Finding Answers: Do You Have to Wait Until You Graduate to Apply for a Home Loan?

The world has become more open, allowing the younger generation to reach the finish line of success more quickly. Young people today have opportunities to build wealth for themselves from a young age. Some start their own businesses in their early twenties, and even while still in university, they take on side jobs as online sellers, generating significant income.

As young people can achieve financial stability while still studying, it’s not surprising that they consider pursuing their dreams by applying for a home loan for their families or buying a condominium for convenience. Some may view this as a long-term investment to help them reach their goals faster. The sooner they are ready, the closer their once-distant goals may become.

The question is: If you want to apply for a home loan, do you have to wait until you graduate? Let's find out together!

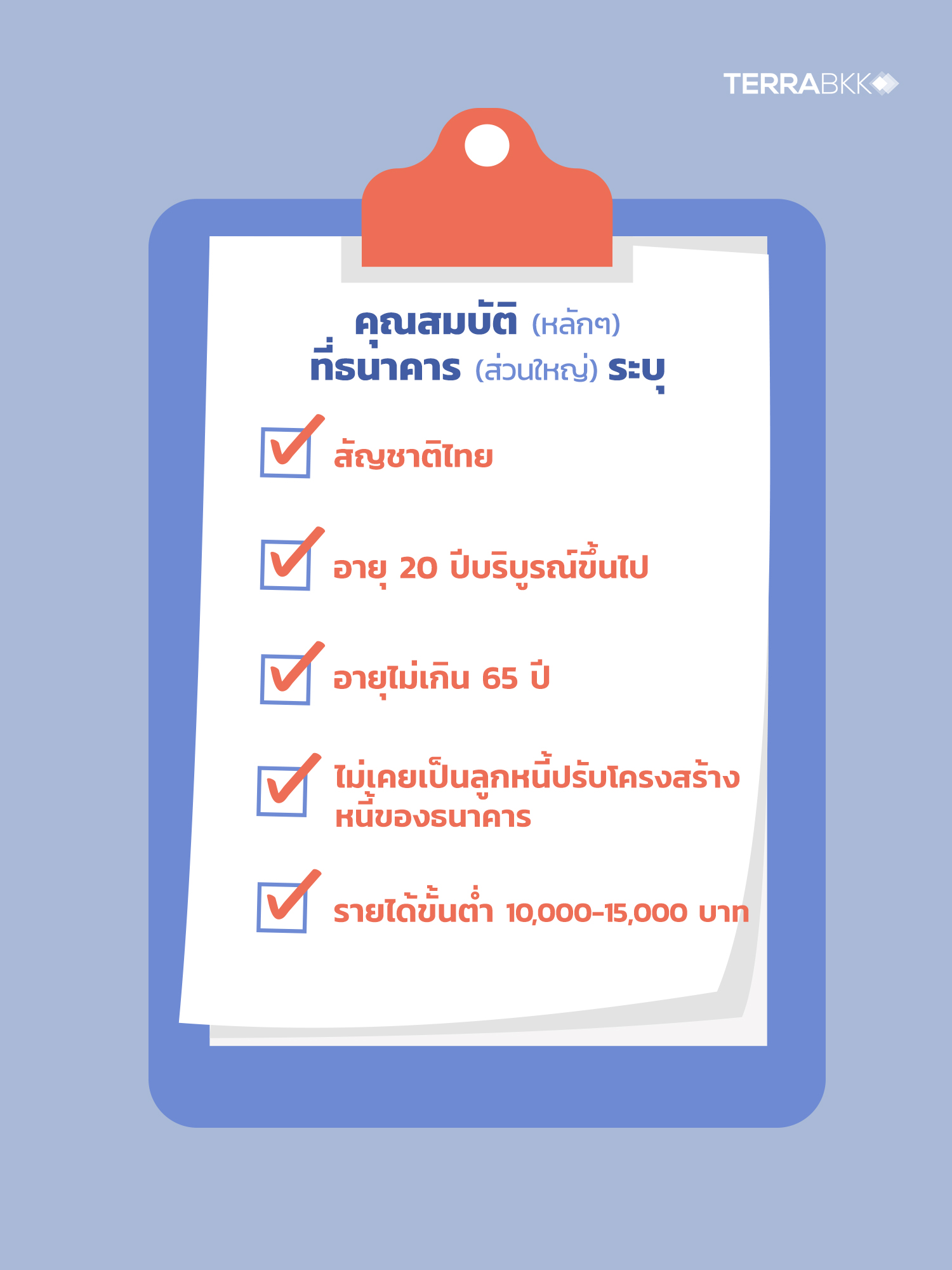

First, let’s look at the qualifications required to apply for a housing loan. Banks typically consider several criteria. The main qualifications that most banks specify are that the applicant must be a Thai national, at least 20 years old and not older than 65, and must not have ever been a debtor undergoing debt restructuring with the bank, with a minimum income of 10,000-15,000 baht.

This means that if you meet the age requirement but are still in university, it’s not a problem as long as you meet another basic condition: having a minimum income of 10,000-15,000 baht. In the past, many might have thought this was difficult because students, even if they had part-time jobs, often earned just enough for pocket money and not substantial income.

However, as mentioned earlier, the world has changed. Technology not only shrinks the world but also breaks down barriers that used to be obstacles, allowing the younger generation to think boldly and pursue their dreams. Many start businesses in their early twenties, and if they are on the right track and generate consistent income, they can apply for a housing loan without letting their student status limit them.

Now, if you apply for a loan, will you get the amount you want to buy a house? Banks will consider your repayment ability, similar to how they assess loan amounts for salaried individuals. However, the documents required for applying for a housing loan may differ.

Typically, for salaried individuals seeking a housing loan, they must have at least 2 years of work experience and be employed in their current position. The main documents required, in addition to personal documents, include:

1. Salary certificate or salary certificate using the agency's benefits

2. Payslips for the past 6 months or bank statements for the past 6 months

