Case Study 23: With This Salary, Which Brand of Detached House Can You Buy?

For those looking to buy a detached house, it’s true that new projects can be expensive. However, if you consider the peace of mind that comes with it—no worries about repairs and better security systems compared to second-hand homes—it can be worth it. What do you think? By the way, what are the current prices of detached houses from various brands? TerraBKK Research summarizes the selling price range or starting price level categorized by project names according to the brand developers as follows:

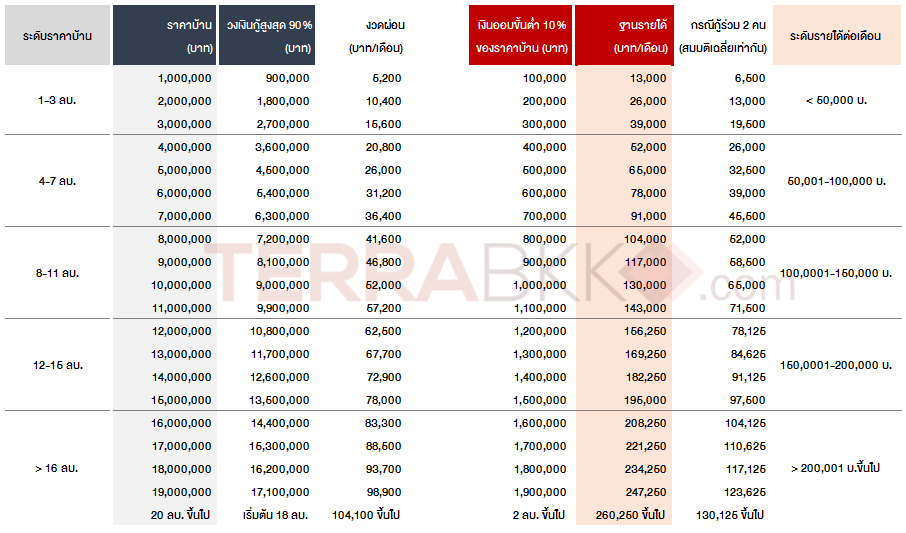

- For this house purchase, you will need to apply for a bank loan, with a maximum loan amount of 90% of the house value

For example, if you buy a house for 5,000,000 baht, the maximum loan amount at 90% would be 4,500,000 baht, meaning you would need to provide 500,000 baht from your own funds. - You must have savings or personal funds of at least 10% of the house price you wish to buy to cover the purchase.

For example, the difference in house price from the loan amount of 500,000 baht above does not include other expenses such as land office fees, etc. - Assuming a loan term of 30 years with an interest rate of 3.5% for the first year, MRR-1.8% for years 2-3, and then MRR-1.25% thereafter (with MRR interest rate = 7.12%), the average monthly payment would be 26,000 baht.

- Debt repayment capacity is typically calculated by banks as 40% of your salary.

For example, a person with a salary that qualifies for a 90% loan on a 5,000,000 baht house, with a monthly payment of 26,000 baht, should have an income of at least 65,000 baht per month (if applying jointly with another person, assuming equal income, each should earn at least 32,500 baht per month).

Based on the above assumptions, when calculating the “house price” along with the “income level”, you will get the following preliminary results table:

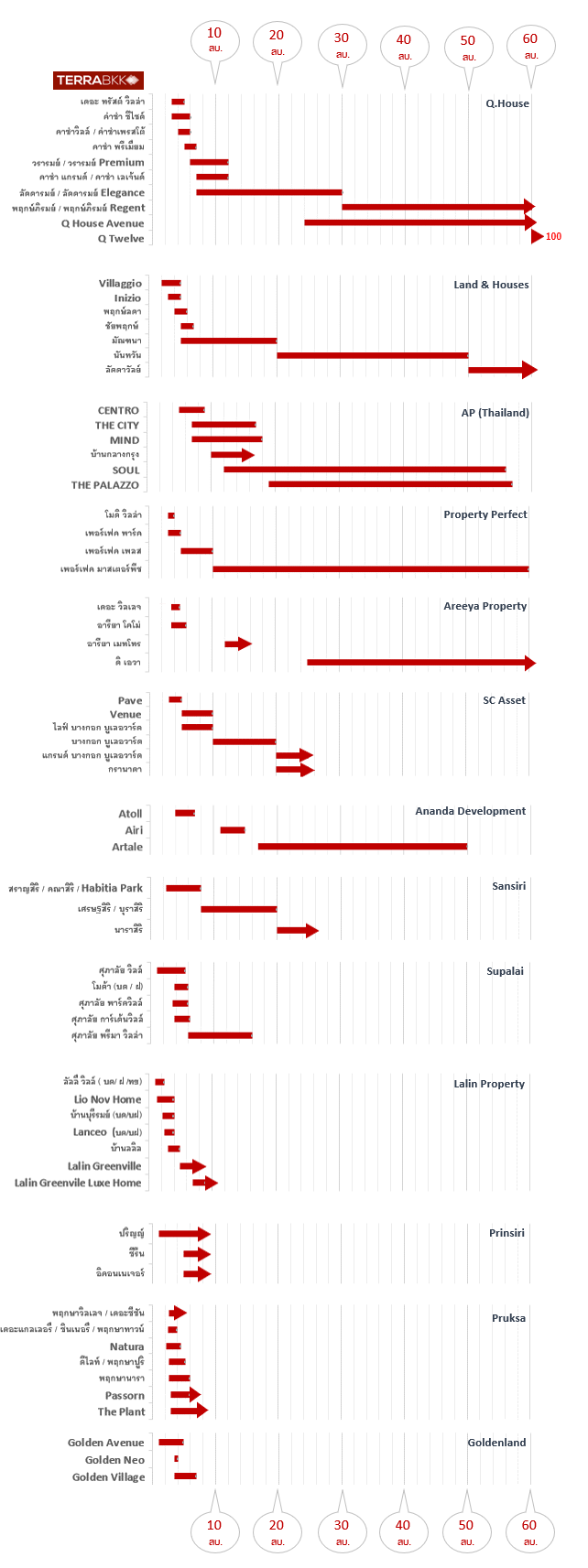

Seeing this, don’t be alarmed that to buy a detached house worth 4 million baht, you need a salary of 52,000 baht, right? TerraBKK suggests considering a joint loan. Assuming both have an average income of 26,000 baht, the possibility of buying that dream detached house may not be out of reach. Therefore, under the above conditions, what brands of houses can you afford? Here’s a list: (Some projects include townhouses, duplexes, and detached houses, so the starting price may not reflect the price of detached houses. Please verify the prices with the respective projects.)

If you have an income level of < 50,000 baht per month, you can buy a house starting from 1-3 million baht, such as:

- Lalin Property brand: Lali Ville / Baan Buriram / Lanceo

- Land & Houses brand: Villaggio / Inizio

- Pruksa brand: Natura / Delight / Pruksa Puri / Pruksa Nara

- Q.House brand: The Trust Villa

- Supalai brand: Supalai Ville

- Goldenland brand: Golden Avenue / Golden Neo

For an income level of 50,001 – 100,000 baht per month, you can buy a house starting from 4-7 million baht, such as:

- AP brand: CENTRO

- Lalin Property brand: Baan Lalin / Lalin Greenville

- Land & Houses brand: Pruksa Lada / Chaiyaphruek

- Property Perfect brand: Modi Villa / Perfect Park / Perfect Place

- Pruksa brand: Passorn / The Plant

- Q.House brand: Casa Ville / Casa Presto / Casa Premium / Casa Seaside

- SC Asset brand: Pave / Venue / Life Bangkok Boulevard

- Sansiri brand: Saransiri / Kanasiiri / Habitia Park

- Supalai brand: Moda / Supalai Park Ville / Supalai Garden Ville

- Ananda Development brand: Atoll

- Prinsiri brand: Prin / Serene / Iconnature

- Areeya Property brand: The Village / Areeya Como

- Goldenland brand: Golden Village

For an income level of 100,001 – 150,000 baht per month, you can buy a house starting from 8-11 million baht, such as:

- AP brand: THE CITY / MIND / Baan Klang Krung

- Lalin Property brand: Lalin Greenville Luxe

- Land & Houses brand: Mantana

- Property Perfect brand: Perfect Masterpiece

- Q.House brand: Casa Grand / Casa Legend / Wararam / Wararam Premium / Laddaram / Laddaram Elegance

- SC Asset brand: Bangkok Boulevard

- Sansiri brand: Setthasiri / Burasiri

- Supalai brand: Supalai Prima Villa

For an income level of 150,001 – 200,000 baht per month, you can buy a house starting from 12-15 million baht, such as:

- AP brand: SOUL

- Areeya Property brand: Areeya Metro

- Ananda Development brand: Airi

For an income level of 200,001 baht per month and above, you can buy a house starting from 16 million baht and above, such as:

- AP brand: THE PALAZZO / Baan Klang Muang Classe

- Land & Houses brand: Nantawan / Laddawan

- Q.House brand: Pruksa Piram / Pruksa Piram Regent / Q House Avenue / Q Twelve

- SC Asset brand: Grand Bangkok Boulevard / Granada

- Sansiri brand: Narasiri

- Areeya Property brand: The Ava

- Ananda Development brand: Artale

All of this is just a case study on buying a house with a loan amount under the conditions set by Terrabkk to help readers estimate the initial price of detached houses they can afford. In reality, buying a house with a loan involves other details, such as components of the home loan like interest rates, loan terms, and loan amounts. If the numbers change, the calculations will yield different results. Additionally, the financial situation of the individual matters; for instance, if you have a lot of debt, your repayment capacity varies, and the possibility of buying a house may not align with the prices mentioned above. Or even in cases where one does not rely on home loans, such as having substantial funds and needing minimal loans, the price of the house you can buy may not depend solely on your income level. However, one thing is certain: as time goes on, the prices of detached houses will continue to rise and move further away from the city. In the future, Bangkok may run out of space for new detached house projects. ---TerraBKK