Summary of TERRA HINT PROPERTY HACK 2024: Exploring Real Estate Strategies in a Divided Global Economy

This event aims to unite and strengthen relationships among real estate entrepreneurs and enhance understanding beneficial to members of the real estate business as well as related industries. It serves as a tool for managing real estate businesses in line with current conditions.

The Thai Real Estate Association, the Nonthaburi Real Estate Trade Association, and Terra Media and Consulting Co., Ltd. have organized a seminar titled "Property Hack: Exploring Real Estate Strategies in a Divided Global Economy." The event was honored by the presence of Pranrit Chuanchaisit, President of the Thai Real Estate Association, and Precha Kulpaisal, President of the Nonthaburi Real Estate Trade Association, who opened the event.

The seminar featured two main topics: "Breaking Through the Real Estate Deadlock in a Heated Economy" and "Opportunities in Real Estate to Support New Purchasing Power," gathering experts from various fields to provide insights aimed at sustainably driving the real estate industry amidst unpredictable economic conditions.

What are the key takeaways? TerraBkk has compiled the highlights for you here!

Discussion on "Breaking Through the Real Estate Deadlock in a Heated Economy" by four speakers:

Over the past decade, Thailand's economy has experienced growth rates below potential due to various external factors, averaging around 3% compared to 5% in ASEAN countries, excluding Singapore. Key sectors driving the economy include exports, tourism, logistics, and consumption. However, the desired financial inflow is from the manufacturing and service sectors, which are still recovering, along with real estate.

In terms of economic stimulation, addressing both short-term and long-term economic issues remains essential. This includes attracting foreign investment, public and private sector investments, and restructuring tax policies. Long-term solutions involve structural adjustments.

Focusing specifically on the Thai real estate sector, it has seen growth but not significantly high. Supply continues to increase, yet purchasing power remains stable. The government has made efforts to support this sector, recognizing its importance in driving Thailand's economy. Studies show that the real estate sector contributes approximately 13% to GDP, which is quite substantial.

“From the government's perspective, investment in infrastructure such as electric trains and motorways is crucial to stimulate private sector investment and enhance future purchasing power. For instance, in Bangkok, over 10 electric train lines have been constructed, boosting purchasing power and attracting foreign investment, leading to expansion.”

However, it must be acknowledged that Thailand's household debt is currently high, around 90% of GDP, primarily from housing, vehicle purchases, and household business debts. Ideally, household debt should not exceed 80% of GDP. This excessive debt poses a barrier to real estate growth as consumers struggle to secure housing loans.

The Ministry of Finance has introduced various low-interest loan measures (Soft Loans) to support the real estate sector, targeting middle to lower-income groups to help create purchasing power at the grassroots level. Additionally, other monetary policies are in place, but developers are concerned about high housing loan interest rates, which the Bank of Thailand is expected to maintain.

“The government is also trying to address debt issues, both formal and informal, particularly among vulnerable groups, categorizing them into small borrowers and SMEs. The central bank will implement various measures through state financial institutions to help delay debt payments and restructure household debts to mitigate the impact of debt issues. Ultimately, the most important aspect is structural adjustment and financial literacy, as debt problems require finding a balance between resolving formal debt issues and ensuring people remain aware of their debt burdens to foster financial discipline and create opportunities for household financial recovery.”

Moreover, there are tax incentive measures such as subsidies for electric vehicle usage in the real estate sector, reductions in land and property tax, and reductions in registration fees for property transfers and mortgages this year for residential properties priced below 3 million baht, providing greater access to financing for middle, lower-income, and vulnerable groups.

Dr. Piyasak shares a view of the Thai economy aligning with Dr. Phisit, highlighting a continuous but slow global economic recovery. In the U.S., unemployment rates are rising while inflation is decreasing, leading to predictions of possible interest rate cuts mid-year, a trend also seen in Europe. In contrast, China faces negative real estate issues and unemployment challenges.

For Thailand, it is believed that once the 2024 budget is implemented, public investment, which had previously slowed, will return to normal, with GDP expected to grow by 3%.

In the real estate sector, the Work From Home trend has increased demand for residential properties, while demand for office space has decreased. This trend mirrors developments in the U.S. and Europe, where office real estate is contracting.

Dr. Piyasak also pointed out that a major issue for Thailand is being stuck in the 'middle-income trap.' Currently, Thailand's GDP per capita is $7,500, having remained stagnant for over three years. In contrast, China, which was at $3,000 twelve years ago, is now at $12,000 per capita, also facing the middle-income trap.

