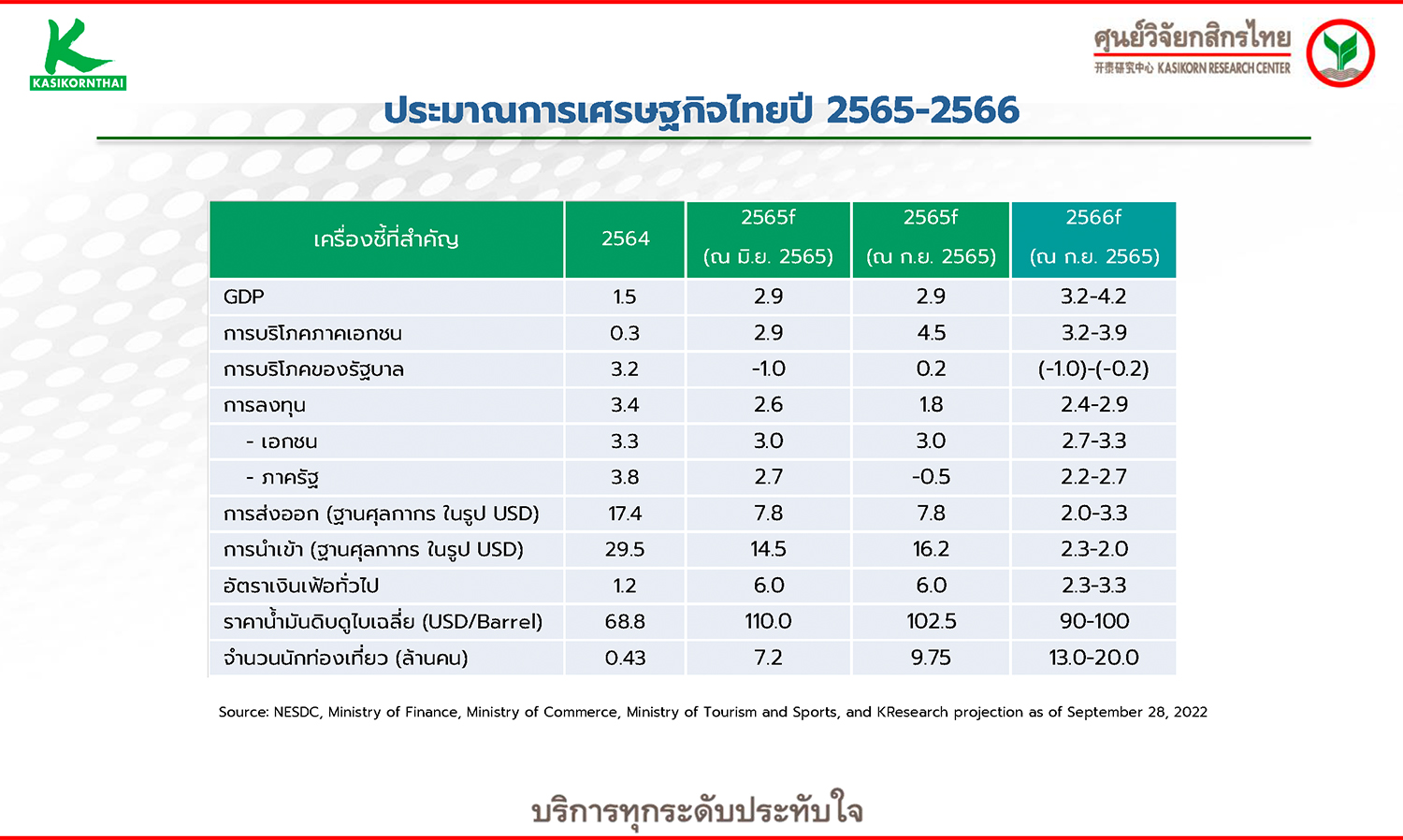

Kasikorn Research Center Maintains 2022 GDP at 2.9%, Projects 2023 GDP Growth of 3.2-4.2% Driven by Tourism Amidst Economic Slowdown of Trading Partners

