January Exports Kick Off with Continued Growth Despite Short-Term Slowdown Signals from Omicron; Russia-Ukraine War Yet to Impact but Remains a Watchpoint

The value of exports in January 2022 grew by 8% YOY, slowing down from the previous month's 24.2%, while imports expanded by 20.5%, down from 33.4% in the prior month. This resulted in a trade deficit of $2,526.4 million in the first month of 2022. The Ministry of Commerce has not yet released detailed data on exports and imports by product for January as it is currently updating the statistical codes according to customs tariffs, a process conducted every five years, which is expected to be completed by the end of the first quarter of 2022. For market-specific exports, the Ministry reported that exports to India, Russia, the United Kingdom, South Korea, and the United States were the top five markets with the most significant growth.

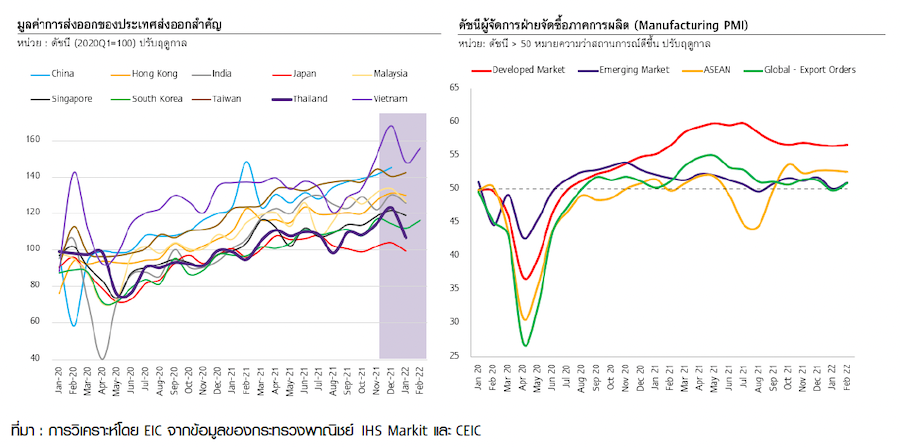

Exports in the first month of 2022 grew by 8%, a slowdown from the previous month's 24.7%. When compared to December (seasonally adjusted), exports contracted by as much as -15.2% (MOM, SA), consistent with the export values of several major countries worldwide (Figure 1 left), as well as a slowdown in manufacturing activity in January, reflected in the Global Manufacturing PMI – export orders index dropping below 50 for the first time in 17 months, and the Manufacturing PMI index declining in both developed and developing countries (Figure 1 right). This is expected to be impacted by the global Omicron outbreak situation in recent times. However, exports in the near future still show positive trends, as indicated by the latest figures in February where the Global Manufacturing PMI – export orders index returned above 50 again, and the export values of Vietnam and South Korea in February accelerated compared to January on a seasonally adjusted basis.

Figure 1: Thailand's exports in January 2022 grew at a slowing rate, consistent with many countries worldwide and the Manufacturing PMI index that declined in January

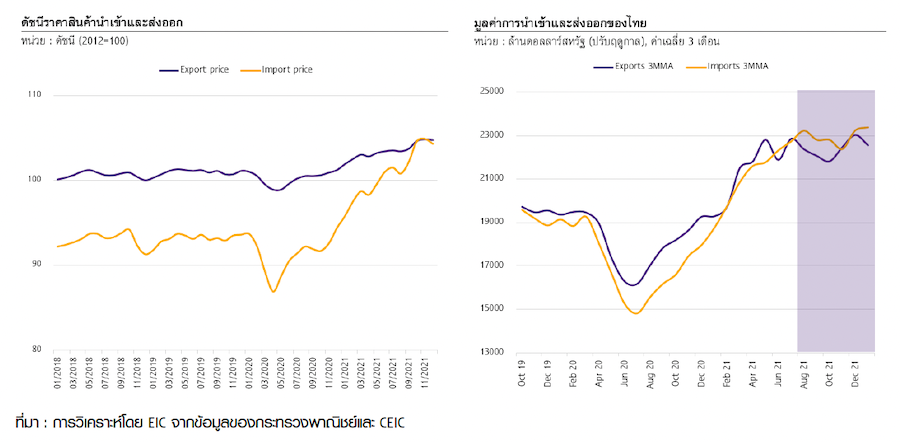

Thailand's trade balance may decrease in 2022 due to the value of imports growing at a higher rate than exports recently, coupled with import prices rising more than export prices (Figure 2). This is partly due to commodity prices, especially energy prices, which remain volatile and at high levels due to supply issues that may escalate from the war between Russia and Ukraine, along with anticipated increased energy demand as global demand recovers.