The question is why? Dr. Piyasak analyzes three key points:

One point is monetary policy. Over the past 12 years, Thailand has operated under a monetary principle of printing money at about 81%, the lowest in Asia, compared to Vietnam at around 300% and Indonesia at about 250%. This is because Thailand has low inflation, which means a lower money supply.

This situation partly arises from the Bank of Thailand's excessive caution, fearing the creation of a bubble. As Thailand prints less money than other countries, the result is a stronger currency. Over the past decade, the Thai baht has appreciated by about 19% against all currencies.

The consequence of a stronger currency is reduced competitiveness in exports compared to rival countries, limiting competitive power to only a few large players. When the broader business environment does not grow, operators cannot raise employee salaries, leading to lower consumption. Meanwhile, essential goods must increase in price but cannot, as consumers lack purchasing power, resulting in a continuous cycle of cost management.

The second point is the Ministry of Finance's infrastructure investment measures, which have not grown sufficiently. Over the past 12 years, large infrastructure investments in Thailand have grown by about 18%, while in South Korea, it is 50%, and in the Philippines, 112%.

The third point is the aging society. Currently, the age structure of Thai society shows that those in their 40s constitute the largest proportion in Asia. This means that market and labor growth will be low, providing little incentive for foreign investment. One solution is to liberalize in various ways, such as opening up labor in different forms.

Meanwhile, real estate operators are concerned about housing interest rates affecting consumer purchasing decisions. Uthen Lohachitpitak, CEO of Pruksa Holding Public Company Limited, believes that this concern should not be overstated, as he is confident that interest rates will eventually decrease. However, he emphasizes that the more critical issue is the policy of injecting funds to stimulate foreign investment (Fund Flow). Even if interest rates do not drop, if investment is stimulated, the economy will generate jobs and continuous cash flow.

Additionally, he suggests that real estate developers should consider whether the decline in property purchases is due to weak purchasing power or because the products do not match the purchasing power. For example, Pruksa employs Design Thinking to deeply understand housing needs, studying family living conditions. When making purchasing decisions based on available funds, if a developer does not produce suitable homes within a budget of 1.5 million baht, consumers may only be able to afford a condo.

“We focus on developing housing first. Our goal is to make housing feasible within the purchasing power available, utilizing state policies to support this. We have introduced a concept of homes priced at 1.29 million baht, resembling a townhouse but not exactly a townhouse, offering a two-story home with 75-80 square meters, smart home features, personal parking, and a shared garden called 'Garden of Happiness.'”

The same executive also shared Pruksa's development strategy, emphasizing partnership work to reduce construction costs and exchange knowledge, leveraging Pruksa's 30 years of construction expertise as a driving force.

“We partner with other operators because we believe that in a situation where you need to reduce construction costs, we can help lower costs as we are in the same industry. We understand the obstacles in home construction, which has been Pruksa's strength for over 30 years and can assist other players.”

“Today, operators must manage the risks of project development, handling construction and home delivery. If homes are delivered quickly, your cash flow will increase.”

Secondly, risk management involves not expanding projects too large and too quickly, focusing on sustainable strategies from selling homes to living, extending to building strong communities.

“If real estate wants to grow rapidly, it must grow through partnerships. Pruksa has established a fund to invest in Proptech or Sustainability and Outside In, looking at living from an innovative perspective.”

“Today, everyone talks about living well and healthily, discussing healthy living styles. The question is, is the concept of development just about house design? Pruksa believes it is not. What needs to be done is to change almost all construction materials, focusing on reducing carbon footprints for environmental sustainability and simultaneously reducing costs, not just carbon stories but pushing costs onto consumers.”

Overall, the housing market data from Terra Byte, collected from Bangkok and surrounding areas, shows that condominiums priced below 2 million baht have improved in areas with clear demand, such as near universities and industrial estates, as these areas have continuous demand, making them suitable for both personal living and rental investment.

Meanwhile, the upper segment condominiums are slowly moving, but interestingly, in the segment above 7 million baht, new projects have emerged, recovering from the COVID-19 situation, with some projects or locations seeing improved sales.

In the townhome segment, which was significantly affected during the COVID-19 situation, especially in the segment below 3 million baht, there are now signs of improvement in the 3-5 million baht segment.

