Exploring the Direction of Private Hospital Business in 2022: Continuous Revenue Growth in Response to Positive Signals from Country Reopening, with Optimism for 2023

- The private hospital business is expected to show clear recovery in 2022 and remains a sector with long-term growth potential. Overall revenue for private hospitals in 2022 is projected to grow by 42.5% YoY, continuing from 2021, driven by temporary factors from treating COVID-19 patients and an improving demand for non-COVID-19 treatments, along with the reopening of the country which is gradually reviving revenue from international patients.

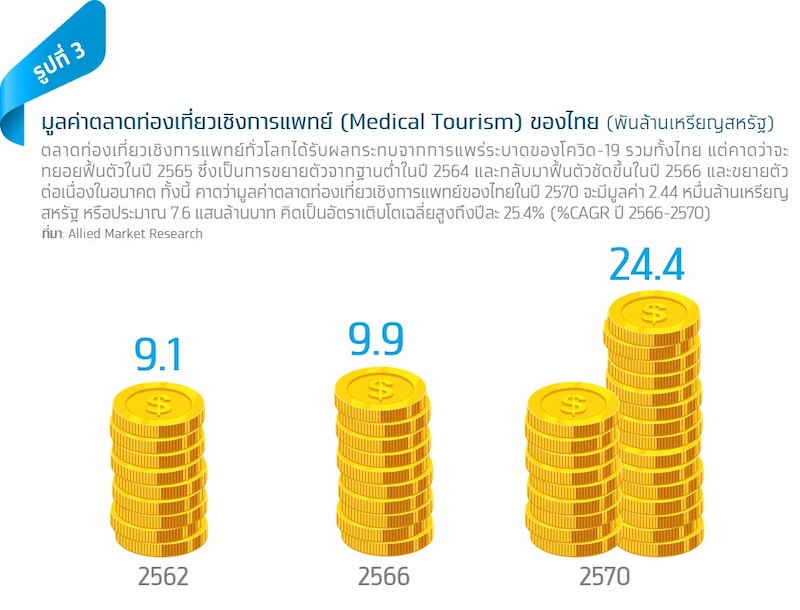

- In 2023, international travel is expected to normalize, supporting the Medical Tourism trend, which is anticipated to lead to a continued revenue growth of 19.8% YoY for private hospitals.

- In the future, Health Tech could become a significant competitor worth watching. Therefore, adjusting business models by collaborating with partners across various sectors will help create opportunities to expand medical services.

By: Sujitra Anno, Krungthai COMPASS

The overall revenue of private hospitals in 2022 is expected to continue growing from 2021, benefiting from temporary factors related to treating COVID-19 patients and an improving demand for non-COVID-19 treatments, along with the reopening of the country which is gradually reviving revenue from international patients.

The overall revenue of private hospitals in 2022 has the potential to grow by 42.5% YoY, with the main customer base being Thai patients. It is expected that in 2023, the business will continue to grow by 19.8% YoY, supported by a clearer recovery in Medical Tourism.