However, if you are a business owner, freelancer, or online seller, you may need additional documents to demonstrate your income status. For example, those who excel in online selling may need to provide evidence showing clear online sales channels, such as which platforms they sell on, whether on marketplaces like Lazada, Shopee, or social media like Facebook, Instagram, or Line.

Additionally, to enhance credibility, you may need documents showing financial capability, such as invoices and receipts to show where your income comes from, along with shipping documents to confirm that your store has orders and income.

One essential document is a bank statement, which can be an advantage for online sellers today. In a cashless society, having a clear income channel to present to banks increases credibility and the chances of loan approval.

At this point, many may wonder which banks are willing to open opportunities and options for applying for home loans.

The answer is that several banks have designed loans to cater to freelancers, online sellers, and those looking to build a foundation for their lives from a young age. Each bank may have different conditions or requirements.

For example, Krungsri Bank's housing loan requires borrowers to have been in business for at least 2 years, while SCB's new home loan requires self-employed borrowers to provide bank statements for the past 6 months. Meanwhile, the Government Housing Bank's housing loan requires borrowers to have a savings account with the bank and provide evidence of their online selling business and income.

For those who assess and find that they do not yet meet the qualifications or have the required income documentation, don’t lose hope. If applying alone is challenging, consider seeking assistance.

For instance, the Two Gen home loan program from the Government Housing Bank allows families with children aged 18 and older to co-borrow with parents under 55 who have no existing home loan obligations. The borrower must also have no educational loan obligations, such as from the Student Loan Fund, to apply for a home loan of up to 2 million baht. Notably, if a child co-borrows, the repayment period can be extended from 40 years to a maximum of 70 years.

At this point, you may be wondering whether students can apply for housing loans. If you ask why one should be eager to apply for a housing loan even before entering the workforce,

it’s clear that not only does it help them reach their goals and create stability faster, but importantly, at a young age, many may have fewer debts or expenses, not yet have family obligations, or children to support.

Therefore, if they have financial stability that the bank assesses as qualifying, they have a good chance of getting loan approval without worrying about the repayment period, as they can choose a term of up to 30 years.