Understanding Cash Buffer Days: A Survival Indicator for Businesses Facing Revenue Shortfalls

During the ongoing COVID-19 situation, businesses across various industries are facing risks due to a lack of revenue after the government announced temporary closures of certain establishments starting March 22. This includes entertainment venues, cinemas, shopping malls, sports arenas, gyms, dine-in restaurants, amusement parks, and educational institutions.

The temporary shutdowns have led to a loss of income for businesses, which may result in closures due to insufficient cash flow to cover ongoing expenses such as rent, raw materials, and employee wages. Cash Buffer Days is one of the indicators that can determine how long a business can operate without revenue.

What are Cash Buffer Days?

Cash Buffer Days refers to the number of days a business can continue to operate or cover its expenses without any cash income. This is calculated by taking the amount of cash available in the business's bank account or savings account and dividing it by the cash outflow or expenses the business must pay to operate, such as rent, raw materials and equipment, wages, owner withdrawals for personal savings, loan repayments, and taxes.

The Cash Buffer Days for each business varies based on the nature of the business, including its size, industry sector, and whether it is labor-intensive or capital-intensive.

Cash Buffer Days is an important indicator of how well a business can operate during crises that impact its revenue, especially for small businesses that have limited access to loans or funding sources. This makes cash flow a crucial indicator of a business's liquidity, and Cash Buffer Days effectively reflects the liquidity and financial buffer of small businesses, helping owners better understand their financial situation.

How many Cash Buffer Days do small businesses have?

SMEs are a vital part of the economy and represent a significant portion of businesses in many countries. However, the market share of SMEs has been steadily declining, raising concerns about their survival in situations that reduce revenue. Cash Buffer Days reflect the liquidity and financial buffer of SMEs, allowing the government to better understand their operational capabilities.

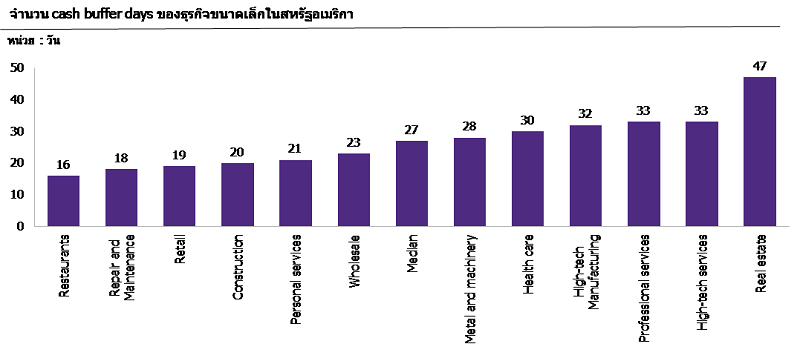

According to a report by JPMorgan Chase & Co. Institute titled "Cash is King: Flows, Balances, and Buffer Days," published in September 2016, which studied data from 597,000 businesses in the United States across 12 industries from February to October 2015, it was found that small businesses in the U.S. have a median Cash Buffer Days of only 27 days. This means that if small businesses in the U.S. experience a lack of revenue, the cash in their accounts will only sustain operations for 27 days. Additionally, JPMorgan found that half of small businesses in the U.S. have Cash Buffer Days of less than one month, and 25% have Cash Buffer Days of less than 13 days.

When analyzed by industry, it was found that small businesses in the real estate sector have the highest median Cash Buffer Days at 47 days, followed by high-technology businesses such as high-tech services and industries.

In contrast, restaurants, repair businesses, and retail have the lowest median Cash Buffer Days at 16, 18, and 19 days, respectively.

Labor-intensive businesses have fewer Cash Buffer Days compared to capital-intensive businesses (23 days vs. 38 days), and industries with lower wages have fewer Cash Buffer Days than those with higher wages (19 days vs. 31 days).

In Thailand, according to data from the Department of Business Development, there were 730,000 SMEs in 2018, accounting for 98.3% of all businesses. Reports from the Office of Small and Medium Enterprises Promotion indicate that the value of SMEs in the same year represented 43.0% of GDP. Therefore, SMEs are a focus for the government, with more than half of small businesses in the service sector having Cash Buffer Days of less than 60 days, particularly in the hotel and restaurant, education, information, and real estate sectors.

Source: JPMorgan Chase & Co. Institute

What are the risks for businesses with low Cash Buffer Days?

One of the challenges for SMEs is managing liquidity, which is essential for business operations and supports future growth. Therefore, having a longer Cash Buffer Days is necessary for managing liquidity and serves as a financial buffer during crises that impact revenue, especially for SMEs that have more limited access to funding compared to larger businesses that may have reserves from loans or equity financing.

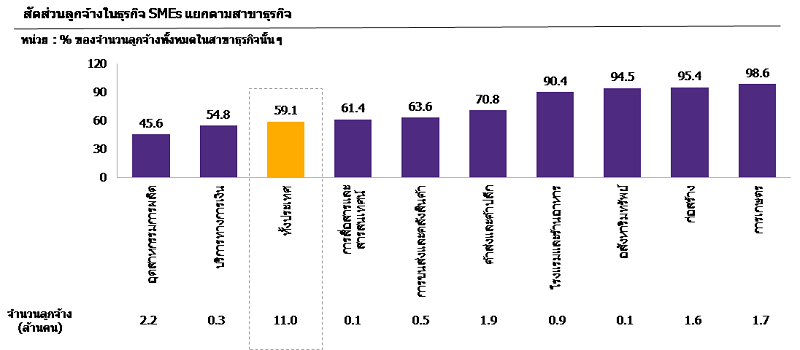

A low Cash Buffer Days reflects reduced liquidity and financial buffer. When faced with tight situations, such as economic crises or pandemics that reduce revenue, or when certain sectors must temporarily cease operations, low Cash Buffer Days increase the risk of business closures. This risk affects both business owners and employees, particularly in the SME sector, which has more limitations in accessing various funding sources compared to larger businesses. Over 11 million workers in Thailand are employed in SMEs, accounting for 59.1% of all employees, making this group vulnerable to the impacts if SMEs must close due to insufficient cash reserves and inability to secure loans during revenue shortfalls.

It is evident that Cash Buffer Days is a crucial indicator of the survival of small businesses. Therefore, the government should implement policies to support businesses in managing their liquidity appropriately, encouraging them to increase their financial buffers, and providing education on cash flow management and Cash Buffer Days to business owners to cope with crises without relying on credit sources.

However, the government should also have measures to assist businesses, particularly in facilitating access to funding sources to help sustain them during economic downturns or situations that lead to reduced or lost revenue, such as emergency loans without collateral for small businesses, deferring or postponing debt repayments for small businesses, or allocating storage facilities for exporters during times when they cannot export.

Source: Analysis by EIC based on data from the National Statistical Office