How Risky Are Real Estate Investment Trust Bonds During COVID-19?

Another investment option for investors, besides holding units in real estate investment trusts (REITs), is investing in bonds issued by these trusts. These bonds provide investors with a fixed interest return and have a clear maturity date for principal repayment, offering returns of approximately 2 – 4% per year. This investment is considered to be less risky than holding REIT units, which yield dividends from profits generated by property rentals at around 5 – 7% per year.

However, the COVID-19 situation has impacted businesses, leading to negative cash flow and potentially insufficient liquidity for business operations due to the inability to generate income during lockdowns. Recovery has been limited due to decreased purchasing power following the economic slowdown, while businesses still face fixed expenses that cannot be immediately reduced, such as employee wages and utility bills. This has resulted in several companies defaulting on their bonds, such as Thai Airways International Public Company Limited (THAI) and Asia Capital Group Public Company Limited (ACAP). Readers may wonder about the risks associated with investing in bonds from real estate investment trusts, particularly regarding the likelihood of default on interest payments or principal repayment.

I would like to outline the key points to consider regarding the risks that investors may face in not receiving interest and principal payments on bonds:

- Credit Rating and Age of Bonds

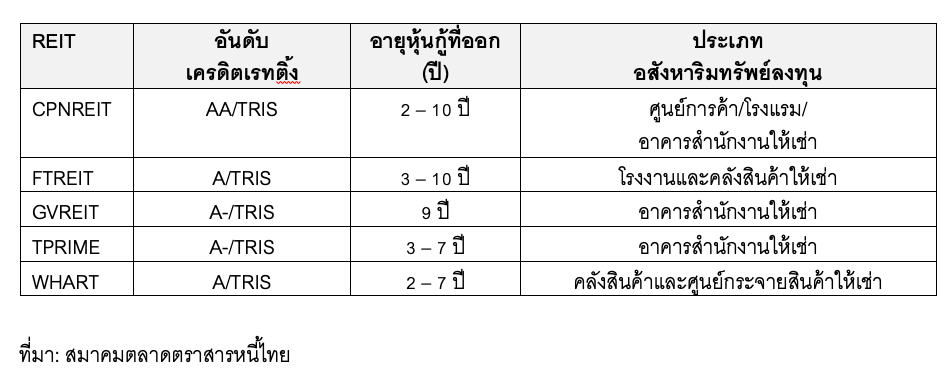

Although trusts can issue bonds without a credit rating, currently, all five trusts in the industry that have issued bonds have established credit ratings ranging from A- to AA. The fact that these ratings remain at the Investment Grade level (not below BBB-) indicates a low likelihood of default.

Another risk is that the trusts may be affected by COVID-19, leading to liquidity issues while having bonds due within the next 1 – 2 years. Although some trusts have bonds maturing soon, only a portion of the bonds will come due, reducing the risk that the trusts will be unable to raise funds for repayment.

Rating Information and Bonds of Real Estate Investment Trusts

- Income Shortfall Risks of Trust Investment Assets

The impact of COVID-19 on the investment properties of different trusts varies, leading to differing risks of income shortfalls and insufficient profits to cover interest and/or principal payments. For example, office buildings, factories, warehouses, and distribution centers have been less affected by COVID-19, resulting in a lower chance of income shortfalls and bond defaults. This includes shopping centers and retail spaces not located in tourist areas that rely on foreign tourists, which have shown good recovery. These trusts experienced reduced income only due to temporary tenant relief measures. However, trusts with hotel investments that have been significantly impacted may need to assess the extent of the impact on their investment portfolios and whether they will have funds to repay bondholders.

- Debt Repayment Obligations

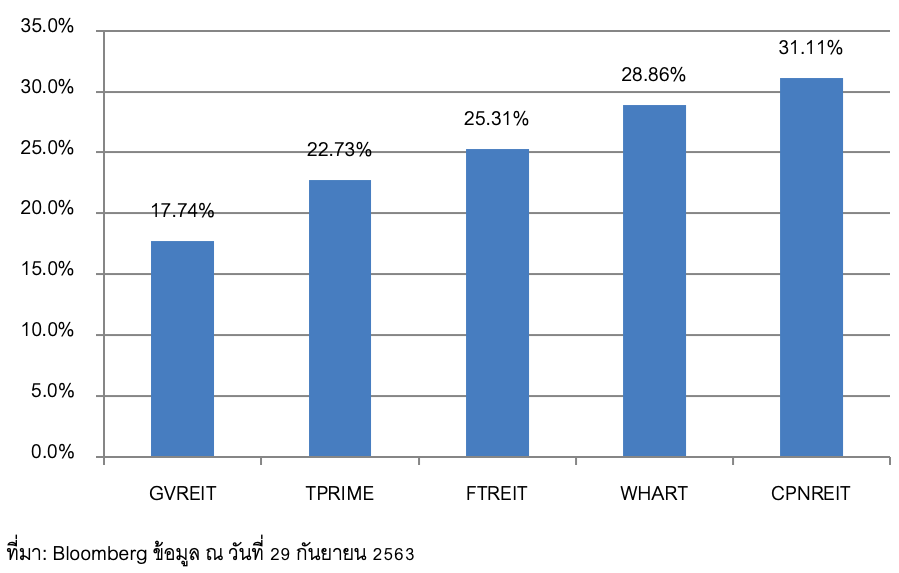

Each trust has varying levels of debt, leading to different default risks. Currently, all trusts that have issued bonds have established credit ratings to instill confidence in bond investors. These trusts have the potential to borrow up to 60% of the total asset value (TAV) according to regulations, given their Investment Grade ratings. However, these trusts have only borrowed 20 – 30% of their total asset value, meaning that even if they face liquidity issues, they still have room to borrow more, potentially seeking alternative financing sources to repay maturing bonds, such as commercial banks or other financial institutions.

Debt-to-Asset Ratios of Real Estate Investment Trusts Issuing Bonds

In summary, the bonds issued by real estate investment trusts currently present a relatively low risk of default given the current COVID-19 situation. As there are no new trusts planning to issue bonds, interested investors can purchase existing bonds from current bondholders through banks and securities companies.