Summary of Real Estate Company Performance for the First Half of 2025

The Thai real estate market in 2025 continues to face ongoing challenges as consumers tend to delay their purchasing and property transfer decisions due to an economy growing slower than actual purchasing power. Additionally, rising land prices, continuously increasing construction costs, and remaining unsold inventory in the market have led to a decline in the performance of Thai real estate companies in the first half of the year, both in terms of revenue and net profit. This reflects the fragility and challenges of the industry, clearly highlighting the impact of the economic environment on consumer purchasing power.

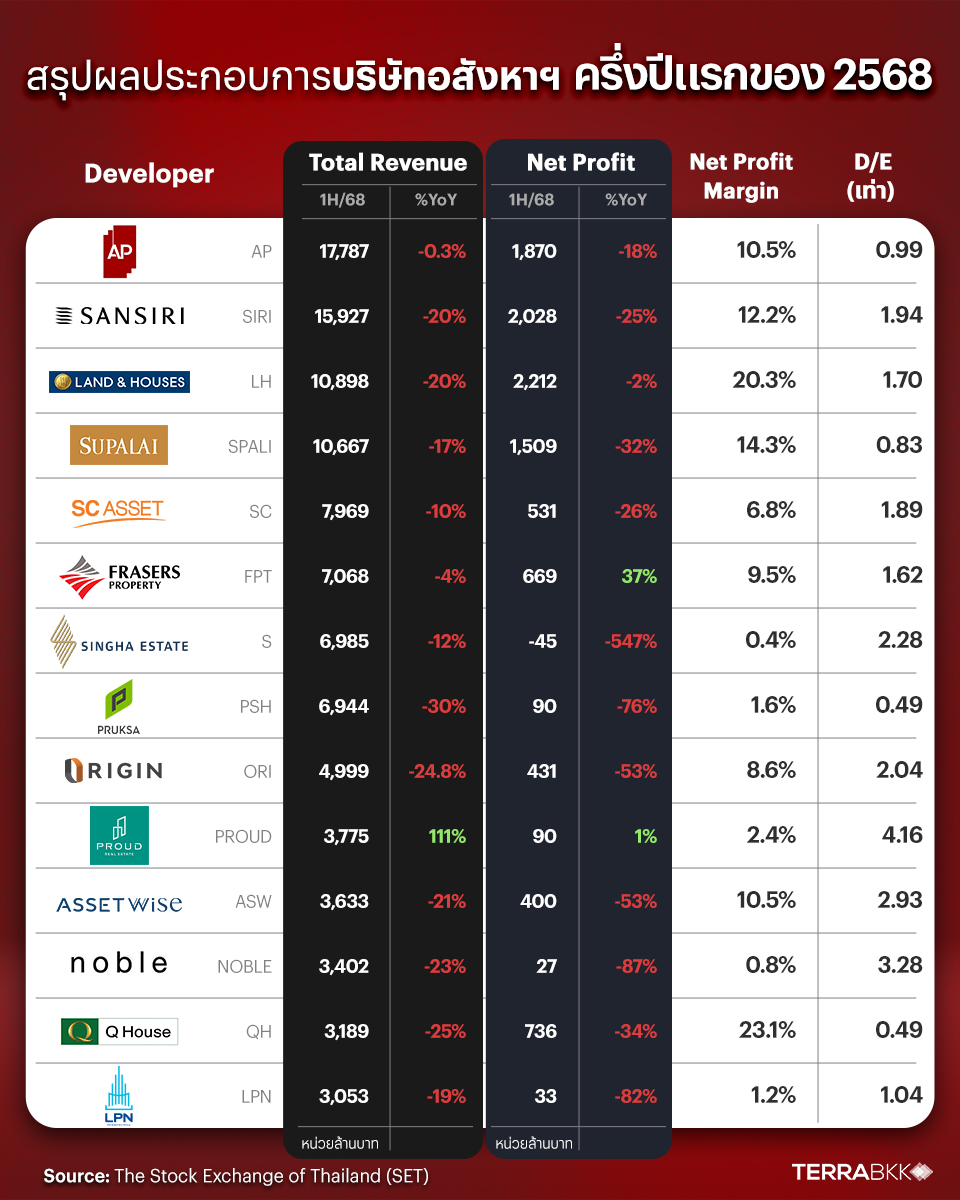

AP Thailand, the market leader with the highest total revenue, reported 17.787 billion baht, showing a slight decrease compared to last year's revenue of 17.846 billion baht. The net profit was 1.870 billion baht, down 18% from the same period last year, with a net profit margin of 10.5%. The debt-to-equity (D/E) ratio stood at 0.99, indicating balanced capital structure management and caution in financial risk management.

Sansiri came in second with total revenue of 15.927 billion baht, a 20% decrease compared to the same period last year, and a net profit of 2.028 billion baht, down 25%. Despite the decline in revenue and profit, Sansiri maintained a net profit margin of 12.2%, which is considered satisfactory. The D/E ratio of 1.94 is not excessively high compared to industry competitors and remains manageable for a large company with ongoing expansion.

Land and Houses ranked third with revenue of 10.898 billion baht, down 20%, but with a net profit of 2.212 billion baht, down only 2%. This demonstrates good cost management ability, allowing them to maintain net profit even in a declining revenue environment, resulting in a net profit margin of 20.3%, one of the highest in the market. The D/E ratio of 1.70 is at a suitable level, reflecting good financial management.

Supalai showed impressive performance considering its cost control efficiency, with revenue of 10.667 billion baht, down 17%, but managed to maintain a high net profit margin of 14.3%, with a net profit of 1.509 billion baht. The D/E ratio of 0.83 indicates balanced debt management and low risk.

SC Asset reported net revenue of 7.969 billion baht, down 10%, with a net profit of 531 million baht, down 26%, and a net profit margin of 6.8%. The D/E ratio of 1.89 is acceptable for the real estate industry. The relatively small revenue decline compared to other companies in the group shows resilience and the ability to maintain market share in a slowing market.

From a financial ratio perspective, Q House stands out with the highest net profit margin of 23.1%, despite having revenue of only 3.189 billion baht and a net profit of 736 million baht, down 34%. This high net profit margin reflects good cost control ability, demonstrating operational efficiency and appropriate pricing strategies, allowing QH to deliver better returns than its industry competitors.

The D/E ratio illustrates the differences in financial management among companies, with NOBLE having the highest D/E ratio at 3.28, indicating high debt usage in operations, while Pruksa has the lowest ratio at 0.49, showing low financial liquidity and debt risk.

The outlook for the Thai real estate market in 2025 continues to face challenges from slow domestic purchasing power recovery. Although the government has introduced supportive measures such as adjusting LTV criteria and reducing transfer fees, positive results have not yet clearly emerged in the short term. Overall, the first half reflects that the Thai real estate industry is undergoing a significant restructuring phase, where companies with strong financial health, effective management, and the ability to adapt to market trends will have opportunities for growth and competitive advantages in the long term.