Project 'You Fight, We Help': Temporary Measures to Assist Debtors of Commercial Banks

Project 'You Fight, We Help' is initiated by the Bank of Thailand (BOT) in collaboration with the Ministry of Finance, the National Economic and Social Development Council, the Thai Bankers' Association, the International Banking Association, the Association of State Financial Institutions, and certain non-financial business operators. This project introduces temporary measures to assist individual debtors and specific groups of SMEs.

Under the 'You Fight, We Help' project, the assistance will cover debtors of commercial banks, specialized financial institutions, and non-bank businesses that are part of the commercial banking group. It has been observed that debtors continue to show interest in participating in the project, leading to an extension of the registration period until September 30, 2025 (Phase 2), from the original end date of June 30, 2025 (second extension).

To register for the project, click https://services.bot.or.th/cpm?id=smp_landing_page

* Please note that the measures from each service provider have different conditions. Be sure to review the details, qualifications, and conditions before registering for the project.

Source: BOT https://www.bot.or.th/th/news-and-media/activities/khunsoo.html

Measures for Debtors of Commercial Banks, Specialized Financial Institutions (SFIs), and Non-Bank Companies in the Commercial Banking Group

Measure 1: "Direct Payment, Keep Assets"

For those with home loans, car loans, motorcycle loans, and small business debts with relatively low limits, this measure allows them to retain their collateral assets by restructuring their debts to reduce installment payments and interest burdens. The installment payments made will be applied entirely to the principal, allowing for quicker debt closure, while the interest will be deferred for 3 years. If participants meet the conditions, the deferred interest will be completely waived.

Assistance Format

(1) Reduced Installments for 3 Years where debtors pay a minimum of 50% and 90% of the original installment in the first, second, and third years respectively (in a stepped manner), with all installments applied to the principal.

(2) Interest Suspension for 3 Years where the deferred interest will be waived entirely if the debtor complies with the conditions throughout the 3-year period and does not incur new debts in the first 12 months after joining.

Debtors can pay more than the minimum installment to reduce the principal further and close the debt faster.

Qualifications for Debtors to Participate in the Measures

(1) Total credit limits with financial institutions must not exceed the specified amounts, considering separate limits per contract (per financial institution) by loan type as follows:

- Home loans / Home for cash: Total limit not exceeding 5 million baht

- Hire purchase / Car registration loans: Total limit not exceeding 800,000 baht

- Hire purchase / Motorcycle registration loans: Total limit not exceeding 50,000 baht

- SME business loans: Total limit not exceeding 5 million baht

- For personal loans and credit card debts, if there are home or car debts that meet the above conditions, debt consolidation measures can be considered under the risk levels acceptable to the financial institution, with total limits not exceeding the specified amounts.

(2) The loan must have been contracted before January 1, 2024.

(3) The debtor's status as of October 31, 2024, must be one of the following:

(3.1) Overdue for more than 30 days from the due date, or

(3.2) Not overdue or overdue for no more than 30 days (from the due date) but has a history of overdue payments* and has restructured debt since January 1, 2023.

* For debtors with a history of overdue payments of no more than 30 days, the overdue period is considered from January 1, 2023.

Conditions for Participation in the Measures

(1) Debtors will not be able to enter into new consumer loan contracts in the first 12 months after joining the measures, except for SME business loans necessary for liquidity. Creditors may provide additional loans based on the debtor's repayment ability.

(2) Participation in the measures will be reported in the NCB.

(3) If the debtor cannot pay the minimum installment as specified or fails to comply with other conditions, such as incurring new debts before the 12-month period, they will be removed from the measures and must repay the deferred interest.

(4) If the loan contract has a guarantor, the guarantor must consent and sign a new guarantee contract.

Example Calculation: Home Loan - Car Loan

Measure 2: “Pay, Close, Finish”

For those with bad debts and low outstanding amounts, they will receive a relaxed debt restructuring to enable quicker repayment and account closure, allowing for a fresh start.

Assistance Format

Debtors can make partial payments to facilitate quicker debt closure.

Qualifications for Debtors to Participate in the Measures

(1) Individual debtors of all types with a debt status as of October 31, 2024, overdue for more than 90 days (NPL).

(2) Debt obligations as follows:

- All types of loans with a debt burden not exceeding 5,000 baht per account.

- Unsecured loans with a debt burden not exceeding 10,000 baht per account.

- Secured loans* with a debt burden not exceeding 30,000 baht per account and credit limits per account as follows:

> Home / Home for cash / Individual SMEs: Limit not exceeding 5 million baht.

> Hire purchase / Car registration loans: Limit not exceeding 800,000 baht.

> Hire purchase / Motorcycle registration loans: Limit not exceeding 50,000 baht.

* Which have already enforced the collateral and cannot be pursued.

