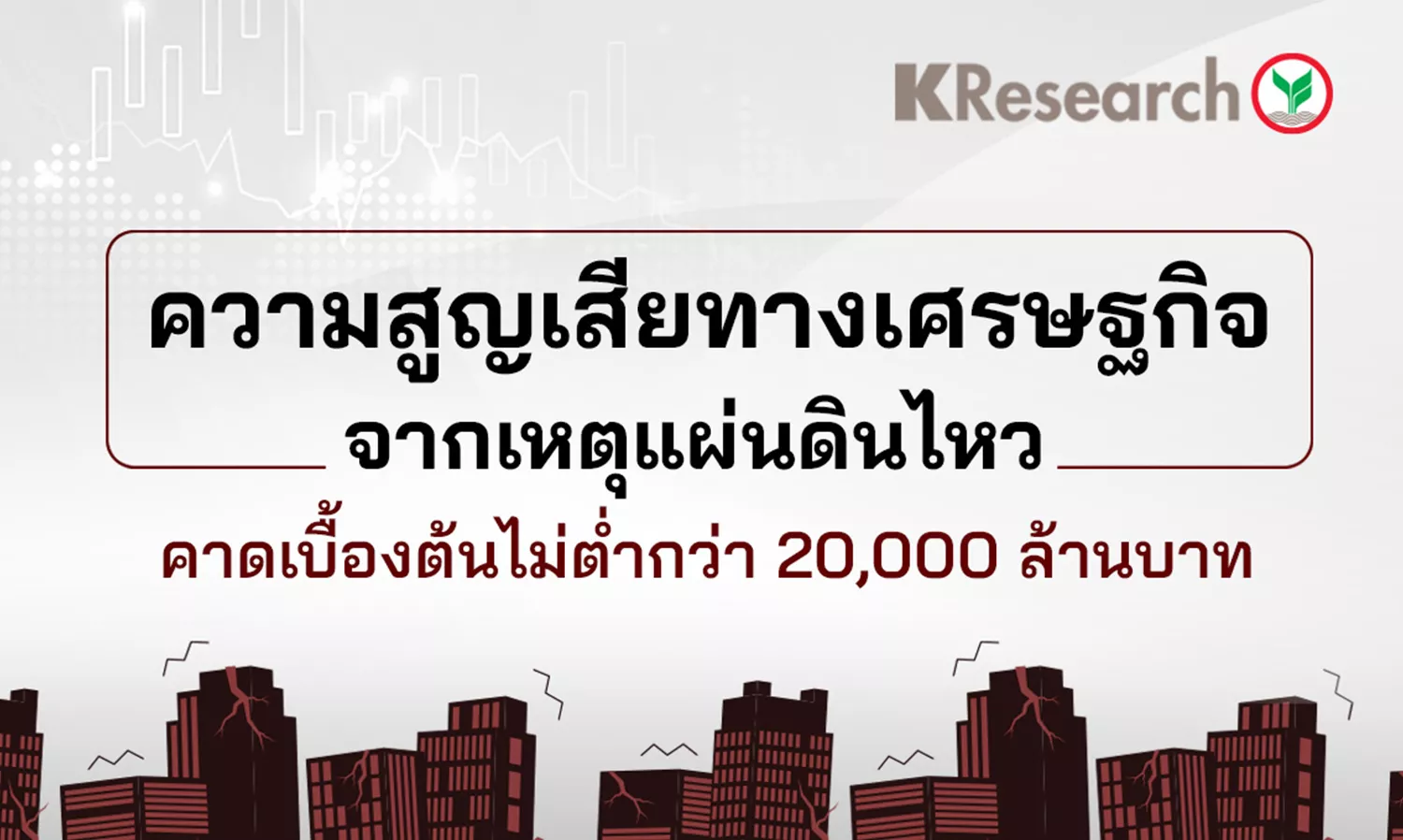

Economic Loss from Earthquake Estimated at No Less Than 20 Billion Baht

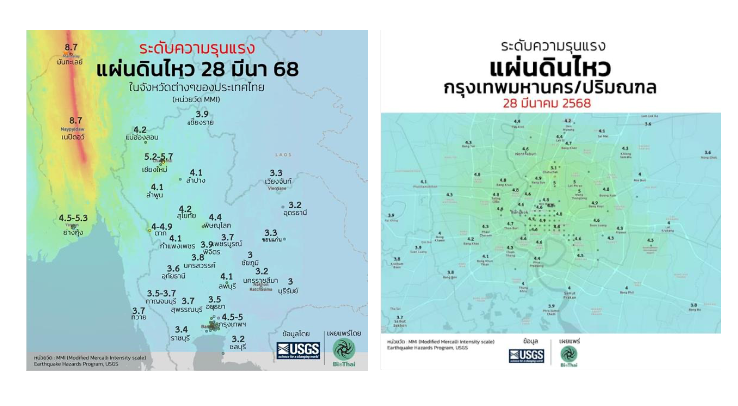

- On March 28, 2025, an earthquake measuring 8.2 on the Richter scale struck near the city of Sagaing, Myanmar, causing Thailand to experience severe tremors in several cities, particularly in Bangkok (intensity level 4.5-5.0 on the Modified Mercalli Intensity Scale – MMI) and Chiang Mai (5.2-5.7 MMI), resulting in immeasurable loss of life and property.

- Regarding the economic impact, Kasikorn Research Center estimates that the initial losses could amount to no less than 20 billion baht, primarily due to the disruption or postponement of economic activities, especially in the service sector in Bangkok and surrounding areas, as well as major cities like Chiang Mai. This includes events, restaurants, retail, transportation, etc. Additionally, purchasing power may decline as businesses and households will need to redirect cash flow/income to assess damages and repair buildings. If we also consider the damage to buildings, property, and the potential collapse/vibration of certain structures, along with repairs and insurance claims thereafter, the impact could be even greater.

