Thai Baht Opens at 33.86 Baht per Dollar, Unchanged from Last Week's Close

Mr. Poon Panichpipool, a market strategist at Krungthai GLOBAL MARKETS, Krung Thai Bank, revealed that last Friday night, the Thai Baht weakened near the 34 Baht per dollar mark due to the strengthening of the dollar after better-than-expected U.S. non-farm payrolls data. However, the dollar faced profit-taking and pulled back, resulting in a gradual strengthening of the Baht.

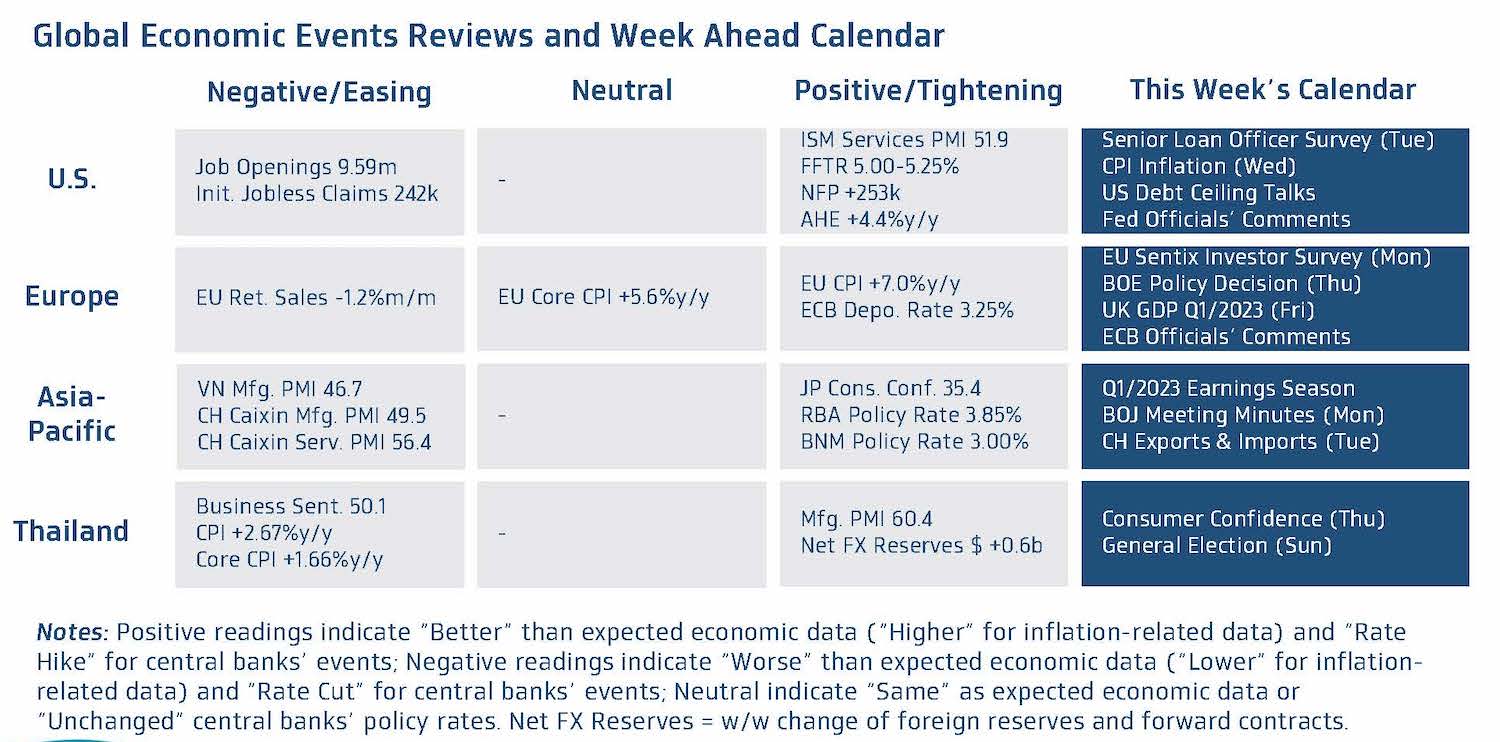

Last week, the Fed signaled a readiness to pause interest rate hikes, while the European Central Bank (ECB) reiterated its stance to continue raising rates to tackle high inflation. This week, we see key highlights including the U.S. CPI inflation rate and discussions on raising the debt ceiling, while in Thailand, the market will be awaiting the results of the upcoming general election. Notable economic data reports include:

Global Economic Outlook

▪ U.S. – A key highlight that market players will closely monitor is the CPI inflation rate for April. The market anticipates that the momentum of both CPI and Core CPI inflation may not show a clear slowdown as expected (CPI +0.4% m/m, Core CPI +0.3% m/m), keeping inflation rates around 5.00% and 5.50%, respectively. This scenario may increase the likelihood of the Fed continuing to raise interest rates. However, we believe the Fed may choose to maintain high policy rates (Higher for Longer) as economic trends and inflation rates are expected to be impacted and slow down due to tighter credit conditions. Market players will also be watching the Senior Loan Officer Survey from the Fed, which is expected to indicate a clearer tightening of credit conditions due to the Fed's ongoing rate hikes and liquidity issues in the U.S. banking system. Most banks may tighten lending standards, while demand for loans may decrease. Additionally, market players will be awaiting statements from Fed officials to assess the Fed's monetary policy outlook after the latest U.S. labor market data showed strength and exceeded expectations. Another interesting point that may impact the financial market atmosphere is the political risk in the U.S. regarding the debt ceiling, with market players closely watching negotiations to raise the U.S. government's debt ceiling. Historical data since 2000 shows that during periods of debt ceiling concerns, market players tend to hold Japanese Yen (JPY) and gold as safe-haven assets, while the dollar often weakens due to concerns that the U.S. may risk defaulting on its debt, affecting confidence in the dollar as a Reserve Currency.

▪ Europe – We assess that the high inflation rate in the UK, which shows no clear signs of slowing down (April CPI inflation may be around 10%, while Core CPI may be at 6%), will be a significant factor for the Bank of England (BOE) to proceed with a +0.25% rate hike to 4.50%. Furthermore, we believe the BOE may continue to signal readiness to raise rates until inflation is successfully controlled, closely monitoring economic trends and inflation (Data Dependent). In terms of economic data reports, the market expects the UK economy to grow only +0.2% y/y in the first quarter of this year, partly due to strikes in March. Additionally, market players will be watching statements from ECB officials to evaluate the ECB's monetary policy outlook.

▪ Asia – The market expects China's exports in April to grow around +10% y/y, which may not reflect increased demand for goods due to last year's low export base amid lockdowns in major cities like Shanghai. However, imports may contract -0.3% y/y, indicating that domestic demand for goods may not be recovering well. In Japan, the market will be monitoring the latest BOJ meeting minutes, as the BOJ continues to maintain an accommodative monetary policy despite inflation being significantly above the 2% target.

▪ Thailand – We assess that the improving recovery trend in the economy, supported by the tourism sector, may help boost the consumer confidence index in April to 54.8 points. However, high living costs, such as electricity bills, could pressure consumer confidence. Additionally, market players will be awaiting the results of the general election on May 14, which may impact the atmosphere in the Thai financial market in the short term.

Regarding the outlook for the Thai Baht, we expect it to fluctuate sideways after breaking above the support zone of 34.00 Baht per dollar. Factors pressuring the Baht to weaken may come from dividend payment flows to foreign investors (estimated at around 190-200 million dollars this week), while foreign investor fund flows may remain unclear until the general election results are known. Technically, the 50-day EMA (around 34.20-34.30 Baht per dollar) will be a crucial resistance zone if the Baht weakens past the 34.00 Baht per dollar mark.

As for the dollar, we believe it has a chance to rebound if U.S. inflation comes in higher than expected or does not show a clear slowdown, leading market players to believe that the Fed may maintain interest rates for an extended period. However, the dollar may weaken further, especially if the market is concerned about the debt ceiling issue or if the BOE reiterates its readiness to raise rates, causing the British Pound (GBP) to strengthen.

We maintain the recommendation that during this period of high volatility in the financial market due to both U.S. political factors (debt ceiling issue) and Thai politics, operators should use various hedging tools, such as options, to enhance efficiency in managing exchange rate risk.

We see the Thai Baht's range this week at 33.50-34.25 Baht/dollar, while today's range is expected to be 33.75-34.00 Baht/dollar.