For single-detached houses, the market remains strong across almost all segments, particularly in the luxury segment, which has seen high launches.

When considering real estate companies in the market, among the top 10 largest companies, most focus on horizontal markets, with only Sena, ASSETWISE, and NOBLE having a higher proportion of condominium projects than horizontal markets. Most single-detached houses are located in the Ratchaphruek, Nakhon In, Samut Prakan, and Lat Krabang areas.

“During COVID, Lat Krabang was quite stagnant due to the aviation industry not being popular, but now that the aviation sector is returning, Lat Krabang is regaining popularity, along with areas like Phetkasem and Phutthamonthon, which have seen new roads similar to highways, leading to improved sales in those areas.”

“Regarding condominiums, after the expansion of electric trains, such as the Blue Line, Yellow Line, and Pink Line, condominium locations are no longer limited to the city but have expanded along these train lines, with prices being three times cheaper than in the city.”

Additionally, real estate developers are increasingly expanding projects to provinces, with both local and cross-regional developers. The Work From Home trend allows people to return to live in provinces. Some companies, especially multinational ones, have found that they can work remotely, with popular provinces including Phuket, Ubon Ratchathani, Chonburi, Nakhon Ratchasima, and Chiang Mai.

4:00 PM - 6:00 PM Discussion on "Opportunities in Real Estate to Support New Purchasing Power" by four speakers:

Reflecting back to the COVID-19 period, Phuket was one of the provinces most affected by COVID but was also one of the first to unlock due to the Phuket Sandbox policy. Since then, Phuket has gradually recovered, with a clear recovery starting in mid-2023, coinciding with a significant leap in the real estate sector driven by Russian demand fleeing the Ukraine war to live on Phuket Island.

The Vice President of the Phuket Real Estate Association analyzed that this phenomenon occurred due to a perfect timing coincidence. During the COVID-19 period, the Phuket real estate market was stagnant, and the limited existing inventory became insufficient when foreign demand surged unexpectedly, leading to a booming Phuket real estate market.

But is the Phuket real estate market genuinely interesting? The answer is yes, as there is continuous real demand, leading to a circulating investment trend, coupled with the rapid recovery of tourism in Phuket, creating a significant leap in real estate demand from Thai workers in the area, tourists, and foreigners residing in Phuket long-term. The largest foreign buyers in Phuket include Chinese, Russian, and French nationals.

According to real estate data, in 2023, there were over 8,800 residential property transfers in Phuket, representing a 20% growth compared to 2022, with horizontal properties growing by about 23% and vertical properties by about 38%, which is a high rate.

“Developing condominium projects in Phuket is not straightforward due to environmental laws, requiring multiple steps for project approval, taking about 6-8 months. Therefore, after COVID-19, as the market began to improve, it takes about a year to design and start construction, meaning that the Phuket real estate sector truly began to restart in 2023, while single-detached houses can be built more quickly as they require less approval.”

Thus, in 2023, there will be a significant increase in construction permit applications compared to land allocation permits, reflecting that the Phuket real estate market is focusing on the luxury segment in high-priced land locations, such as Laguna, Layan, Rawai, and Sai Yuan. The reason for the lack of land allocation is that the demand in Phuket primarily comes from foreigners, and land allocation is mainly for sales purposes.

“Currently, real estate developers in Phuket include both local and external operators, with good sales in both high-rise condominiums and villas. However, recently, the volume of villas may have decreased due to rising land and construction costs, coupled with a weakening Thai baht against a strengthening Chinese yuan, affecting construction material costs, most of which are imported from China, leading to a 20-25% increase in material costs.”

“Additionally, the real income of people in Phuket relies on newcomers from other regions working in the area, growing alongside the tourism and service sectors. This new group typically earns between 30,000-40,000 baht, making lower-tier housing the highest transfer segment at 35-40%. Furthermore, financial institutions are regaining confidence in Phuket real estate and are starting to adjust their plans to be more aggressive, making Phuket real estate quite promising across all segments. For investors looking to invest in Phuket real estate, now is the best time to do so within the next two years, as demand is at its peak.”

Marketing experts shared their thoughts on real estate marketing strategies during this period of certainty, stating that SC Asset aims to diversify its portfolio. Currently, SC Asset not only develops both high-rise and horizontal residential properties but also office buildings, with some collaborating with IWG to modernize spaces into Flexible WorkSpaces suitable for the new generation of workers. Additionally, they have three hotel businesses, including YANH Hotel in Ratchawithi and a hotel soon to open in Sukhumvit 29 and Pattaya, as well as rental properties in downtown Boston, USA, and warehouses.

