What Has Happened in the Thai Real Estate Sector Over the Past 30 Years?

We must honestly acknowledge that the year 2020 has been a challenging one for all sectors of business. Not only has the real estate sector shown signs of stagnation since 2019, but this year appears to be particularly severe, affecting both small and large players alike. Currently, everyone is in a "SAVE MODE" as purchasing power has diminished, and people are starting to feel insecure about their income, especially in the middle to lower market segments, which make up a significant portion of the property sector.

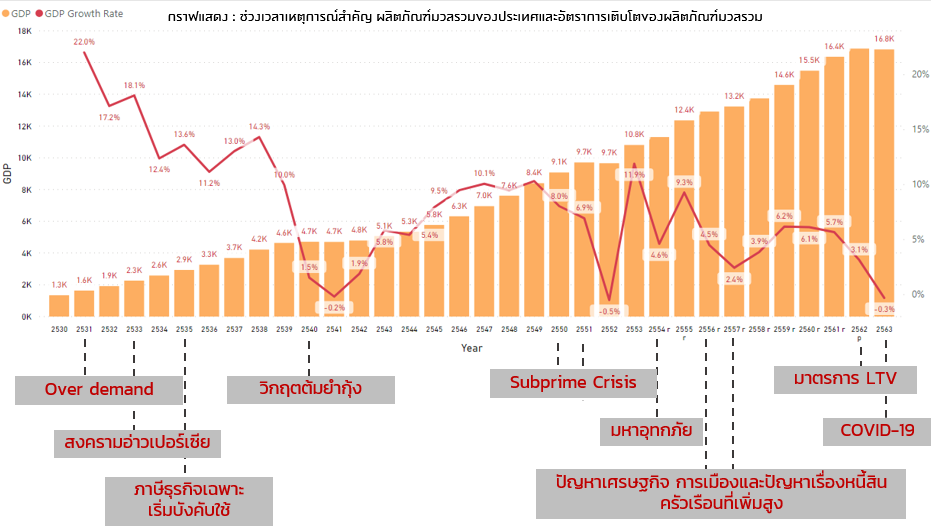

However, it is important to note that this is not the first time the Thai real estate sector has faced such a heavy crisis. In fact, if we focus on the past 30 years, we can see that our real estate business has gone through numerous challenges, including economic downturns, natural disasters, and government policies. Today, TerraBKK has compiled these events to take everyone back in time to see what the Thai real estate sector has faced over the past 30 years and how each company has adapted after each crisis.

1988-1990 | OverDemand

This period marked the golden age of real estate, as major world powers signed the Plaza Accord Agreement, leading to an over-demand in the Thai economy and speculation that resulted in business expansion. Additionally, this was a time when the industrial sector's gross domestic product clearly surpassed that of agriculture.

1991 | Gulf War

Following the growth era of real estate, the Middle East crisis (Gulf War) occurred, causing a slowdown in production in both the financial and real estate sectors, as most loans from financial institutions were not released for real estate project development.

1997 | Tom Yum Kung Crisis

It is well-known that Thailand faced a historic crisis known as the Tom Yum Kung crisis, where the Thai baht depreciated, leading to a bubble burst in the real estate market characterized by oversupply and speculation across all property types. Developers faced significant debt burdens, and many small and medium-sized developers went out of business.

For example, the Sathorn Unique project, which was 90% completed, faced issues when the financial institution that lent money to the project went bankrupt, leading the government to suspend funding for the Sathorn Unique project, causing construction projects across Bangkok to come to a halt.

LPN adapted by selling assets and land, reducing staff, and accelerating construction to complete projects within a year to bring cash flow back into the company.

Pruksa adjusted its strategy to deliver projects to customers on time by introducing pre-cast housing innovations that sped up construction, giving Pruksa a competitive edge. In 2004, Pruksa established its own Pruksa Precast Concrete Factory for all its projects.

Land & Houses and Muang Thai adopted a strategy of building homes before selling them to instill confidence in customers, focusing on buyers who would transfer ownership immediately to increase liquidity and reduce the company's interest burden.

2007-2008 | Subprime Crisis

Many are familiar with the Hamburger crisis or Subprime Crisis, which stemmed from the bankruptcy of U.S. real estate lending companies, impacting the real estate business in Thailand. This created liquidity risks for developers reliant on foreign funding and increased financial costs as domestic financial institutions became more cautious in approving loans.

AP adjusted its policy by immediately canceling reservations that did not pass loan applications, allowing properties to be resold more quickly.

Pruksa launched a business for buying and selling second-hand homes to support the sale of its own projects.