- Impact on Businesses: We believe that while the repair and recovery from damages and the demand for temporary housing will benefit construction, building materials, and low-rise accommodations, the negative impact will likely affect sales and the transfer of condominium ownership in Bangkok, which may slow down for some projects. Additionally, the demand for rentals (rather than ownership) is expected to increase. According to REIC data, the accumulated number of condominiums for sale in Bangkok stands at over 65,000 units, valued at 375 billion baht.

- The international tourist market in Thailand is another group facing increased short-term risks due to confidence in travel and finding accommodation in affected areas. Most hotels in Bangkok are high-rise buildings. Although it is not peak season, there was already a downside as the main tourist markets for Thailand, such as China, Malaysia, and South Korea, began to decline in February and March. There is an increased risk that the estimated number of international tourists for the entire year 2025, projected at 37.5 million by Kasikorn Research Center, will be revised downward.

- Regarding assistance measures from financial institutions, they may help alleviate some impacts. However, the issue of fragile purchasing power and high debt will continue to pressure overall spending by households and businesses in the near future. Kasikorn Research Center views that the outlook for the remainder of this year poses increased negative risks to the Thai economy, key industries, as well as credit expansion and debt quality.

- The initial estimated impact on GDP from the earthquake is around -0.06%, which could lead to a downward adjustment of the Thai economic forecast for 2025, potentially below the previously anticipated 2.4%. However, Kasikorn Research Center is still awaiting the announcement of the U.S. import tax increase (Reciprocal tariff) on April 2. If Thailand is subjected to a 25% tax, it could further impact GDP by approximately -0.3%.

- Given the impact of the earthquake situation combined with trade war risks, Kasikorn Research Center assesses that the Monetary Policy Committee (MPC) is more likely to reduce the policy interest rate sooner than previously expected, which was anticipated in the second half of the year, to the upcoming meeting in April. The MPC may also reduce the policy interest rate at least once more during the remainder of 2025, amid a decreasing policy space.

- Regarding the impact on the financial sector, Kasikorn Research Center observes that:

- Insurance Business: Although those affected are currently assessing damages from the earthquake before filing claims, it is expected that the impact on the insurance business will be manageable since such events are rare in Thailand. Most Thai insurance companies have diversified risks through reinsurance abroad. Meanwhile, the risk-based capital (RBC) ratio of life and non-life insurance businesses is approximately three times higher than the minimum requirement.

While natural disasters may prompt customers to be more proactive in purchasing insurance, both in fire insurance and Industrial All Risks Insurance (IAR), insurance companies will need to manage the Loss Ratio, particularly in the fire insurance sector, which is expected to increase due to the frequency of natural disasters, and control risks from other more concerning and larger businesses, such as automobile insurance, accident, and health insurance.

-

- Commercial Banking: The recently announced financial assistance measures may have some immediate effects in stabilizing overall credit. However, overall credit remains pressured by purchasing power and economic uncertainty, leading to a projected growth of Thai bank credit this year at 0.6%.

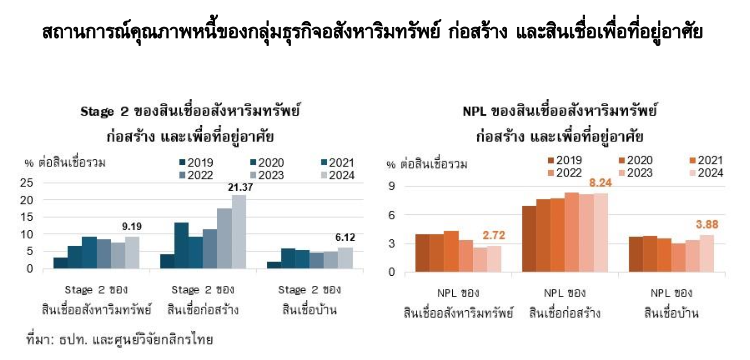

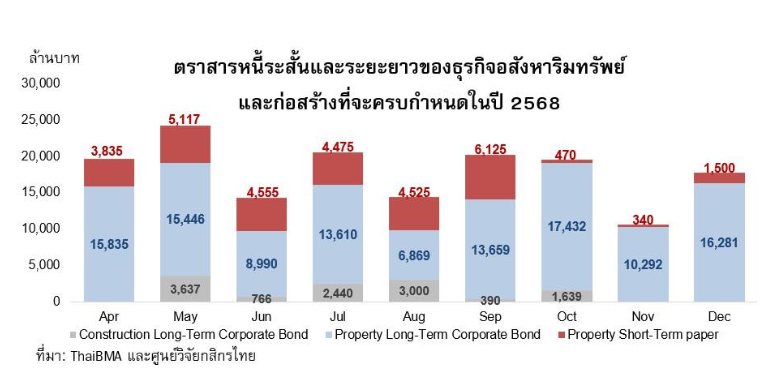

Key issues to monitor will include 1) Debt Quality, particularly in real estate, construction, and housing loans, which were already showing a declining trend post-COVID. Kasikorn Research Center previously estimated that the ratio of NPLs in the banking system could rise from 2.7% at the end of 2024 to the upper end of the range of 2.65-2.85% by the end of 2025. 2) The redemption of corporate bonds affected in the remainder of this year and 3) The impact of further interest rate cuts in the country if the Thai economy shows clearer signs of slowdown, which would further affect the net interest income of the Thai banking system.

[1] Data as of the end of 2024 for life insurance companies and as of Q3/2024 for non-life insurance companies.