In the residential business, SC Asset will balance its portfolio by focusing on properties priced below 10 million baht, as this segment is gaining popularity. Currently, SC Asset's portfolio consists of 70% horizontal properties and 30% high-rise, with 70% being luxury properties priced above 10 million baht and 30% below 10 million baht.

“We believe that the upper market still has potential, but it is not as hot as before. However, this year, the segment below 10 million baht has improved. Upon reviewing the portfolio, SC Asset has projects over 10 million baht that cover almost all locations. Ultimately, this may lead to market share competition, making the decision to balance the portfolio below 10 million baht a better choice. Nevertheless, we will not stop developing luxury products.”

Additionally, Nattakitti shared marketing tips for this era, emphasizing the importance of adhering to the DNA and strengths of each developer.

“I believe that all developers look at the same data set, but it depends on which segment they are most comfortable with. Every developer has their own DNA. For SC Asset, we continuously create homes that align with new lifestyles based on studying customer behaviors to match each area and style.”

For example, single-person homes have received positive feedback for improving living quality by changing the design approach from dividing rooms into many to fewer rooms but with more space, adding relaxation corners, walk-in closets, and shoe rooms. Such features are typically found in luxury homes, but this concept has been adapted for affordable single-person homes, leading to the development of homes that cater to both introverts and extroverts.

“Single-person homes target those without children, which could be couples earning together, whether male-female, male-male, or female-female. Thus, they can also be developed to cater to the LGBTQ community.”

