When Secondary Cities Are Not Just an Option, But a New Destination for Living and Investment

In a world where consumer behavior is rapidly changing and major cities are facing congestion and rising living costs, the search for "new spaces" that offer both quality of life and better investment opportunities has become a crucial choice. "Secondary cities" are no longer just a visual respite; they have become destinations for both residents and real estate investors.

Secondary cities refer to those that are not the "main centers" of each region or do not appear on the list of top-tier tourist destinations such as Bangkok, Phuket, or Chiang Mai. Instead, they possess unique characteristics that are appealing, such as tranquility, good environments, low costs, and untapped business opportunities. Additionally, secondary cities are part of government promotion policies, such as the "Visit Thailand Secondary Cities" project or the "Half Price Tourism" initiative, which offer special privileges for accommodation and spending in these areas.

Trends of Thai Tourism in Secondary Cities

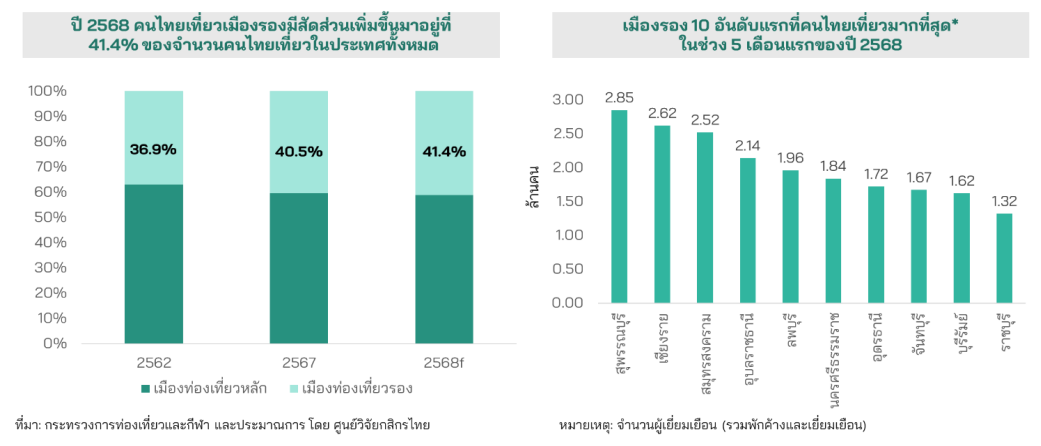

According to the Kasikorn Research Center, it is estimated that by 2025, Thai domestic travel will reach 205 million trips, an increase of 2.2% from the previous year. Although growth is slowing down, the proportion of tourism in secondary cities continues to rise. The share of Thai tourists visiting secondary cities in 2025 is expected to be 41.4%, up from just 32.3% before COVID-19. Many secondary provinces, such as Suphanburi, Chiang Rai, Samut Songkhram, and Ubon Ratchathani, attract over 2 million Thai tourists annually, surpassing some major provinces. The average spending per trip in secondary cities is 2,800 THB per person, compared to 5,000 THB per person in major cities, reflecting that the cost of living and living expenses in secondary cities remain low.

In the second half of 2025, domestic tourism among Thais is expected to continue growing, but at a slower rate of 1.4% compared to the previous year, supported by the "Half Price Tourism" project that helps reduce accommodation and shopping costs. However, the market still faces negative factors from a slowing economy, unpredictable weather, and increasing competition from abroad that attracts more Thai tourists.

Throughout 2025, the Kasikorn Research Center predicts that domestic travel among Thais will increase, but growth will not be uniform across all areas, with secondary tourist provinces receiving more interest from Thai travelers.

Factors driving the popularity of secondary cities include the desire to avoid congestion in major cities, the charm of a slow-life lifestyle, social media facilitating the discovery of new tourist spots, and the rise of remote work, leading more people to choose to live in secondary cities. The lower cost of living combined with a good quality of life is appealing. Additionally, more people are opting for "day trips" with over 51% of domestic tourists being non-overnight visitors, prompting movement in the service and real estate sectors.

Secondary Cities and Real Estate Investment Opportunities

In recent years, the Thai real estate market has undergone significant changes. Previously focused primarily on major cities like Bangkok, Chiang Mai, or Phuket, the "secondary cities" are now emerging as new areas with high growth and investment potential, especially as people seek better quality of life, affordable living costs, and improved connectivity. These cities often have lower land prices and construction costs than major cities, resulting in lower investment costs while still offering high growth potential if supported by transportation, economic, or service sector developments. Factors supporting the real estate market in secondary cities include:

1. Expanding infrastructure: The Thai government has ongoing plans to develop infrastructure in secondary cities, including high-speed rail (e.g., Bangkok-Nong Khai), expressways, regional airports, and public transport connections, making travel from Bangkok or major cities to secondary cities more convenient and faster. For instance, the dual-track railway from Khon Kaen to Nong Khai enhances connectivity between major provinces in the Northeast, promoting population movement and investment in surrounding secondary cities.

2. Changing consumer behavior: The trend of hybrid and remote work has led many young people to choose to live in cities with a good quality of life, natural surroundings, and low costs while still being well-connected to the outside world. Secondary cities have become an ideal solution. A survey by DDproperty in 2024 found that 28% of potential homebuyers plan to move outside major cities, particularly in provinces like Lampang, Phitsanulok, and Surat Thani.

3. Lower investment costs: Land costs in secondary cities are significantly lower than in major cities. For example, land in some areas of Nakhon Si Thammarat is priced around 15,000–30,000 THB per square wah, compared to Bangkok, where prices may start at 100,000 THB per square wah or more. Investing in mid-range housing or condominium projects in secondary cities thus offers quicker returns on investment.

Real Estate Market in Secondary Cities and Tangible Opportunities

1. Mid-range to lower-end condominiums: Although condominiums are not yet a primary market in some provinces, the demand for housing that is not tied to land ownership is on the rise, especially among workers and students. For example, in Khon Kaen, which has a large university and medical center, many new condominiums are emerging within a 2–3 km radius of the city center.

2. Single-family homes and townhouses: In many secondary cities, single-family homes and townhouses remain the primary market, especially for buyers looking to expand their families in their hometowns. Investors can develop medium-sized projects of 30–50 units at affordable prices, achieving net profits of 20-25% if costs are managed well.

3. Rental income for steady returns: In provinces that are government centers, tourist attractions, or have industrial estates, such as Rayong, Lamphun, or Nakhon Ratchasima, the long-term rental market continues to have steady demand. Investing in houses or condos for rent can yield average returns of 5–7% per year, which is higher than bank deposits or some mutual funds.

Secondary cities are no longer just "second choices." Real estate in these areas is transitioning from an "option" to a "mainstream" choice for those seeking a good quality of life, low costs, and future growth potential, both for living and investment. For homebuyers, secondary cities offer "life value," while for investors, they represent "cost-effective investments" and "opportunities that have yet to be seized."

Source: Kasikorn Research Center