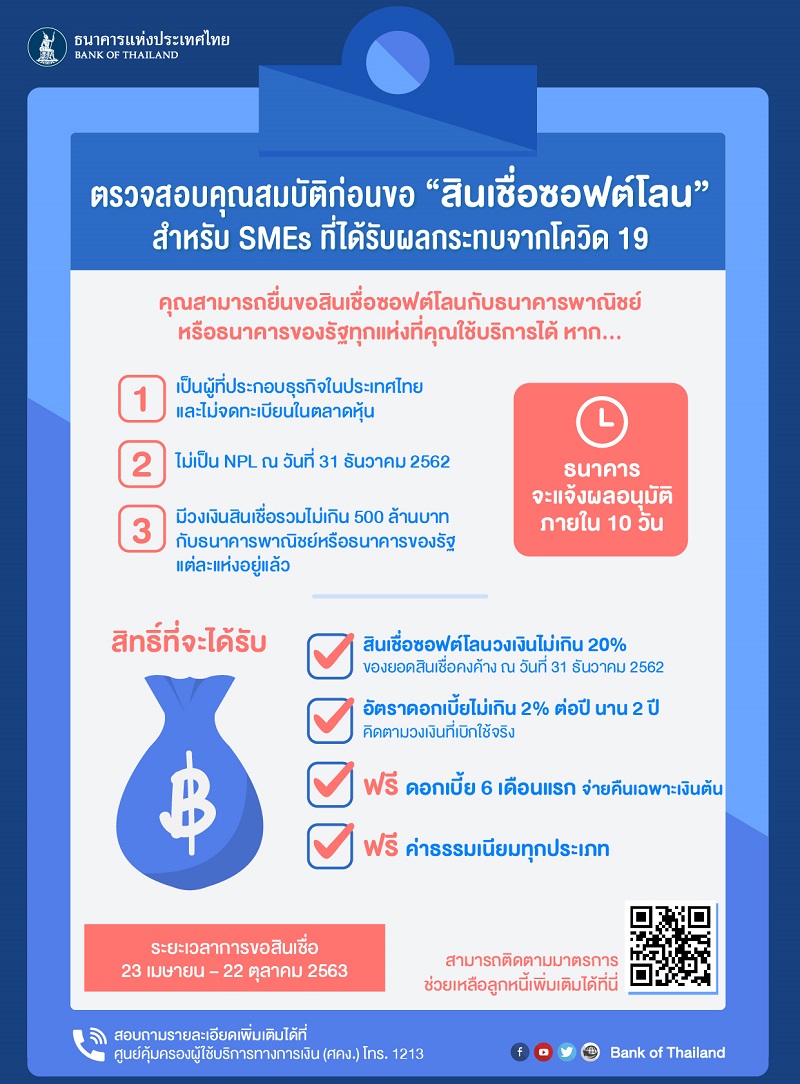

Clarifying Soft Loan Conditions from the Bank of Thailand

The low-interest loan (soft loan) measures from the Bank of Thailand are another initiative to assist SMEs with a credit limit of up to 500 million baht (for each financial institution) that have been affected by the COVID-19 pandemic, allowing them to access low-interest loans, which is a measure to help increase liquidity for businesses in this situation.

Many entrepreneurs may still have questions regarding the conditions and uncertainties surrounding this measure when applying for soft loans. Therefore, the Bank of Thailand has summarized 10 frequently asked questions regarding the low-interest loan measures for everyone.

1. What qualifications must SMEs have to apply for assistance?

Answer: SMEs applying for assistance must meet the following qualifications:

1. Be an individual with a business establishment operating in Thailand.

2. Not be a company listed on the Stock Exchange of Thailand.

3. Not be classified as an NPL by financial institutions as of December 31, 2019, as the focus is on supporting those with potential affected by COVID-19.

4. Not be engaged in financial business.

5. The original credit limit must not exceed 500 million baht, and new loans can be requested for no more than 20% of the outstanding credit with the financial institution.

2. Do SMEs applying for a soft loan have to pay any fees?

Answer: There are no fees for applying for a soft loan from the Bank of Thailand.

3. Can SMEs apply for a soft loan exceeding 20% of their existing debt?

Answer: SMEs can only apply for a soft loan up to 20% of the outstanding credit as of December 31, 2019. If they wish to borrow more, each financial institution will consider it based on the entrepreneur's capacity and may set different conditions, such as an interest rate higher than 2% for the additional amount provided by the financial institution, which is not related to the soft loan.

4. Is it true that financial institutions have reported that the soft loan is no longer available?

Answer: This is not true; the soft loan from the Bank of Thailand is still available.

There is a total fund of 500 billion baht, and applications for loans opened on April 27, 2020. However, there may be confusion with the soft loan from the Government Savings Bank, which may have reached its full limit.

5. Can SMEs that are not existing debtors of financial institutions apply for the Bank of Thailand's soft loan?

Answer: No, because the Bank of Thailand's soft loan is limited to existing debtors of financial institutions.

This is to expedite the assessment of qualifications for debtors needing urgent assistance and to manage the risk of bad debts for financial institutions.

New SMEs can contact state-owned banks for loans, which have different details from the Bank of Thailand's soft loan.

6. Do SMEs applying for the Bank of Thailand's soft loan need to purchase various types of insurance to qualify for this loan?

Answer: This is not true; purchasing various types of insurance is at the debtor's discretion.

It does not affect the application for a soft loan. However, financial institutions may charge for life insurance premiums for loan protection based on actual costs, but they cannot force life insurance and cannot set it as a condition for loan approval.

7. If I have applied for a soft loan from the Government Savings Bank, can I apply for one from the Bank of Thailand as well?

Answer: Yes, but the bank may consider providing assistance under this measure to debtors who have not previously received similar assistance to distribute support to SMEs affected more broadly.

8. Does the credit limit for businesses under this measure include loans secured by residential properties?

Answer: Yes, if the debtor informs the financial institution from the outset that it is a business loan.

However, loans for residential purposes do not qualify for the Bank of Thailand's soft loan. The loans counted for applying for the Bank of Thailand's soft loan will only include the outstanding business loans of each financial institution.

Except for personal loans under supervision, small loans for business under supervision, and credit card limits.

9. If I have loans with multiple banks but am classified as NPL with some banks, can I apply for the Bank of Thailand's soft loan?

Answer: You can contact the financial institution where you still have a normal debtor status.

10. How can I inquire for more information or report problems when applying for the Bank of Thailand's soft loan?

Answer: You can contact the Call Center of that financial institution. If you encounter fraud or issues when applying for the soft loan, you can report it to the Financial Consumer Protection Center at the Bank of Thailand by calling 1213.

Thank you for the information from: Bank of Thailand