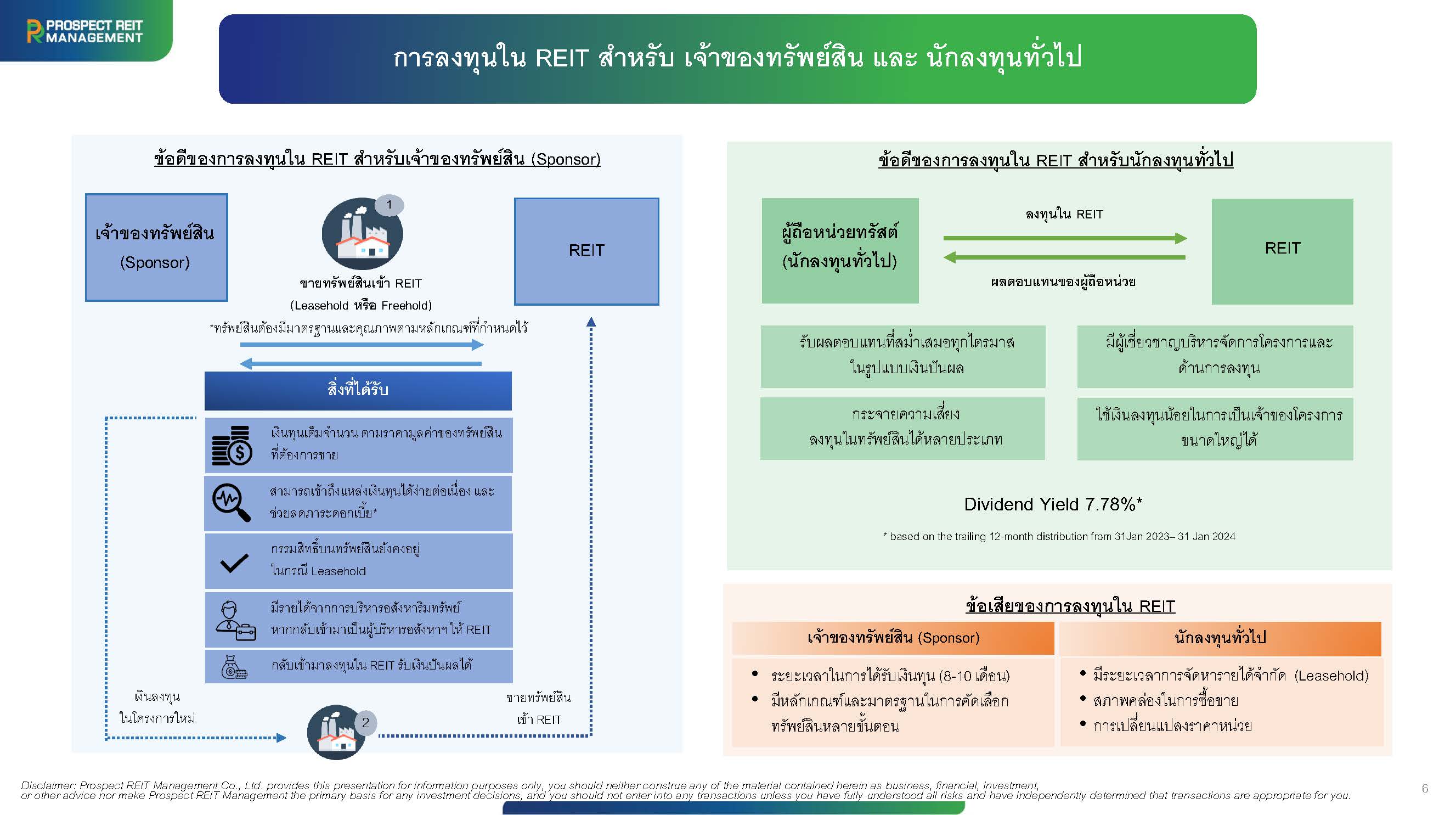

In addition to creating value in marketing, there are also interesting investment opportunities in real estate through other forms, such as investing in REITs (Real Estate Investment Trusts). Oranong Chaitong explained that investing in REITs is a type of investment in rental properties, where the asset must generate clear and consistent income, be legal and ethical, and be registered on the stock exchange (SET), allowing for buying and selling like stocks.