2011 | Major Flood

This flood was the largest and most severe in 50 years, causing significant damage to homes and at least 1 million housing projects. The real estate business slowed considerably, and most brands focused on selling properties in areas that were not flooded to restore consumer confidence.

Pruksa adjusted its strategy to develop more urban areas, moving away from its previous dominance in Rangsit and Bang Bua Thong.

Supalai began opening more projects in inner Bangkok and focused on launching projects in major provinces, as many Bangkok residents sought to buy or rent vacation homes during the floods.

Property Perfect offered a campaign where customers buying homes received free flood insurance, covering cases where water entered the house.

Sansiri adapted by focusing on expanding into provincial areas, such as Hua Hin, Phuket, Chiang Mai, and Khao Yai, emphasizing vacation homes or second homes for weekend relaxation.

2013-2014 | Economic and Political Issues

After recovering from the flood crisis, economic and political issues arose, along with rising household debt, leading to decreased purchasing power and hesitance among consumers in deciding to buy homes. The real estate market faced fierce competition, prompting many large developers to shift their business plans towards developing cheaper condominium projects.

Pruksa expanded projects into potential provincial areas.

Q House targeted markets with real demand, focusing more on horizontal projects.

2019 | LTV

The Bank of Thailand enforced LTV measures to prevent speculation and investment in real estate, impacting consumer purchasing power and making project sales more challenging. This particularly affected the condominium market as investors disappeared, including the mid-to-high segment targeting families or newlyweds, who often already owned condominiums, making it harder to secure loans for a second property.

Sansiri shifted focus to horizontal properties, including single-family homes, duplexes, and townhomes, while reducing new launches and seeking new foreign customers.

Supalai adjusted its strategy to target middle-income customers looking to buy homes for actual living or renting, with average selling prices ranging from 60,000 to 80,000 baht per square meter.

AP increased its focus on horizontal markets and launched projects across all brands in every segment, emphasizing affordable products for consumer accessibility.

Land & Houses focused solely on horizontal projects, with no new high-rise developments, generating income from other businesses such as land sales and property leasing.

Pruksa expanded into new provinces and adjusted its development plan from low-rise condominiums to high-rise projects, extending down payment periods to 18-24 months, while also increasing the down payment period for horizontal homes to 4-6 months.

2020 | Economic Recession and Covid-19 Pandemic

Amidst an economic recession due to a global slowdown, LTV measures, high household debt, land and property taxes, and the outbreak of Covid-19, consumer purchasing power has been affected, reducing consumer confidence in Thailand and causing a slowdown in foreign investment. Additionally, as people began to stay home, visiting sales galleries became increasingly difficult, resulting in almost no sales opportunities. Consequently, many companies started adapting by selling homes and condominiums online, revolutionizing the home/condo buying process from site visits to online reservations, thus increasing sales channels.

Pruksa focused on selling existing stock of condominium projects, selectively launching new projects only in high-potential locations, expanding the market to potential customer segments, and investing in low-rise condominiums and horizontal properties to achieve quicker returns.

Land & Houses improved internal efficiency, developing personnel and systems to keep expenses below 15%.

AP reduced its condominium launch plans, downsized projects, studied actual customer demand, expanded its customer base to middle-income levels, and distributed horizontal project developments to provincial areas to mitigate risks.

Sansiri focused more on real demand, creating a brand image that is easily accessible, and established a real-time online condominium sales platform available 24/7, along with extending the transfer period by 1-2 months for Chinese customers on a case-by-case basis.

Supalai targeted new market segments with purchasing power in provincial areas and implemented a three-month payment deferment for customers in professions affected by Covid-19.

LPN created a sales platform via telephone (Telesales) for customer safety and offered project condominiums for rent to generate income.

Sena established the Sena Zero Covid measures to support three customer groups: those who booked properties during the down payment period nearing transfer, new customers wishing to purchase Sena projects during this time through personalized promotions, and current customers by assisting with shopping during quarantine, as well as providing a hotline to take residents to the hospital if they have a fever or suspect they are at risk.

TerraBKK hopes that the Covid-19 pandemic will pass quickly and believes that the real estate sector will soon find ways to adapt to similar situations in the future. It is evident that Covid-19 only recently surged heavily about a month ago, yet many developers have already begun to adapt promptly, whether through online sales or payment deferments. After this crisis, we believe the real estate industry will undergo further changes in terms of sales channels and internal management. Regardless of how severe and prolonged this crisis may be, TerraBKK wishes strength to all businesses to overcome it together.

Graph showing: Timeline of significant events, GDP, and GDP growth rate.