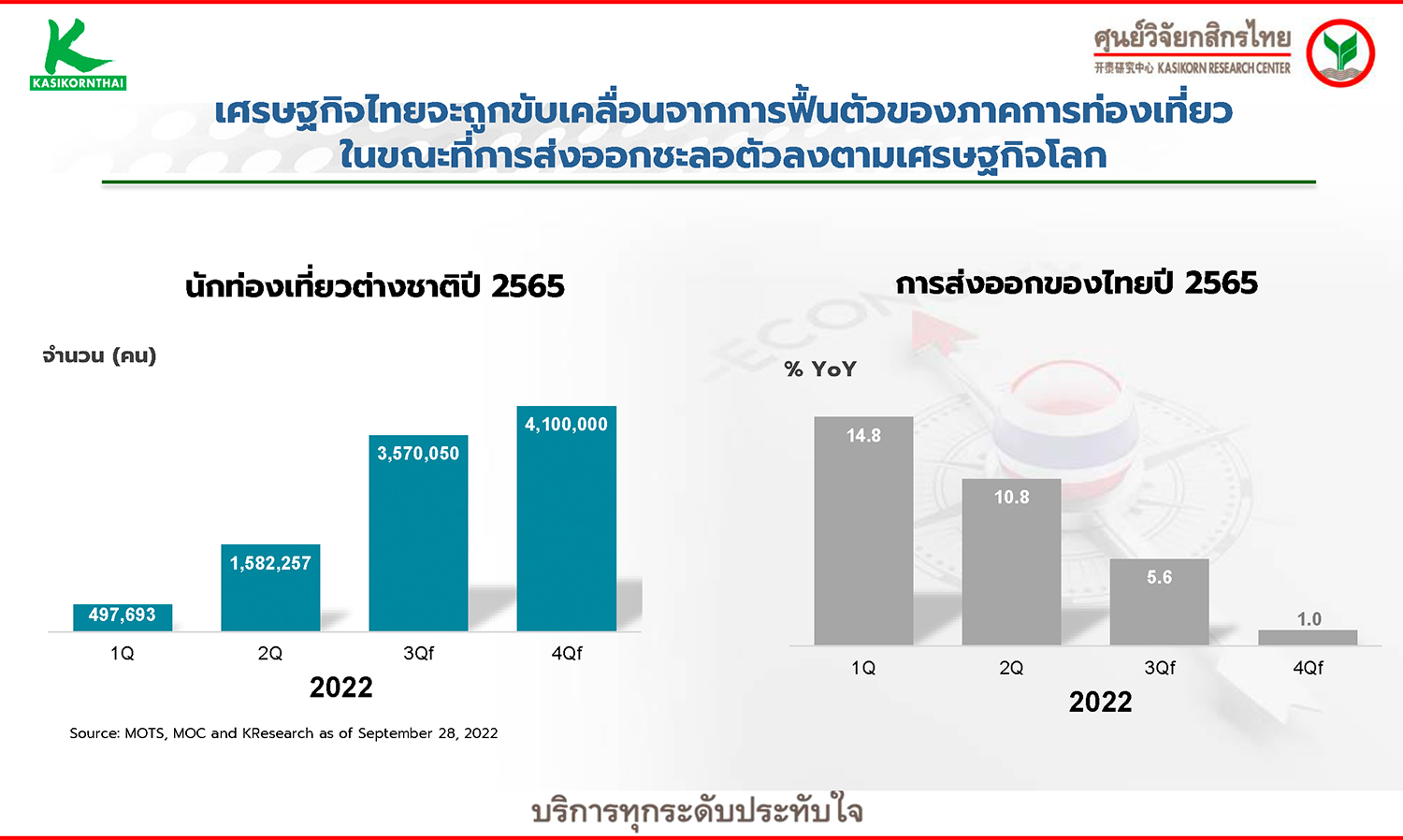

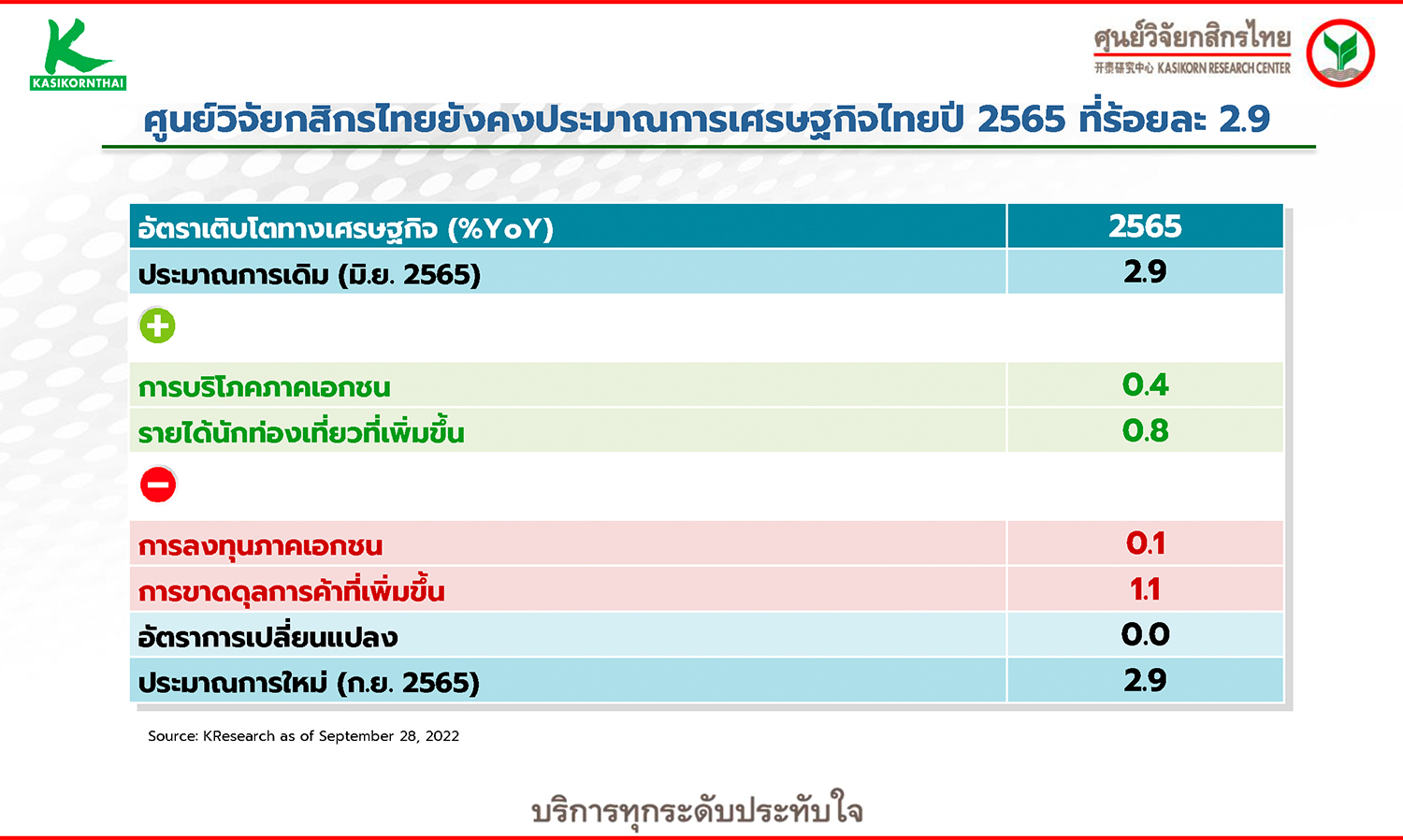

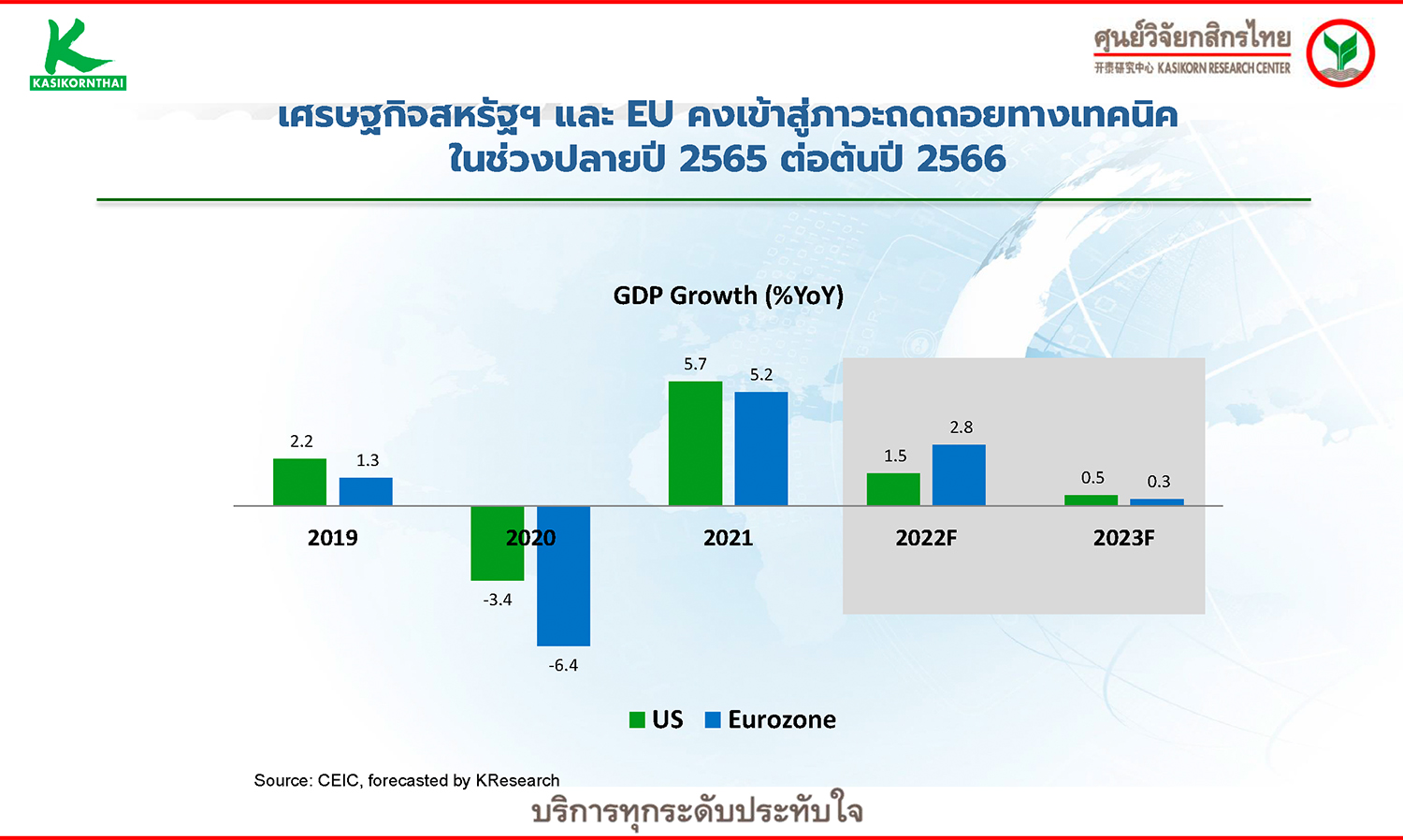

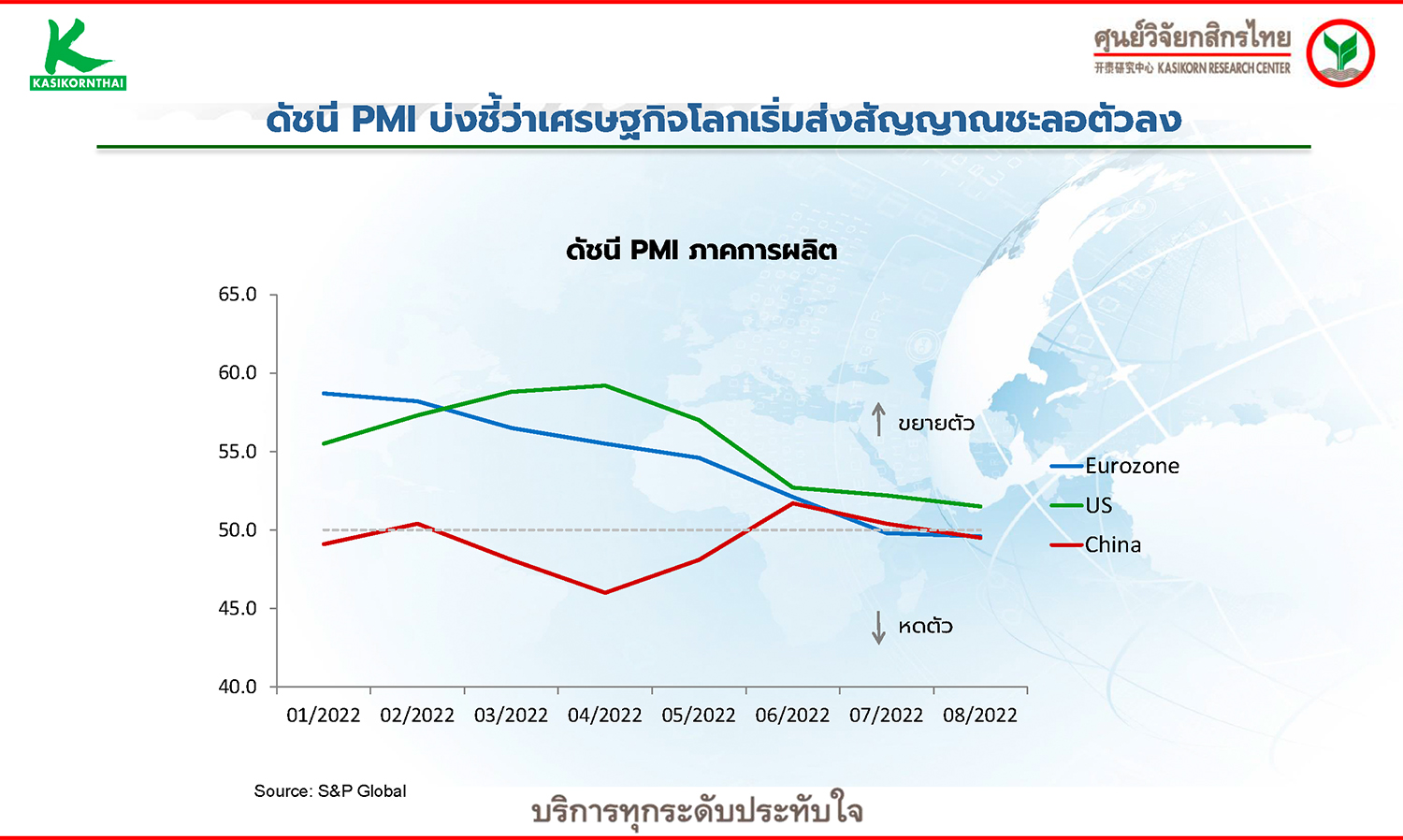

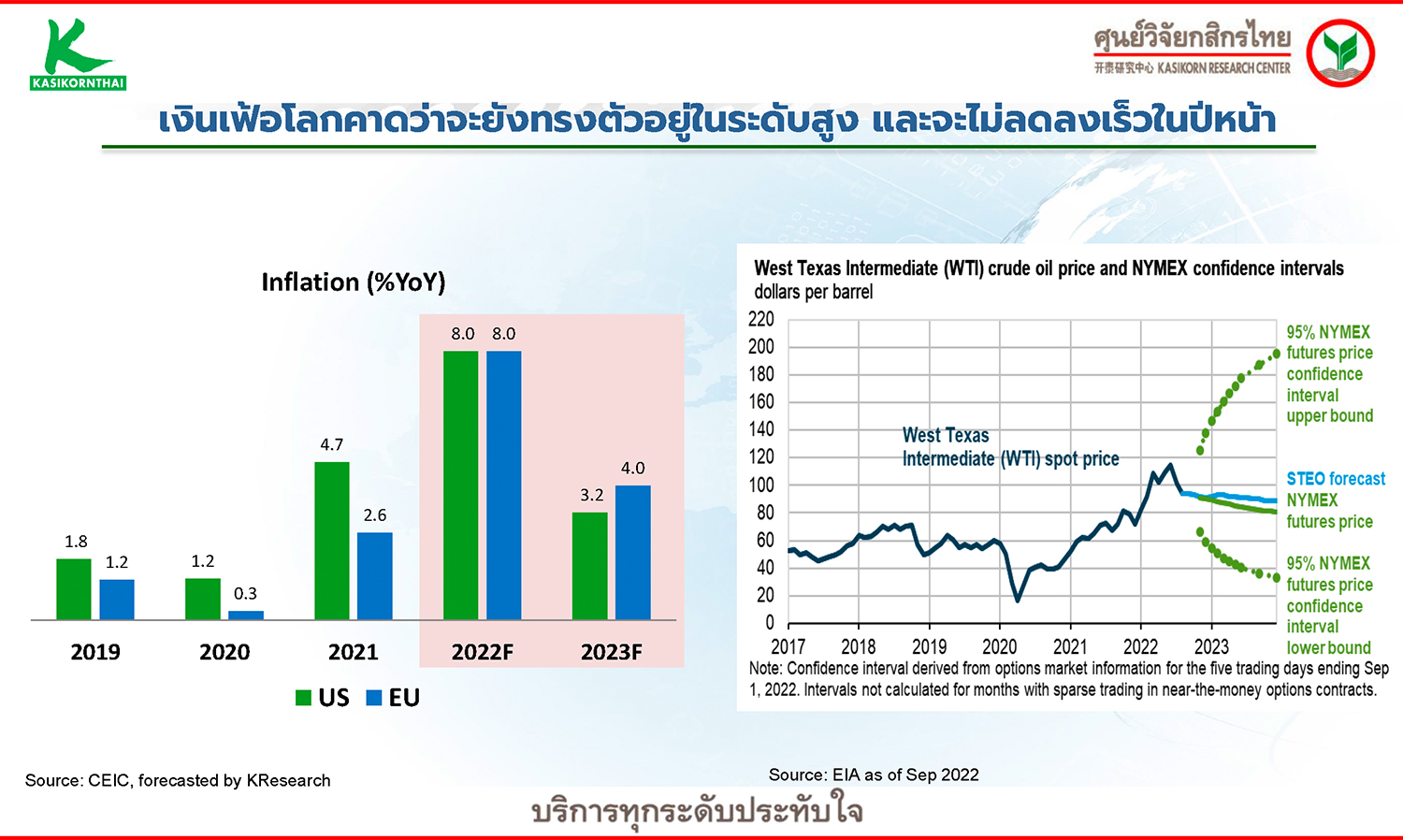

Ms. Natthaporn Treeratnasirikul, Deputy Managing Director of Kasikorn Research Center Co., Ltd., believes that by the end of 2022 and into early next year, the U.S. economy is likely to enter a technical recession again, similar to Europe, which is expected to experience a quarter-on-quarter contraction for two consecutive quarters. This reduces expectations for Thailand's recovery driven by exports. Additionally, global inflation is not expected to decrease quickly, pressured by prolonged international political issues. Therefore, Thailand's economy for the remainder of 2022 and into 2023 will primarily rely on the recovery of tourism, with an estimated number of tourists this year at 9.75 million, up from the previous estimate of 7.2 million. For 2023, the number of tourists is expected to rise to between 13.0 and 20.0 million, which is still significantly lower than the pre-COVID level of 40 million. Overall, Kasikorn Research Center maintains its GDP forecast for 2022 at 2.9%. Although GDP is expected to accelerate to a range of 3.2-4.2% in 2023, there are still several risk factors to monitor, including inflation, interest rate hikes, and the slowdown of economies in several trading partner countries.