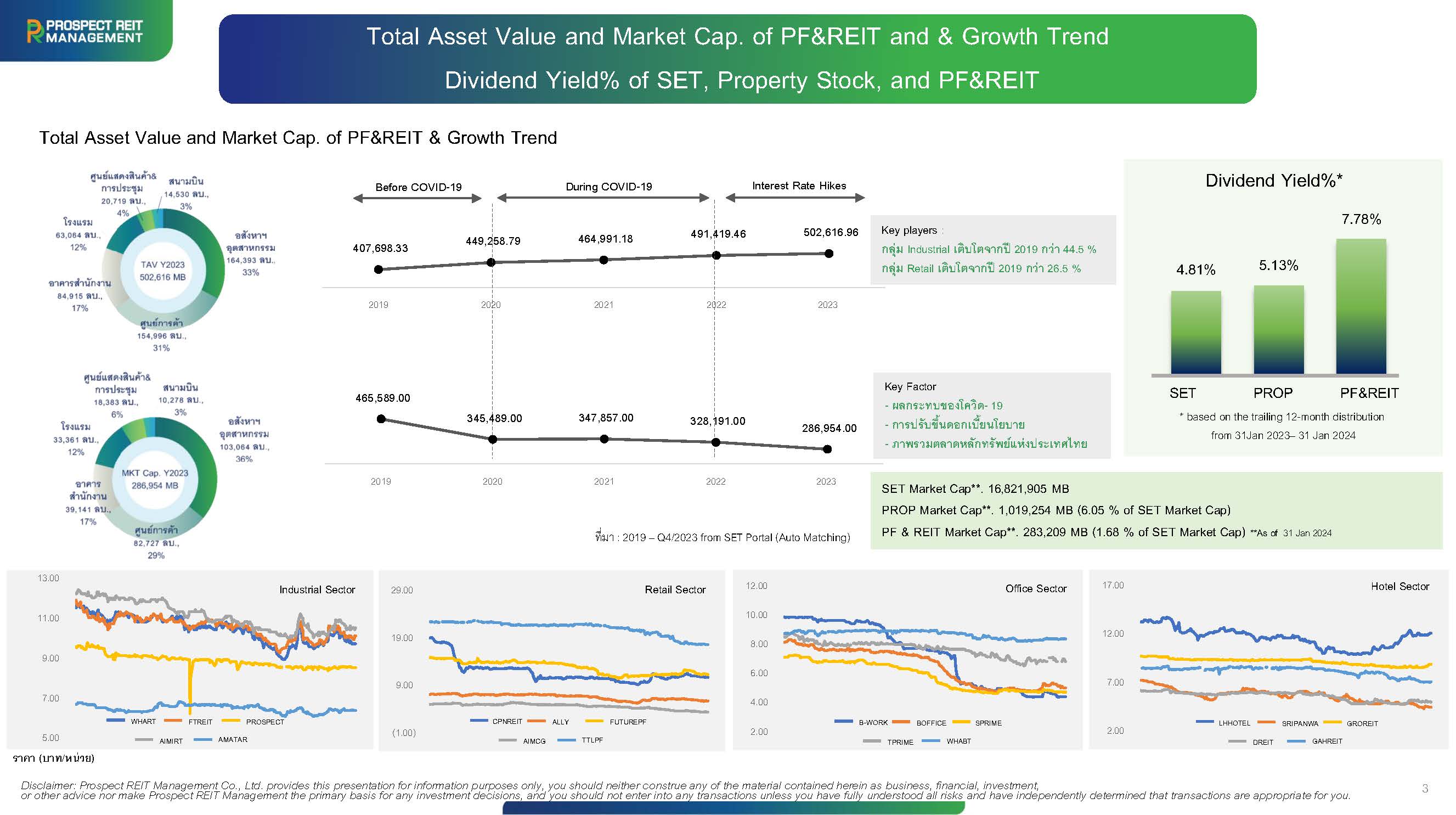

Currently, there are 27 REITs, with six popular sectors, the largest being industrial real estate, including factories and warehouses, accounting for about 40%, followed by shopping centers, office buildings, hotels, exhibition and conference centers, and airports.

Overall, the REIT situation can be divided into two dimensions: the total asset value and market pricing, as these assets are listed on the stock exchange. Before COVID-19 and during the trade war, REITs had a total asset value of over 400 billion baht, which is quite high. Despite the impacts of COVID-19 and interest rate situations, asset prices have consistently grown, explaining why REITs have received positive responses from investors.

The second dimension concerns market pricing, where external factors have caused market values to decline, currently around 200 billion baht. However, Oranong views this phenomenon as an opportunity since each REIT has adjusted lower, providing a chance for investors to buy in for potential future returns, with dividend yields reaching 4.8% in the SET and 7.7% in PF&REIT.

“Each type of bond has a chance of return, depending on how much risk the investor can accept and how well they understand each sector. Nevertheless, REITs provide consistent quarterly dividends, with 90% of REITs currently in the market offering dividends that can be recorded back.”

When discussing the real estate business, the office building sector is also facing fierce competition due to changing consumer behaviors, prompting building owners to adapt. “Providing flexible office rental spaces” has become crucial in catering to the needs of modern office users.

Thitiwat Thanapornnithinan, Country Manager of IWG, a leading provider of flexible workspace solutions, reflected on the changing landscape of office buildings in Thailand, noting that these changes can be viewed from both supply and demand perspectives.

From the supply side, before COVID-19, the office building market was thriving, with occupancy rates nearing 90%. However, post-COVID, companies and organizations have increasingly adopted hybrid working models, and new office buildings are being designed to better meet the needs of modern work life. In the past year, the emergence of Grade A office buildings has increased by 30%.

On the demand side, after COVID-19, companies and organizations have reduced their office space and increased WFH, leading to decreased office rental budgets to cut costs. At the same time, new demand has emerged from recognizing Thailand's potential as a headquarters location, similar to Singapore.

“Thailand has the potential to be a mini Singapore, with advantages in tax support for expatriates, an environment that promotes a good quality of life for employees, an educated population capable of using English, and relatively low labor costs. This situation has attracted demand from large foreign companies considering relocating their headquarters.”

Due to these changes, the market has become highly competitive, leading to a price war where office rental prices have dropped by 25%, and occupancy rates have fallen to 70%. Building owners are becoming more flexible, willing to offer special conditions to attract tenants, diversifying risks in various ways, including shorter lease agreements compared to the past, which typically lasted three years, and partnering with co-working spaces to expand their tenant base.

This presents a new opportunity for office businesses like IWG to meet the needs of office building operators and respond to the behaviors of modern companies with ready-to-use office solutions and flexible workspace options.

“This service model can cater to various scales, from 2-3 square meters to 2,000-3,000 square meters. Even virtual offices, which do not have a physical space but serve as a registered address for companies, can be provided with check-in locations worldwide. Many businesses require such services, such as lawyers who work off-site and do not need a physical office but need a place to drop off documents.”

Furthermore, Thitiwat predicts future demand will rise from IT and tech platforms, which are expected to grow significantly, necessitating more office spaces. Thailand will become a favorable hub not only due to its location advantages, lower living costs, and lower cost of living compared to Malaysia and Singapore but also because it is a destination where foreigners want to reside.