Understanding Sale with Right of Redemption and Related Concepts

Before delving into the details of sale with right of redemption, the author would like to clarify the differences among these four terms for a mutual understanding.

1. Selling Real Estate refers to the transfer of ownership (Title) of a property from the seller to the buyer. Selling residential properties, especially second-hand homes, can be quite challenging and time-consuming. Once ownership is transferred, the seller loses the right to reside in or benefit from that property. Additionally, property taxes and common area fees (if applicable) become the responsibility of the buyer or new owner. If the seller wishes to reclaim the property in the future, they must negotiate with the new owner, who may or may not agree to sell.

2. Consignment of Residential Property involves the property owner or seller entrusting another individual, typically a real estate broker, to find a buyer and assist in selling the property. This process is often referred to as a "listing," derived from the term Property Listing. Since selling a property can take a long time and buyers often want to see the actual property and review documentation, sellers frequently rely on brokers to handle these details. It is important to note that brokers do not hold ownership of the property being sold; they merely facilitate the connection between buyers and sellers. Brokers typically earn a commission, usually around 3% of the sale price. Thus, consignment is essentially selling real estate through a marketing intermediary.

3. Sale with Right of Redemption refers to the sale of a property where ownership has been transferred from the seller to the buyer, but the seller retains the right to repurchase the property within an agreed timeframe and price (as long as it complies with the law governing such sales, which allows for contracts of up to 10 years and interest rates not exceeding 15% per annum). The key difference between this and a typical sale is that the seller can request to buy back the property within the specified time and price. However, ownership has already changed hands, and if the seller fails to secure the funds to repurchase within the agreed timeframe, ownership is permanently transferred without the need for legal action. This aspect of sale with right of redemption can lead to significant losses for many individuals. Some readers may wonder why one would choose this option instead of a straightforward sale. The answer lies in the fact that traditional property sales can be difficult and time-consuming, while in a sale with right of redemption, the price is determined not by the seller but by the buyer or investor. Further practical details about this process will be explained later.

4. Mortgage is a loan secured by the property itself. Therefore, a mortgage is not a sale of the property, and ownership remains with the borrower. This allows the borrower to continue using the property and to pay property taxes and common area fees. If the borrower fails to repay the loan and interest, the lender cannot simply take the property; they must pursue legal action. Thus, a mortgage serves as collateral for a loan rather than a sale of the property.

The meanings of these four terms differ significantly, but they share one commonality: the property owner is in need of cash.

Sale with right of redemption is often encountered through credit companies, but currently, there are many investors (or buyers) engaging in this business. Typically, these investors work through real estate companies or agents to screen clients (or sellers) and assess the properties they are willing to buy.

Sale with right of redemption often offers more cash than a mortgage. Currently, it is common to see offers of up to 60-70% of the appraised value. However, it is important to note that there are three methods for appraising property value:

1. Cost Approach involves assessing property value based on the cost to acquire it, minus depreciation over time. This method often results in a lower appraisal value than the actual market value (this is also the method used by the government’s Treasury Department).

2. Market Approach considers supply and demand for the property and may involve comparisons with nearby properties. This method typically yields a higher appraisal value than the cost approach.

3. Income Approach is suitable for income-producing properties or commercial real estate, such as shopping centers, hotels, and rental office buildings.

It is true that sale with right of redemption can offer up to 60-70% of the appraised value, but this appraisal is often based on the cost approach or the Treasury Department's valuation. However, sellers must also consider additional costs, including: 1. Processing fees or "bag fees" of 5% of the loan amount; 2. Legal interest not exceeding 15% per annum, often with some interest deducted in advance to prevent early redemption; 3. Brokerage fees of 3%; 4. Transfer fees of 2% (even though the government has reduced transfer fees to 0.01%, this does not apply to sale with right of redemption as it is not a first-hand property). Additionally, sellers must pay personal income tax withholding and specific business tax of 3.3% if they have held the property for less than 5 years (or if their name has been on the property registration for less than 1 year). If the seller has held the property for more than 5 years, they will pay a stamp duty of 0.5% and minor documentation fees.

