Thailand's Real Estate Market Index (Residential Sector) Q4 2023

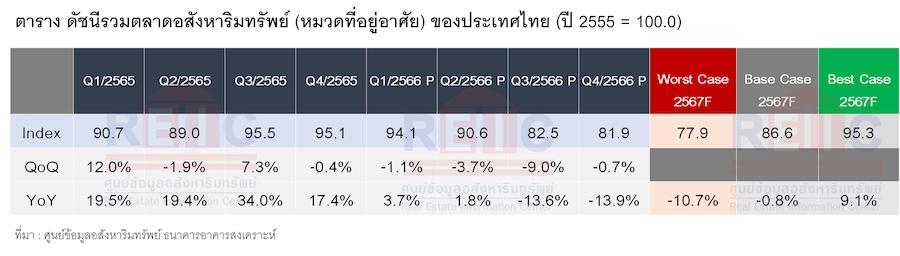

REIC reports that the overall index for Thailand's real estate market (residential sector) in Q4 2023 stands at 81.9, a decrease of -0.7% compared to the previous quarter (QoQ) and a -13.9% drop year-on-year (YoY). This decline is attributed to four main factors: the cancellation of LTV relaxation measures, high household debt levels, rising interest rates, and slow economic growth, which have reduced consumers' ability to purchase housing. For the entire year of 2023, the overall index for the real estate market (residential sector) is 87.3, down -4.8% from 2022 and slightly below expectations. In 2024, the index is expected to decrease slightly to 86.6, or about -0.8%, due to ongoing risk factors.

The Real Estate Information Center of the Government Housing Bank (REIC) reports that the composite index reflecting the overall residential market shows a value of 81.9, indicating a -0.7% decrease QoQ and a -13.9% decrease YoY, with declines in both demand and supply.

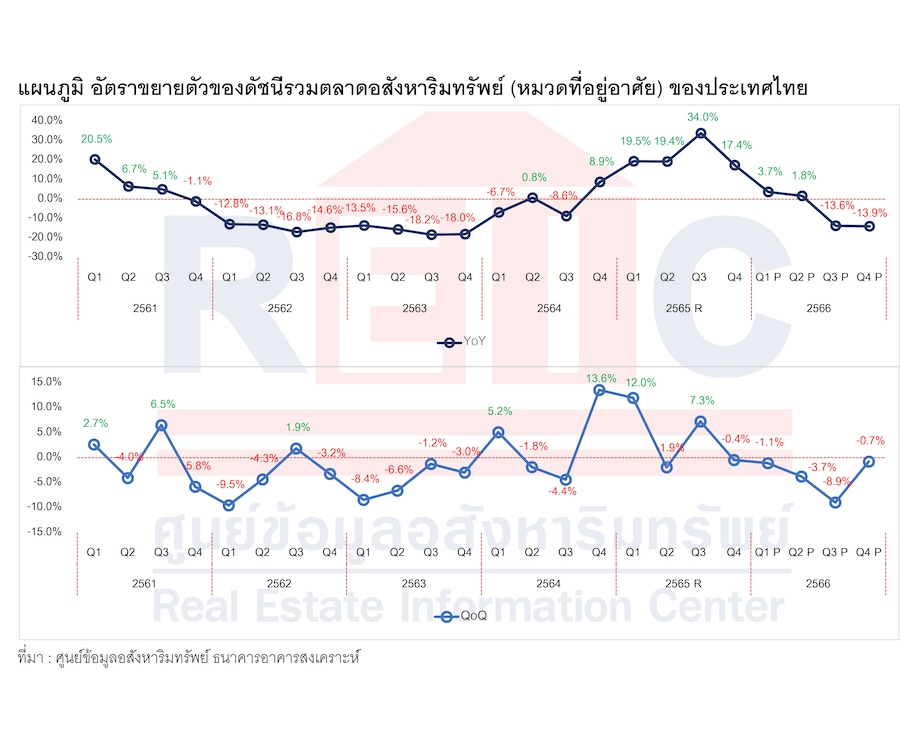

In terms of demand for housing, the transfer of ownership units decreased by -8.8% and value by -4.2%, while the absorption rate for new condominiums fell by -2.8% and for new single-family homes by -1.5%. On the supply side, the area permitted for residential construction decreased by -6.8%, and the confidence index for operators dropped by -4.0 points, particularly in investment, which fell by -10.8 points, sales by -6.8 points, performance by -6.5 points, employment by -5.9 points, and new project launches by -2.5 points.

This decline is due to several negative factors: (1) the cancellation of LTV relaxation measures by the Bank of Thailand, (2) high household debt levels exceeding 90% of GDP, (3) rising interest rates, which have increased five times in 2023, directly affecting purchasing power, and (4) the slow recovery of the Thai economy. These factors significantly limit the income growth of potential homebuyers while increasing their expenses, thereby reducing their purchasing and repayment capabilities, which directly impacts housing sales.