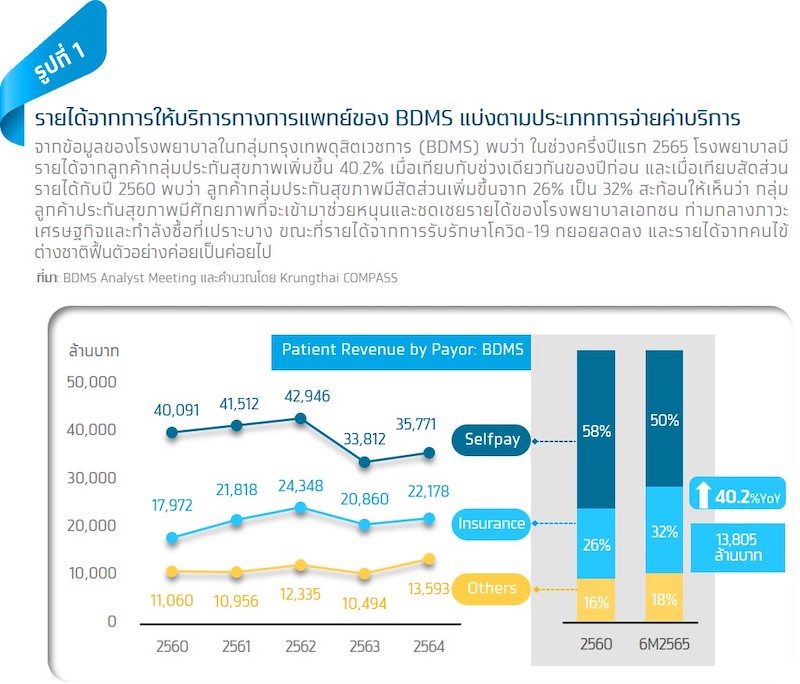

Business Overview: In 2022, the business is expected to continue growing by 42.5% YoY after recovering by 32.3% YoY in 2021, benefiting from temporary factors related to treating COVID-19 patients and an improving demand for non-COVID-19 treatments. The main customer base in 2022 remains Thai patients, with health insurance customers showing potential to support private hospital revenues. Additionally, the easing of travel restrictions since late 2021 and the reopening of the country in the second half of 2022 positively impacts revenues for private hospitals with a high proportion of international patients, such as Bumrungrad Hospital (BH), Samitivej Hospital (SVH), and Bangkok Dusit Medical Services (BDMS). Krungthai COMPASS estimates that the number of international tourists visiting Thailand in 2022 will be around 8.9 million, an increase from earlier estimates, with a significant portion expected to seek medical services in Thailand, positively impacting the business.

For 2023, it is expected that the international travel situation will normalize, making travel more convenient, leading to a continued revenue growth of 19.8% YoY for private hospitals, supported by a clearer recovery in Medical Tourism, particularly from international patients from ASEAN, China, Russia, Japan, and the Middle East, who will return to use private hospital services in Thailand due to confidence in treatment quality, affordable medical costs, and good standards and services. Thailand has 59 hospitals accredited by JCI, and the existing infrastructure continues to support the increasing demand for medical services due to a higher number of patients and rising illness rates, driven by lifestyle risks, an aging society, and the increasing spread of various diseases.

Health insurance customers remain a key target supporting private hospital revenues amid Thailand's fragile economy and pressures from inflation and rising living costs.

According to data from Fitch Solutions on the payment structure for private hospital patients, self-paying patients make up the largest proportion, followed by health insurance customers, which aligns with data from BDMS hospitals that hold the largest market share.

Thus, amid Thailand's fragile economic situation, where purchasing power faces pressures from inflation and rising living costs, health insurance customers represent a potential group that can help support private hospital revenues after the temporary factors from treating COVID-19 patients and income from alternative vaccines gradually diminish. Expanding this customer base requires strategic planning and collaboration with insurance companies to design policies and enhance privileges for using services at specific private hospitals.

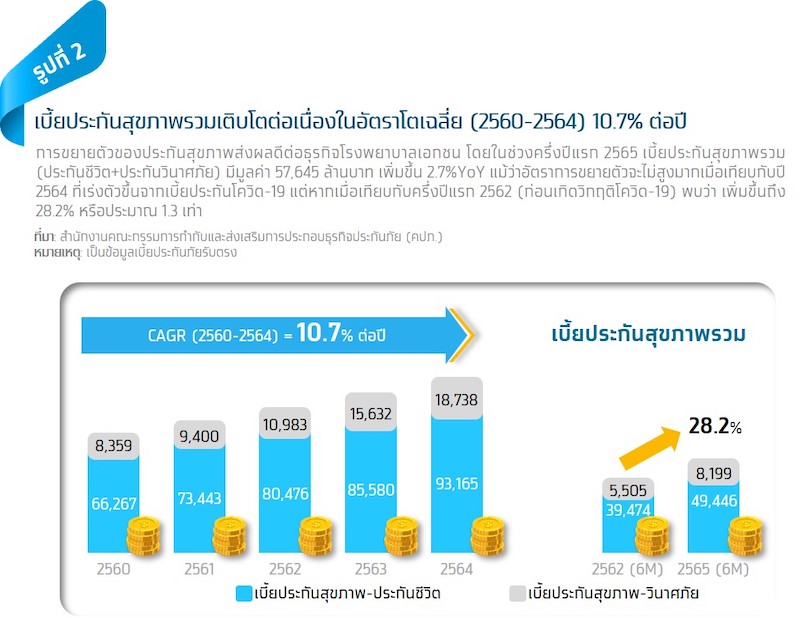

Thai people are increasingly concerned about health and interested in purchasing health insurance to mitigate risks, positively impacting the private hospital business.

The COVID-19 pandemic has heightened awareness among Thai people regarding health care, disease prevention, and treatment, as well as concerns about rising medical costs, leading to increased recognition of the importance of purchasing health insurance to reduce the risk of bearing future medical expenses, along with a desire for convenience in using private hospital services, especially among middle-income customers. This aligns with a TDRI study estimating public health expenditure in the next 15 years, which found that the rate of using universal health insurance inversely correlates with income; as income increases, the usage rate decreases, and people are willing to pay more to go to private hospitals or purchase health insurance for greater convenience.