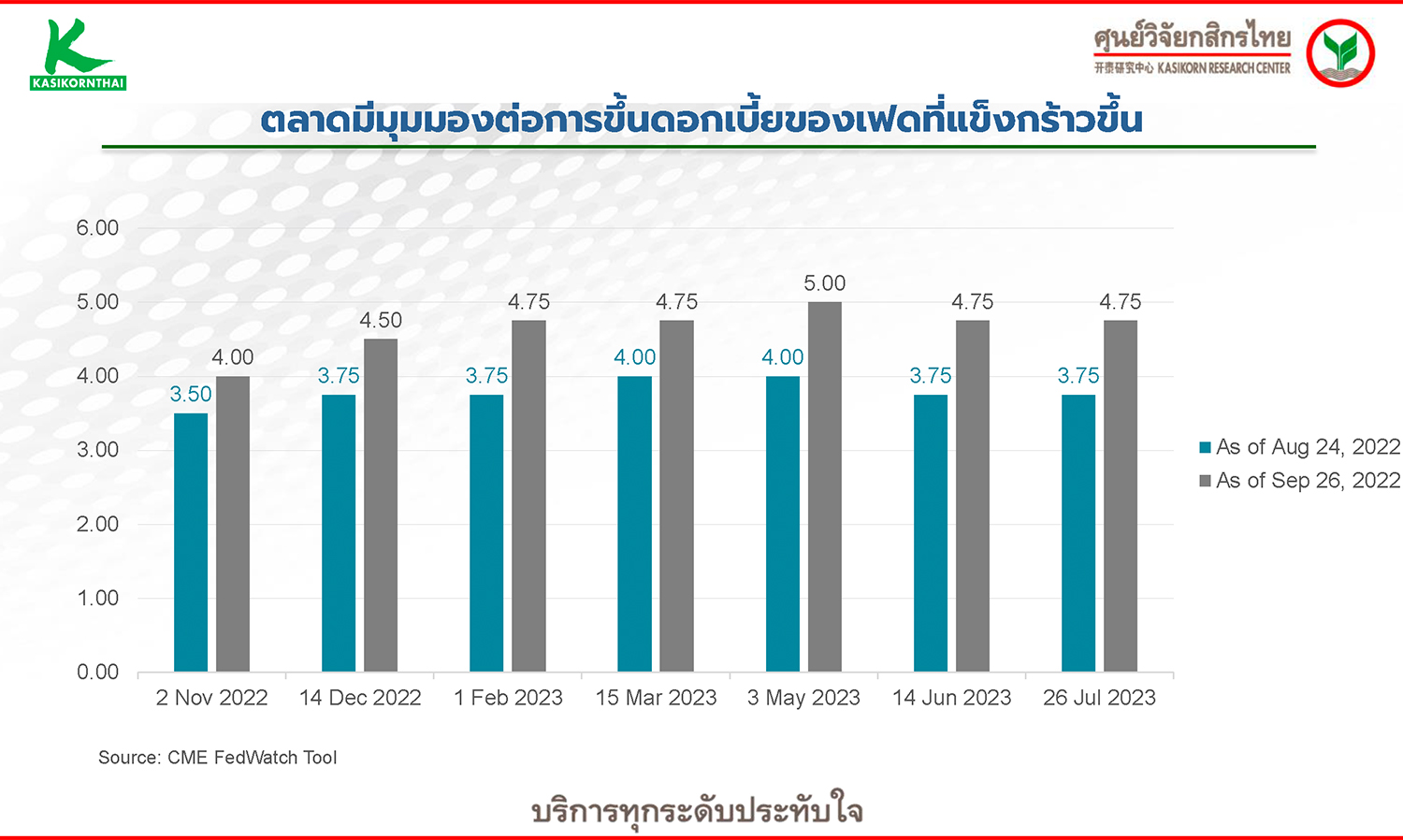

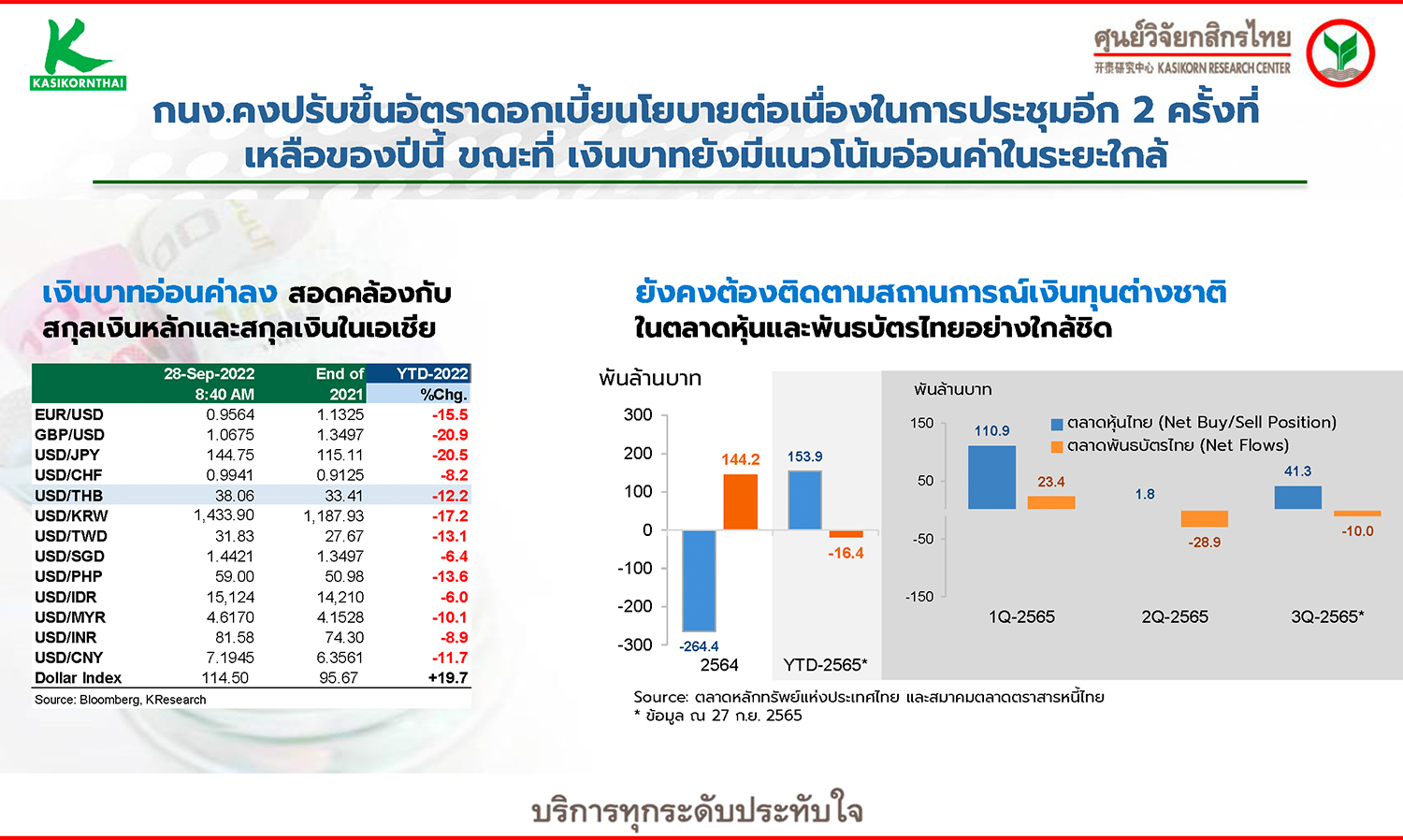

Regarding interest rate trends, it is expected that the Federal Reserve will continue to raise interest rates in the remaining two meetings of this year, potentially extending into early next year, depending on the strength of inflation and the size of each rate hike. Meanwhile, Thailand's policy interest rate is likely to continue to rise at least until the first quarter of 2023, albeit at a gradual pace. The Thai baht is expected to remain weak for the rest of 2022 as long as the U.S. dollar is supported by the Fed's interest rate hikes.