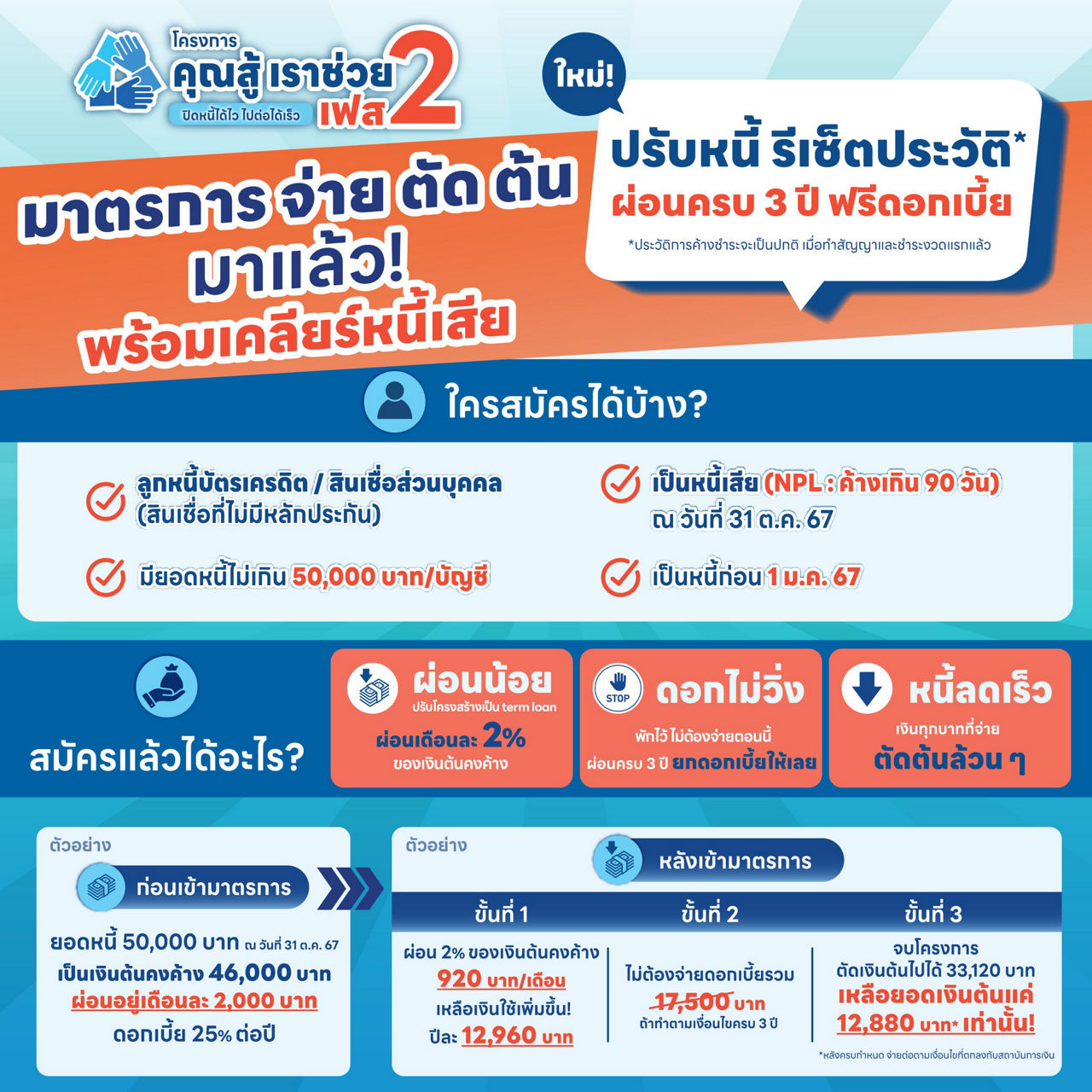

Measure 3: “Pay, Cut, Principal”

Individual or corporate debtors with bad debts from unsecured loans (e.g., credit cards, cash cards) will receive debt restructuring with relaxed repayment terms (term loan), where interest will be suspended for 3 years, and if participants meet the conditions, the deferred interest will be entirely waived.

Assistance Format

- Debt restructuring into term loan repayment.

- Repayment of 2% of the outstanding principal before joining the measures.

- All payments will be applied to the principal, and interest will be suspended for 3 years, with all deferred interest waived if the debtor meets the conditions.

- Debtors can agree with creditors to pay more than the specified installment to reduce the principal further and close the debt faster.

Qualifications for Debtors to Participate in the Measures

- Individual or corporate debtors with a status of bad debt (NPL) as of October 31, 2024.

- Unsecured loans (e.g., credit cards, personal loans) with outstanding debts not exceeding 50,000 baht per account.

- Loan contracts made before January 1, 2024.

Conditions for Participation in the Measures

(1) Debtors will not be able to enter into new consumer loan contracts in the first 12 months after joining the measures. If necessary to borrow for business liquidity, creditors may provide additional loans based on the debtor's repayment ability.

(2) Participation in the measures will be reported in the NCB.

(3) If the debtor cannot pay as specified or fails to comply with other conditions, such as incurring new debts before the 12-month period, they will be removed from the measures and must repay the deferred interest.

Participating Financial Institutions and Non-Banks Find the list and contact numbers of creditors/business operators participating in the project here.

Check if your debt is included in the measures?

Registration Steps

Source: Bank of Thailand BOT