When comparing total health insurance premiums between the first half of 2019 (before the COVID-19 crisis) and the first half of 2022, the first half of 2022 saw total health insurance premiums 1.3 times higher than in the first half of 2019. However, Krungthai COMPASS believes there is still room for growth in health insurance, as total health insurance premiums per capita remain relatively low, estimated at 1,691 baht per person in 2021.

The cancellation of the Thailand Pass is boosting the gradual recovery of Medical Tourism.

Before the COVID-19 crisis, medical tourism customers were a significant source of revenue for private hospitals. However, the crisis caused this revenue stream to shrink due to international travel restrictions. Nevertheless, the government eased travel measures since late 2021 and fully reopened the country in the second half of 2022. The cancellation of the Thailand Pass has allowed private hospitals that rely heavily on international patient revenue to expand again, leading to a gradual recovery in medical tourism in 2022, with clearer recovery expected in 2023. Key supporting factors include 59 hospitals in Thailand accredited by international standards (JCI), relatively low medical costs compared to regional competitors, and high standards and services, along with a reputation for specialized medical treatments such as infertility, anti-aging medicine, and gender reassignment surgery. Additionally, the cost of living in Thailand remains low, making it suitable for long-term medical care and recovery.

According to data from Bangkok Dusit Medical Services (BDMS), revenue from international patients has increased and has been growing significantly since Q1 2022. Therefore, the reopening of the country is expected to further promote the gradual recovery of the Medical Tourism market.

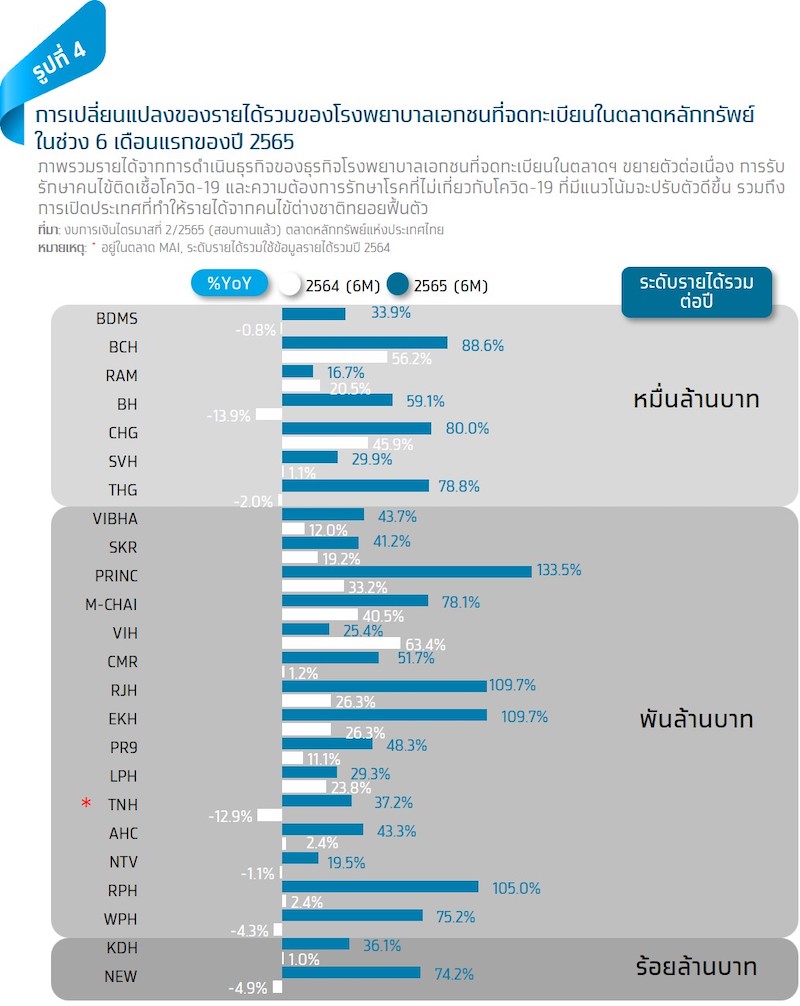

In the first half of 2022, the revenue and net profit of 24 registered private hospitals in the market continued to grow compared to the same period last year, with total revenue of 125.499 billion baht, growing by 48.9% YoY, and net profit of 24.226 billion baht, increasing by 173.8% YoY. The main customer base remains Thai patients, benefiting from the easing of travel restrictions since late 2021, positively impacting revenues for private hospitals with a high proportion of international patients, such as Bumrungrad Hospital, Samitivej Hospital, and BDMS.