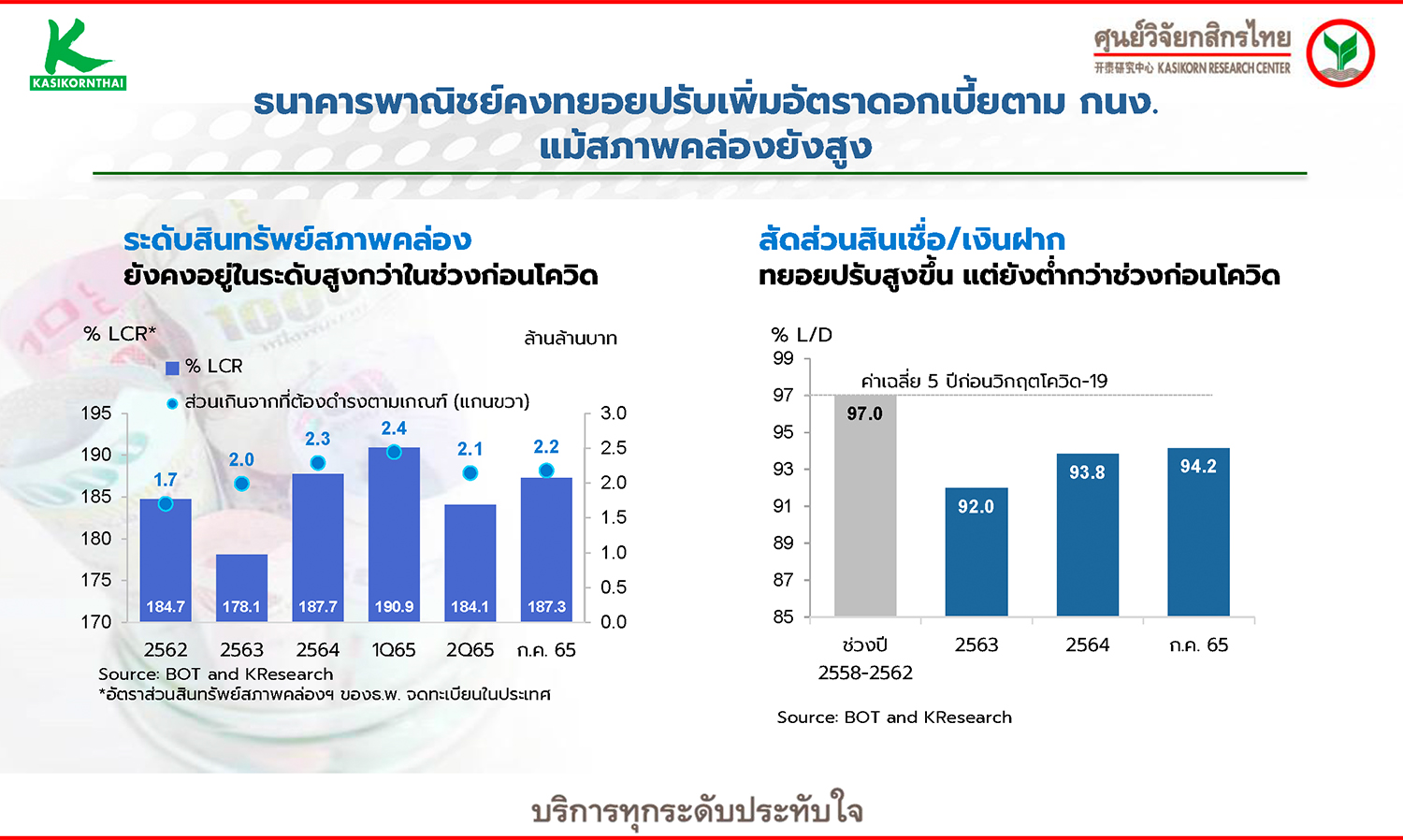

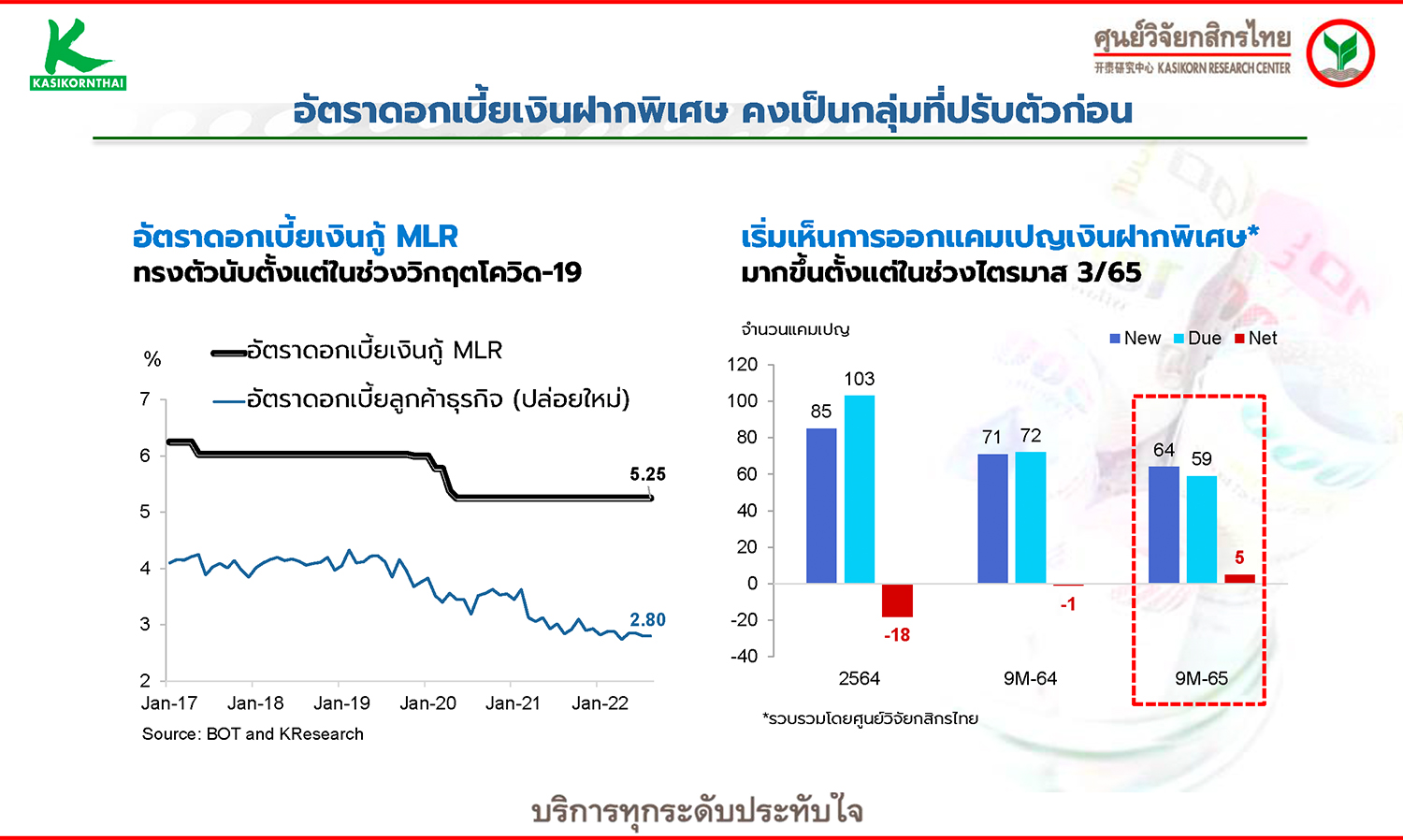

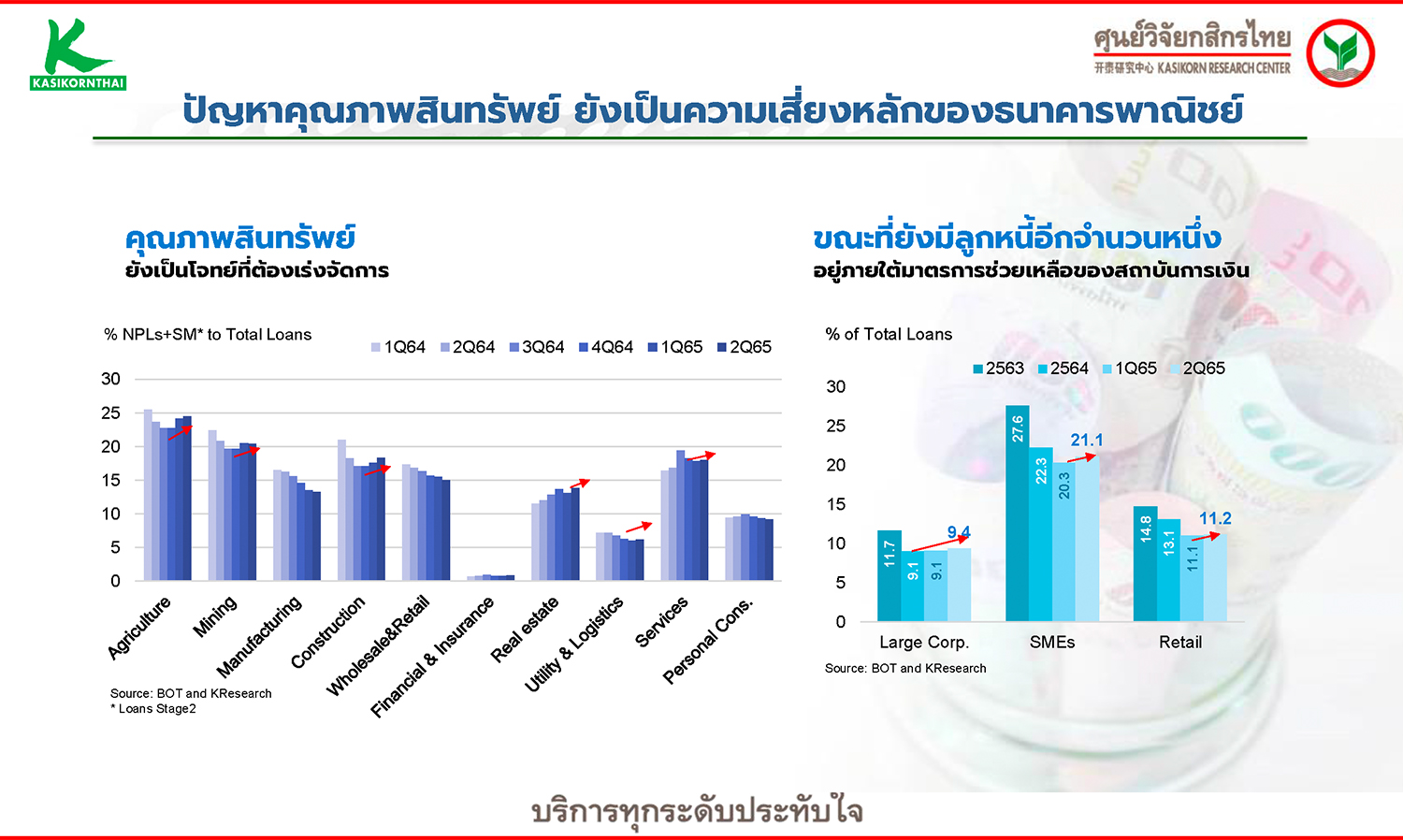

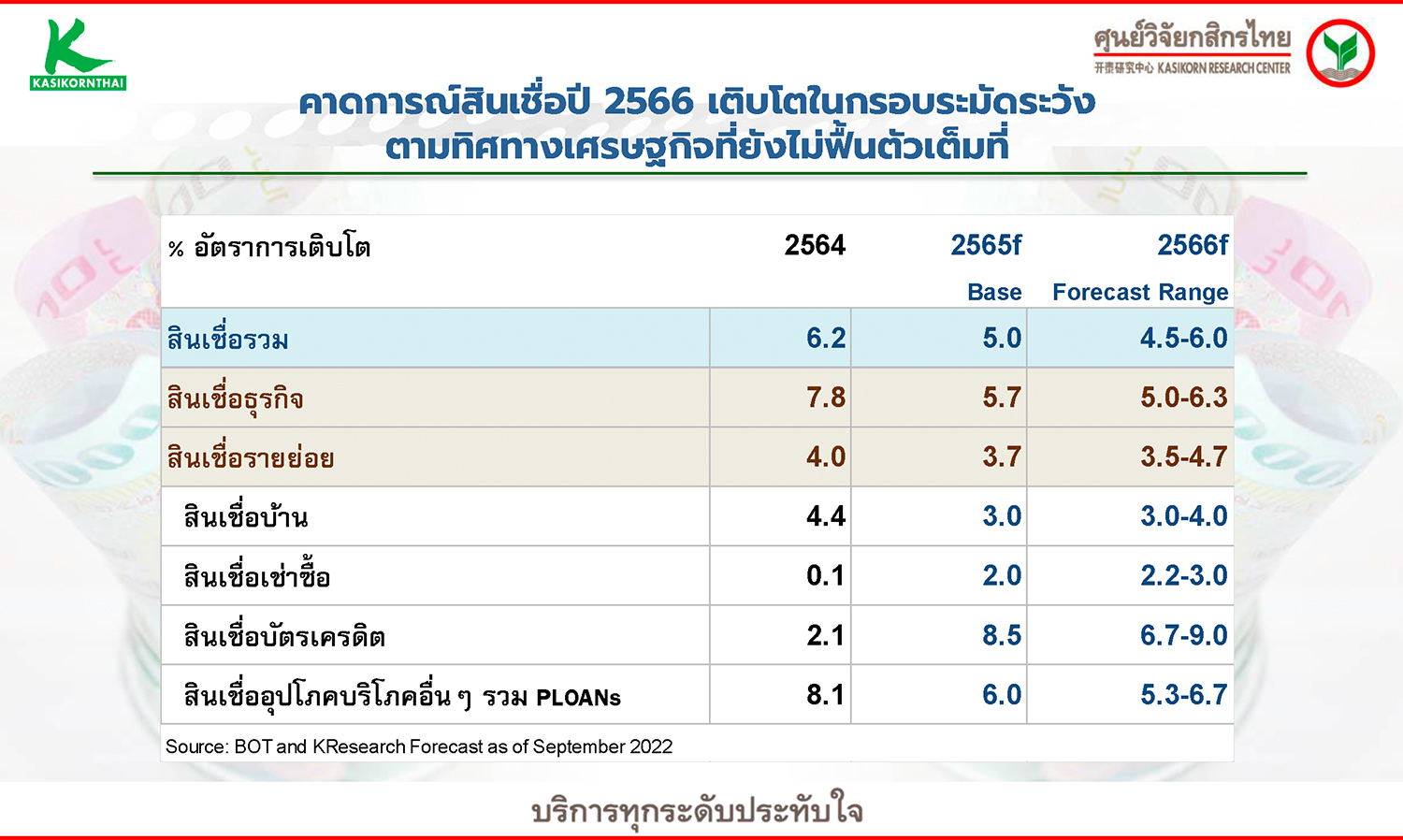

Ms. Thanyalak Watcharachaisurapol, Deputy Managing Director, observes that the signals of the Bank of Thailand's policy rate hike, combined with the adjustment of the contribution rate to the rehabilitation fund back to 0.46% starting in early 2023, will likely lead commercial banks to gradually raise their fixed deposit and standard loan rates. Although liquidity remains high, the expectation is that higher interest rates will not lead to a rapid surge in non-performing loans (NPL Cliff) as commercial banks are proactively restructuring and managing debts. However, the quality of loans and customer assistance still need to be closely monitored. Kasikorn Research Center forecasts the ratio of non-performing loans to total loans in the banking system to be in the range of 2.90-3.10% by the end of next year, compared to 2.88% at the end of Q2 2022. The outlook for loans in the Thai banking system is expected to grow in the range of 4.5-6.0% in 2023, compared to an estimated 5.0% this year, which is not very high amid ongoing economic uncertainties.

