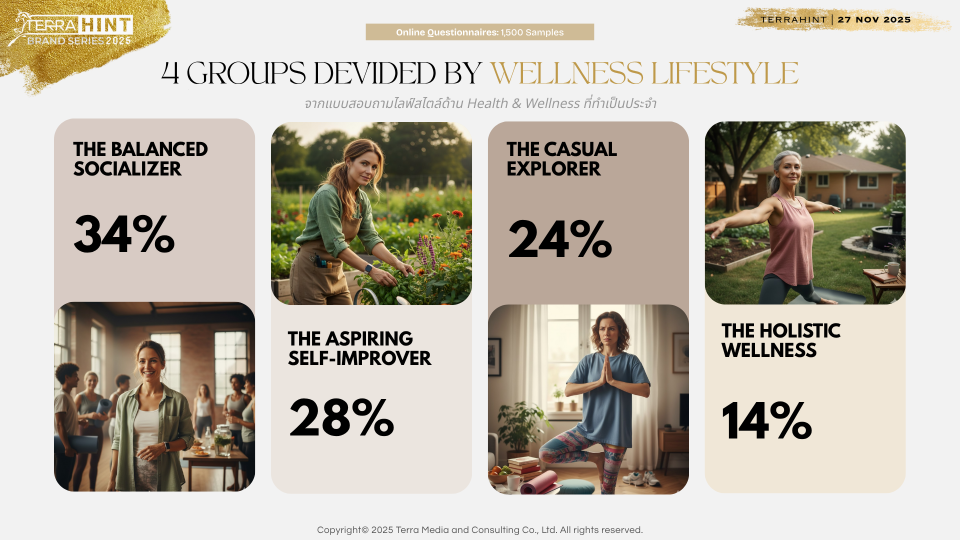

4 Wellness Personas Based on Lifestyle & Self-Care Approaches

From the study, consumer behaviors can be categorized into four groups based on self-care approaches and lifestyles, reflecting current needs and expectations for housing and services:

1. THE BALANCED SOCIALIZER (34%) A group of young people seeking balance between health and social life. While they take care of basic health, they do not neglect socializing and building relationships with others. They enjoy traveling both domestically and internationally, valuing experiences and meeting people. Their desired housing should offer convenience and time-saving technology, along with health and beauty services.

2. THE ASPIRING SELF-IMPROVER (34%) This group has their own health care approach, choosing only activities that genuinely interest them. They prioritize sleep and relaxation in nature but do not seek social activities. Housing for this group requires services beyond general offerings, such as room service or concierge services and safety-related services.

3. THE CASUAL EXPLORER (24%) A family group interested in health but facing obstacles in fully caring for themselves due to work and family responsibilities. They focus on easy activities like reading, listening to music, and meditating, necessitating basic services essential for living, especially regarding safety, such as transportation to hospitals.

4. THE HOLISTIC WELLNESS (14%) This group values comprehensive health care for body, mind, and society. They have discipline in sleeping, exercise regularly, and choose nutritious food. They enjoy being close to nature and value mental healing through outdoor activities. Their ideal housing must have large green spaces, comprehensive health care services, and standard safety systems.

The Wellness Blueprint: Strategies for Sustainability

Insights from the TERRAHINT BRAND SERIES 2025 seminar have provided a clear "blueprint" for entrepreneurs, marketers, and investors in the real estate industry, indicating that sustainable growth in this era does not stem solely from price competition or location but must place "Wellness" at the center of all processes, from product design and brand communication to after-sales service.

Step 1: Changing the Mindset from Selling Houses to Selling Quality Living The most crucial aspect is shifting developers' perspectives from "selling houses" to "selling quality of life." Modern consumers are knowledgeable about Wellness and have higher expectations. They are not just looking for a swimming pool or fitness center but require safety and emergency systems that respond quickly within four minutes, reflecting genuine concern for life, universal design to accommodate long-term living (Aging Society), and complete green spaces (Private Garden) that help rejuvenate the mind and create spiritual wellness.

Step 2: Adjusting Strategies According to Generation and Segmentation Including:

- Baby Boomers: Focus on holistic healthcare and well-being strategies, from physical health to mental and spiritual well-being.

- Generation X: Emphasize family-centered strategies, prioritizing care for both upper and lower family members (Sandwich Generation).

- Generation Y: Focus on individualized/personalized strategies, as this group has diverse personalities and seeks products that meet their specific needs.

Step 3: Enhancing Functional & Trust with After-Sales Service Although many large brands receive high trust scores, the overall score for the industry regarding "good after-sales service" still falls significantly below customer expectations. This is a point where differentiation can be created and true brand loyalty established. Investing in fast, sincere, and responsible after-sales service, akin to perfect hospitality service, will be key to transforming buyers into brand advocates ready to recommend our projects.

"Our challenge today is to align consumer expectations with what developers provide. In the context of Wellness, customers are not afraid to buy homes, but they are 'afraid of you,' fearing that what they see will not meet their expectations. What we need to do is instill confidence in every dimension of wellness and trust."

In summary, The Wellness Blueprint is not just a passing trend but a permanent foundation. Understanding the relationship between mental well-being and spending confidence is the most crucial strategy because when consumers feel safe, secure, and healthy, they will trust the brand and be ready to invest in a future designed for them.

#TerraBkk #TERRAHINT #BrandSeries2025 #TerraHintBrandSeries2025

#QualityLiving #TheWellnessBlueprint #Wellness #Hospitality