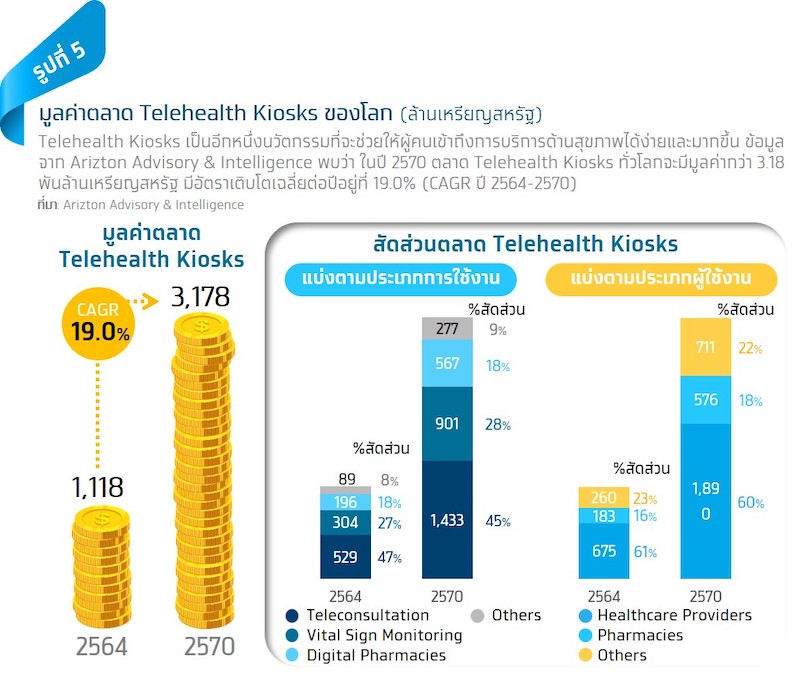

Will Telemedicine or Telehealth transition from being an assistant to becoming a competitor for private hospitals?

It is undeniable that after the COVID-19 crisis, health technology, or Health Tech, has played a more prominent role in healthcare and medical treatment, particularly telemedicine, commonly known as Telehealth. Initially, it was used to enhance the medical service capabilities of hospitals, but in the future, telemedicine may be offered in the form of Telehealth Kiosks in shopping malls, government centers, or through collaborations between Health Tech operators and mobile carriers, clinics, and pharmacies, making health services more accessible and convenient for the public. While it may not completely replace hospitals, it is certainly a competitor worth watching.

Globally, the market value of Telehealth Kiosks is expected to increase. According to a survey by Arizton Advisory & Intelligence, the global market value of Telemedicine is projected to reach $3.18 billion by 2027, up from $1.12 billion in 2021, growing at an average rate of 19.0% per year.

Implication:

- Krungthai COMPASS views the private hospital business as having strong growth potential after facing a crisis that impacted revenues. As the global COVID-19 pandemic subsides, it is estimated that the business will continue to grow in the long term, supported by strong factors such as increasing demand for medical treatment due to a rising number of patients and higher illness rates from lifestyle changes, an aging society, and the spread of various diseases. The recovery of the medical tourism market, where Thailand is renowned for its high-quality treatment, combined with relatively low medical costs compared to regional competitors, is also a significant factor. The COVID-19 crisis serves as an important lesson for operators in all businesses, including private hospitals, to prepare for unexpected revenue-impacting situations. Therefore, strategic planning to expand the domestic customer base is essential, particularly targeting health insurance customers who represent a potential group that can help reduce reliance on any one customer type, especially international patients, by collaborating with insurance companies to design health insurance products that meet diverse consumer needs.

While the private hospital business has growth potential, there are factors to consider:

- Health Tech or Digital Health may become significant competitors, both directly and indirectly, to watch. The advancement of technology, combined with people's familiarity with using technology, will lead to continuous innovations in health. As Health Tech plays a larger role, making basic healthcare and treatment easier, it could lead to long-term public health benefits that help reduce congestion in public hospitals and improve access to healthcare services, which may decrease the demand for private hospitals with higher costs. However, private hospitals can leverage Health Tech to enhance their medical service capabilities, reduce service costs, and focus on using internationally recognized modern medical technologies for complex disease treatments, such as precision medicine and regenerative medicine, which emphasize cell or gene therapy, along with promoting specialized expertise among doctors, ultimately creating credibility and long-term revenue growth for hospitals.