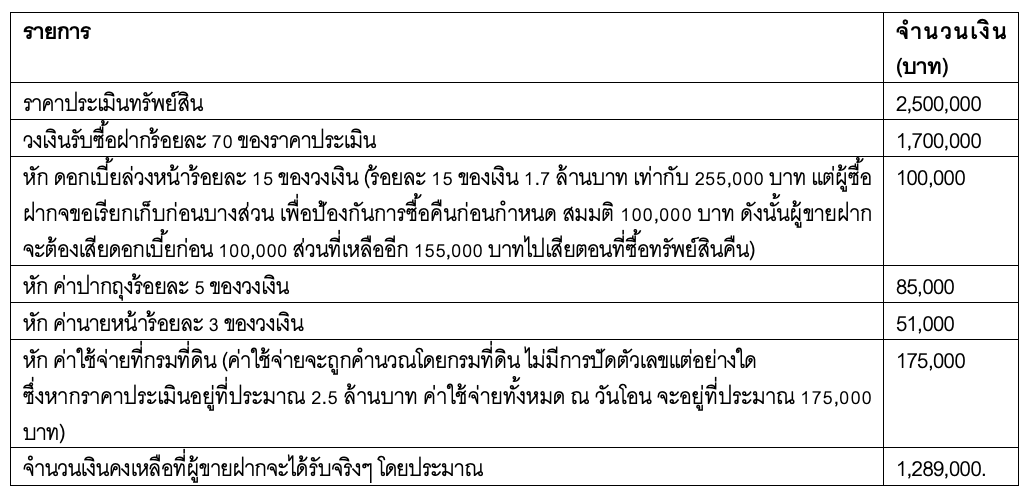

To illustrate, let’s assume a seller has a condominium of 73 square meters purchased for 4 million baht, but the Treasury Department appraises it at 34,500 baht per square meter. Thus, the appraised value would be approximately 2,500,000 baht (values are often rounded down). If the buyer offers 70% of this appraisal, the seller would receive about 1,700,000 baht. Typically, the initial sale contract lasts for 1 year, resulting in interest of 255,000 baht, plus the bag fee of 5% and brokerage fee of 3%. The seller would also incur transfer fees, withholding tax, and stamp duty (assuming they have held the property for over 5 years), totaling around 175,500 baht. This is summarized in the table below:

From the above table, the seller would net approximately 1,289,000 baht from this sale. Upon contract expiration (1 year), if the seller wishes to repurchase the property, they must pay the buyer 1,855,000 baht (1,700,000 + remaining interest of 155,000 baht).

This example illustrates a real sale with right of redemption. Therefore, when real estate companies or brokers claim to offer high loan amounts, it is accurate, but the appraisal method used is not specified. The 15% interest on the loan amount is in accordance with legal regulations, and the processing and brokerage fees are legitimate expenses that the company or broker is entitled to receive, just as the land office fees are expenses the seller must bear since they are the ones receiving income from the sale.

Readers may wonder why a condominium valued at over 4 million baht would only yield about 1.3 million baht in a sale with right of redemption.

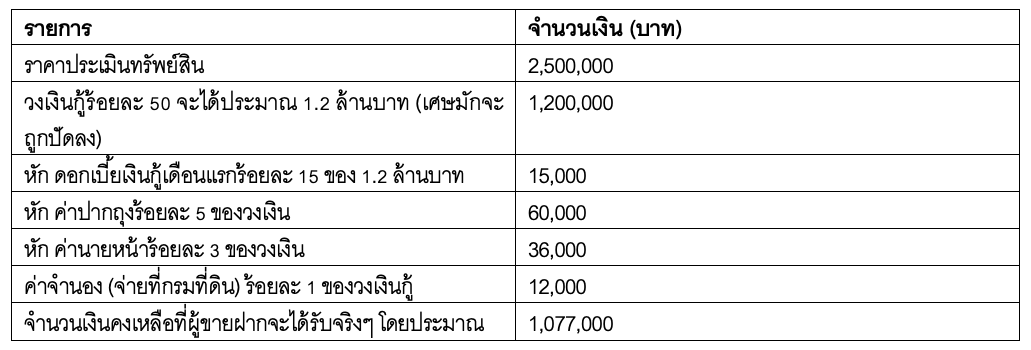

The author believes that many readers may question why, if the seller only receives about 1.3 million baht from the sale with right of redemption, they do not simply sell the condominium outright. The answer is that sometimes sellers need quick cash (or are in urgent need of funds) but do not want to sell the property immediately (as they retain the right to repurchase within the agreed timeframe). If they were to take out a loan using the condominium as collateral, they would typically receive only about 50% of the property’s value, which, after deducting various expenses, would leave them with just over a million baht. Moreover, the borrower would have to pay fixed monthly interest to the investor until the loan is repaid, as illustrated in the table below:

Thus, the borrower (not referred to as the seller anymore, as this is a loan) would receive approximately 1,077,000 baht. Additionally, the borrower would need to pay the investor 15,000 baht in monthly interest until the loan is repaid. If they wish to repay the loan, they must pay the investor a total of 1.2 million baht.

The author believes that many readers may also wonder if it would be better to borrow from a bank instead of an investor, as banks typically offer higher loan amounts, lower interest rates, and longer repayment terms. The answer is that borrowing from a bank takes longer for credit analysis, requires extensive documentation, such as proof of income, which demonstrates the borrower’s ability to repay the loan and affects loan conditions like interest rates, repayment terms, and monthly payments. Importantly, banks also check the borrower’s credit history or credit bureau information, including credit scores, which can lead to loan denial if the borrower’s score is below the bank’s threshold. However, as previously mentioned, sale with right of redemption or borrowing from investors does not involve credit history checks or credit scores. This is why borrowers or sellers can receive funds relatively quickly (sometimes within just 2-3 days).

Therefore, the author urges sellers or borrowers to be mindful that the funds obtained should be genuinely necessary and should only be taken as needed, such as to settle high-interest debts or personal loans from financial institutions with interest rates as high as 26% per annum. They must also ensure they can find the funds to repurchase the property. This is especially critical if the property being sold or mortgaged is the seller's or borrower's residence, as failing to secure funds for repurchase or redemption would inevitably lead to the loss of their home.

Readers may wonder if the Master of Science program in Real Estate Development Innovation at Thammasat University (MIRED) includes financial education. The author would like to inform that the MIRED program is interdisciplinary, integrating knowledge from various fields such as architecture, engineering, innovation management, and business administration. Consequently, the faculty members of the MIRED program come from diverse backgrounds, as the program employs instructors with qualifications and direct experience in each subject area.