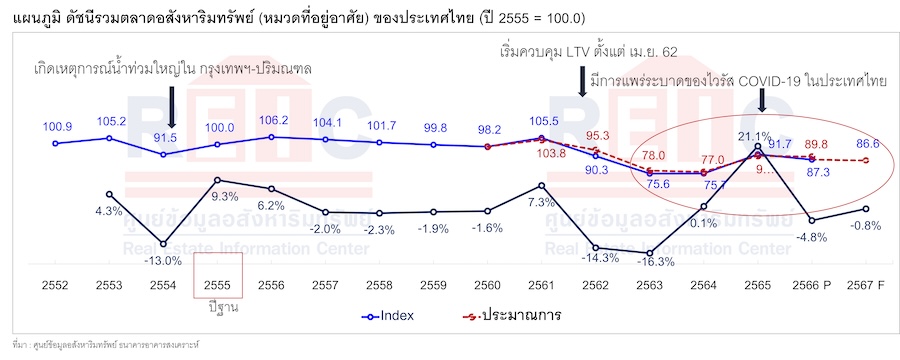

Dr. Vijai Wiratthakhan, Inspector of the Government Housing Bank and Acting Director of the Real Estate Information Center, stated that for the entire year of 2023, the overall index for Thailand's real estate market (residential sector) is 87.3, down -4.8% from 2022 and slightly below the REIC's forecast of 89.8, affected by the overall economic growth of only 1.9% in 2023, a slowdown from 2.5% in 2022.

The outlook for the overall index of Thailand's real estate market (residential sector) in 2024 is expected to face several risk factors, including (1) potential economic slowdown due to global economic conditions, (2)

the cancellation of LTV relaxation measures, (3) rising living costs, and high household debt levels exceeding 90% of GDP. These factors significantly affect purchasing power and access to credit, as financial institutions continue to apply strict lending criteria similar to the previous year, potentially becoming even stricter.

REIC anticipates that the overall index for the real estate market (residential sector) in 2024 will slightly decline from 2023, projected at 86.6, or a decrease of approximately -0.8% in the base case. This decline is expected due to factors in the operator confidence index, particularly in sales and performance, as concerns about the slowing economy persist. Demand for property transfers and supply of permitted construction areas may improve slightly compared to 2023, but the supply of completed and registered housing may slow down due to the existing surplus in the market and the sluggish economic conditions.

However, if these factors yield better outcomes for the real estate market than anticipated in the base case, the index could rise to 95.3, reflecting a growth of 9.1% (Best Case). Conversely, if these factors turn out to be more negative than expected in the base case scenario, the index could drop to 77.9, a decrease of up to -10.7% (Worst Case) (see Table 1 and Chart 3).

“Considering the changes in the index, it is evident that after encountering the COVID-19 pandemic, the real estate market hit its lowest point in Q3 2021 and has been recovering continuously since Q1 2023 until Q1 2024. However, the cancellation of LTV relaxation measures, coupled with significantly rising interest rates and worsening household debt, along with a clearly slowing economy, are crucial factors affecting the Thai real estate market, leading to a continuous downward trend in each quarter (QoQ), especially in Q3 and Q4 2023, which saw significant declines. It is expected that the real estate market in Q1 2024, lacking new positive factors, will remain sluggish, with all sectors hoping to see new positive developments in Q2 or by Q3 2024 to drive overall growth from 2024,” Dr. Vijai concluded.

----------------------------------------------------------------

Data Compilation Method

The Real Estate Information Center of the Government Housing Bank has developed the “Composite Index for Thailand's Real Estate Market (Residential Sector)” using a quantitative index method (Quantity index) based on the geometric mean of average data and employing multiple linear regression analysis for forecasting.

Data from both demand and supply sides in the Bangkok Metropolitan Region are used, consisting of the following variables:

- There are 6 independent variables:

- Transfer of ownership data, which is a demand-side variable.

- Absorption rate for housing projects, which is a demand-side variable.

- Absorption rate for condominiums, which is a demand-side variable.

- Data on completed and registered housing, which is a supply-side variable.

- Area permitted for residential construction, which is a supply-side variable.

- Operator confidence index, which is a variable for both supply and demand.

- There is 1 dependent variable, which is the “Composite Index for the Real Estate Market (Residential Sector)” that has been developed.

The Composite Index for Thailand's Real Estate Market (Residential Sector) is developed quarterly, starting from Q4 2021, using data from both demand and supply sides from 2009 to 2017 to develop the index, using the index from 2012 as the base year.

Disclaimer

The statistical data and any writings in this report are sourced from reliable sources or processed from credible data. The Real Estate Information Center has verified this information to a certain extent but cannot guarantee its accuracy or truthfulness and cannot be held liable for any damages arising from the use of this information. Users should exercise discretion and verify as appropriate.