Figure 2: Comparison of Thailand's imports and exports in recent times

EIC is currently reassessing the export forecast for 2022, expecting that Thailand's exports in 2022 will benefit from (1) the continuous recovery of the global economy and trade, particularly in developing countries where economies are gradually recovering and are likely to rebound faster than previously anticipated due to the less severe impact of Omicron than originally estimated; (2) the value of exports related to oil that may increase in line with global energy prices; and (3) in the future, benefits from participation in the Regional Comprehensive Economic Partnership (RCEP), which is the largest free trade agreement in the world that came into effect in early January 2022.

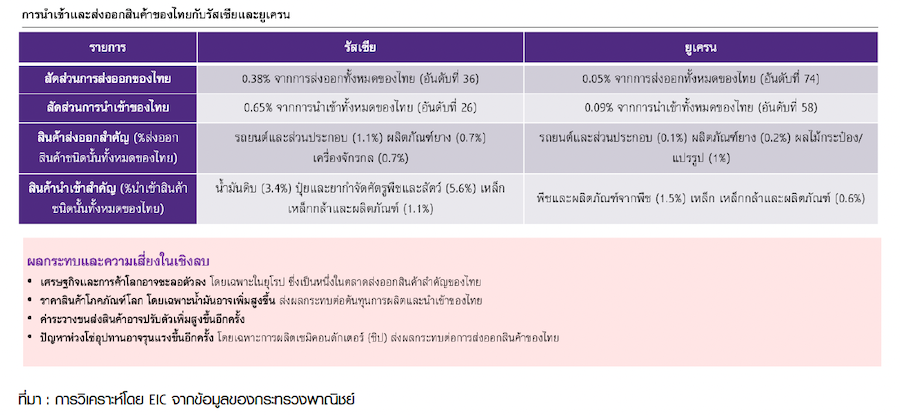

The direct impact of exports to Russia and Ukraine on Thailand's overall exports will be limited, but the ongoing effects of the Russia-Ukraine war need to be monitored closely. Although the war between Russia and Ukraine, along with international sanctions against Russia, has not yet significantly impacted Thailand's international trade, as the value of Thai exports to Russia and Ukraine accounts for only 0.43% of total exports, the Russia-Ukraine war remains a closely watched factor that could affect Thailand in several ways: (1) The war and sanctions may slow global economic and trade growth, especially in Europe, which is a significant export market for Thailand, as exports to European countries, including the EU, the UK, and the European Free Trade Association (EFTA), account for 9.9% of Thailand's total exports; (2) Russia and Ukraine are major producers of oil and natural gas, as well as important agricultural products such as fertilizers, corn, wheat, barley, and sunflower oil, which could lead to Thailand importing these goods for industrial, agricultural, and livestock production at higher prices, potentially worsening the trade balance; (3) Russia and Ukraine are major global producers of palladium and neon gas, which are essential components in semiconductor (chip) production, potentially prolonging the semiconductor shortage more than expected, affecting the production and export of electronics, electrical appliances, and automobiles from Thailand; (4) Shipping freight rates may remain higher than anticipated. However, retaliatory measures between Russia and Western countries may provide opportunities for certain Thai products to penetrate markets previously served by Russian and Ukrainian exports, such as cassava (to replace corn) and certain ready-to-eat foods.

Given the rapidly evolving global situation, EIC will reassess the export forecast for Thailand in 2022 and publish it in March.

Figure 3: Trade between Thailand and Russia and Ukraine

Analysis by: https://www.scbeic.com/th/detail/product/8115