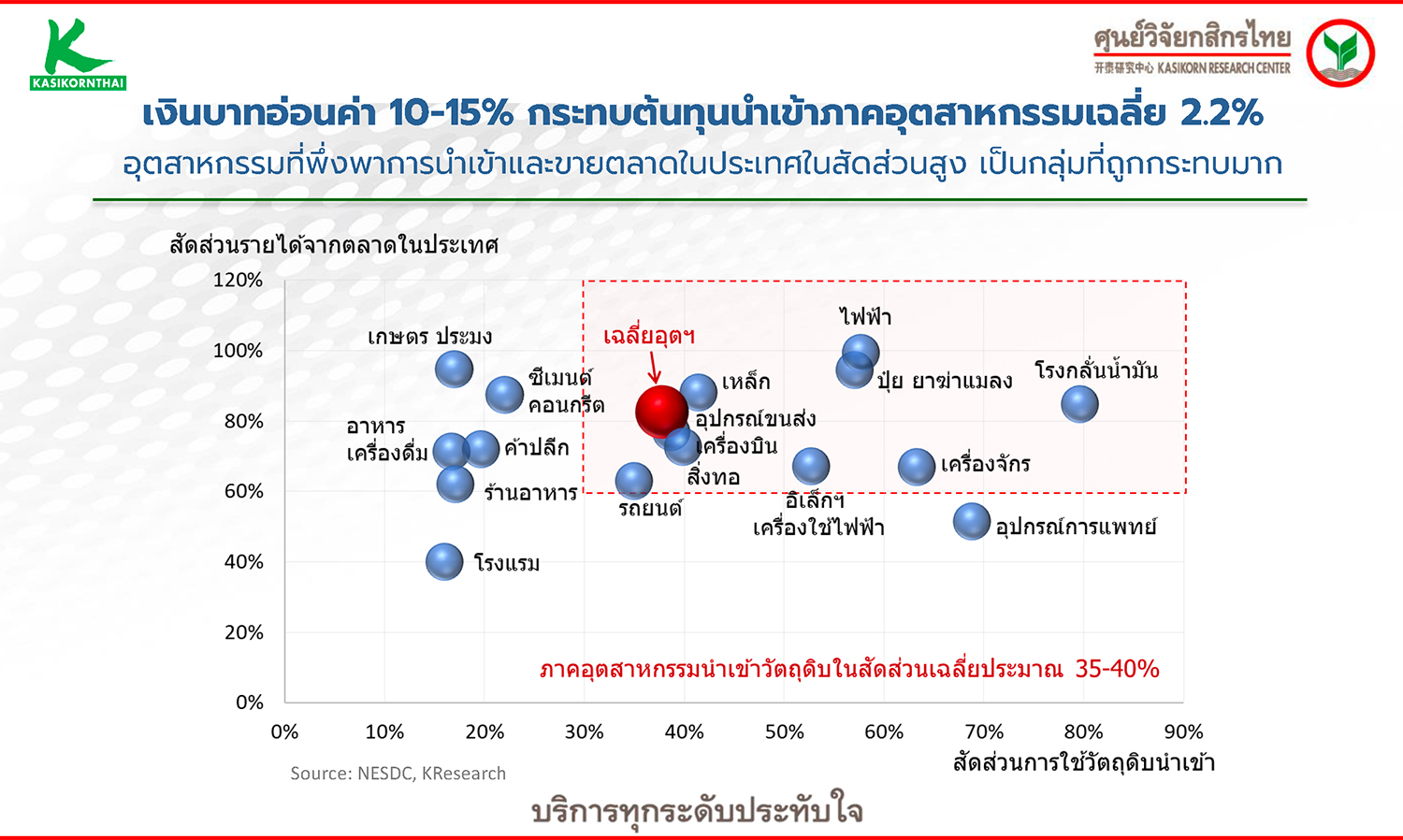

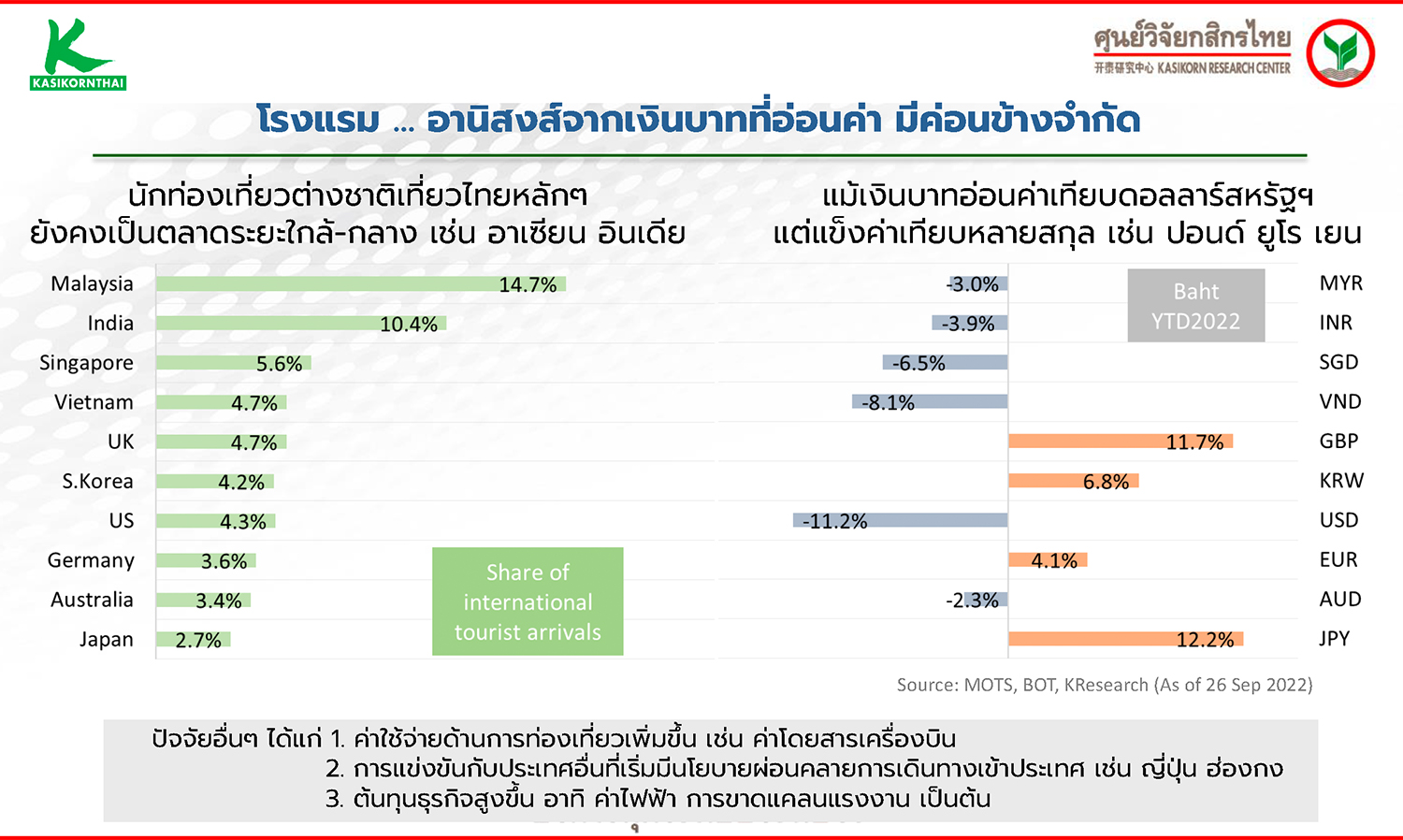

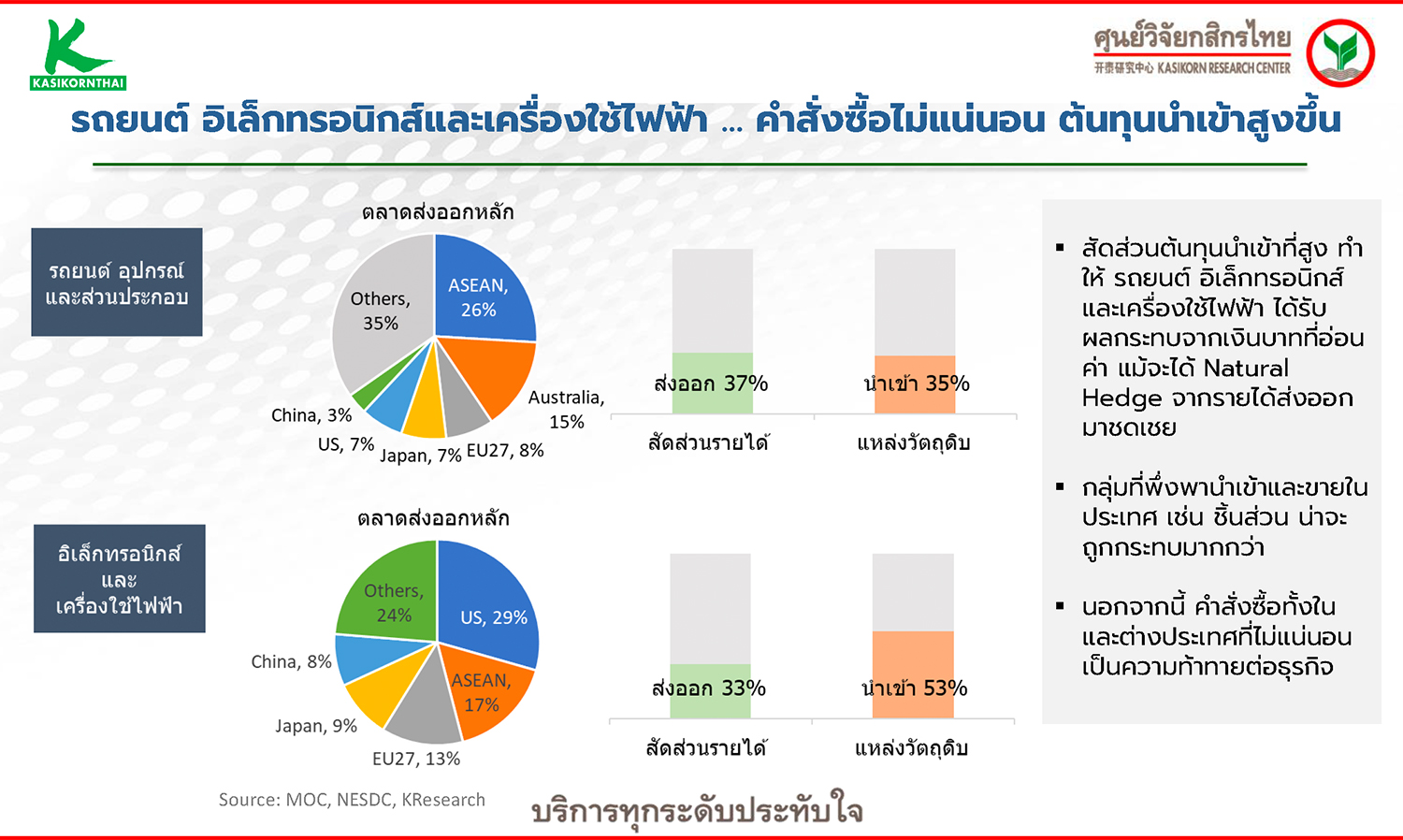

For most industries for the remainder of this year and into 2023, Ms. Kewalin, Deputy Managing Director, believes they will still face significant challenges, particularly from the slowdown of major economies that are key trading partners of Thailand. This means that export-dependent industries may not fully benefit from the weaker baht. The tourism sector faces similar issues, as major tourist markets are dealing with weak currencies and some countries are at risk of economic recession. Additionally, high energy prices are driving up airfare and other expenses, which all affect travel and spending decisions. The depreciation of the baht by 10-15% is expected to impact the average cost of imports in the industrial sector by about 2.2%. Therefore, this presents a challenge that the industrial sector must prepare for, and the path to recovery next year is still not expected to be smooth.