Are You Financially Prepared Today?

In the current COVID-19 situation, many of us are facing various problems around us, including financial issues. Many people are struggling with cash shortages and insufficient funds due to job losses or being laid off, while daily expenses continue to exist, along with other burdens such as home loans, car loans, tuition fees, etc. This raises a significant question: Are we all financially prepared today, especially in terms of having funds to support emergencies or unexpected situations?

In emergencies or unusual events, the most useful assets are those that are liquid or can be quickly converted into cash, such as cash, bank deposits, and certain financial assets that can be traded daily. These can quickly resolve financial problems in emergencies. On the other hand, low liquidity assets are those that take a long time to sell or convert into cash, such as real estate or collectibles, which may not effectively address financial issues during emergencies. Comparing this to the current situation clearly shows that the most essential thing for everyone right now is to hold cash or have savings and deposits, as these assets align with the current circumstances. Even gold, another popular asset, cannot be sold quickly despite its rising prices, as some buyers cannot afford the high prices.

How is the savings situation for Thai people?

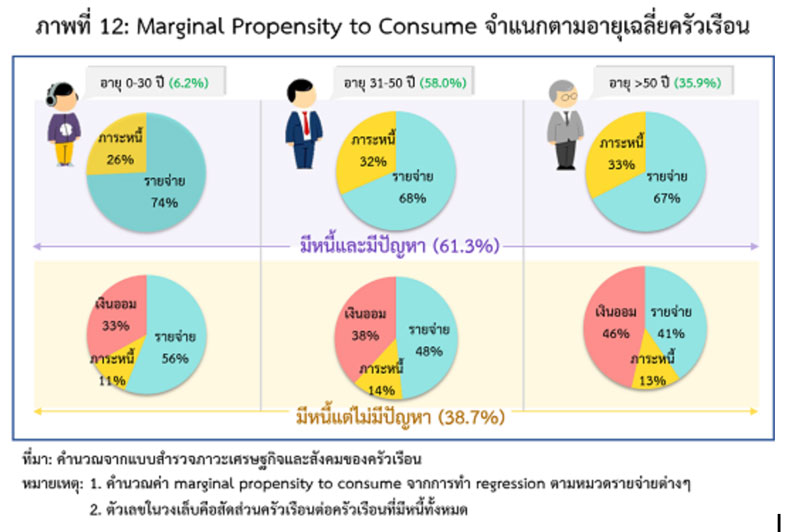

According to a survey by the Bank of Thailand in 2017, over 61.3% of Thais have no savings, indicating they are in debt and struggling with financial management. Meanwhile, 38.7% have savings, are in debt, but do not face financial management issues. This highlights that over 61.3% of Thais are not financially prepared for emergencies.

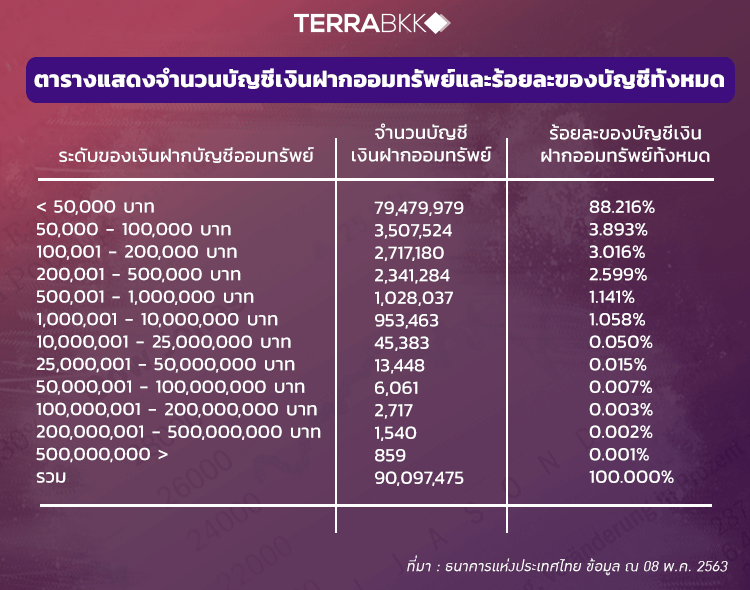

Additionally, the Bank of Thailand provided further information that in March 2020, there were a total of 101 million deposit accounts across all banks in Thailand, with a total deposit value of over 14.13 trillion baht, of which more than 90 million were savings accounts. However, upon examining the details of these savings accounts, it is evident that over 79 million accounts, or about 88%, have deposits of less than 50,000 baht. This further emphasizes the lack of preparedness among the majority of the population to handle financial issues in emergencies.

If we reflect on what constitutes an "emergency," it can be likened to the current COVID-19 situation that everyone is experiencing. In a time when salaried jobs were considered secure, many have been unexpectedly laid off as businesses could not continue operations. We see news daily about businesses closing, hotels losing money, and airlines canceling flights, which indicates a chain reaction affecting various professions.

If you are one of those facing these issues directly, how many months do you think you can sustain your living expenses without a job?

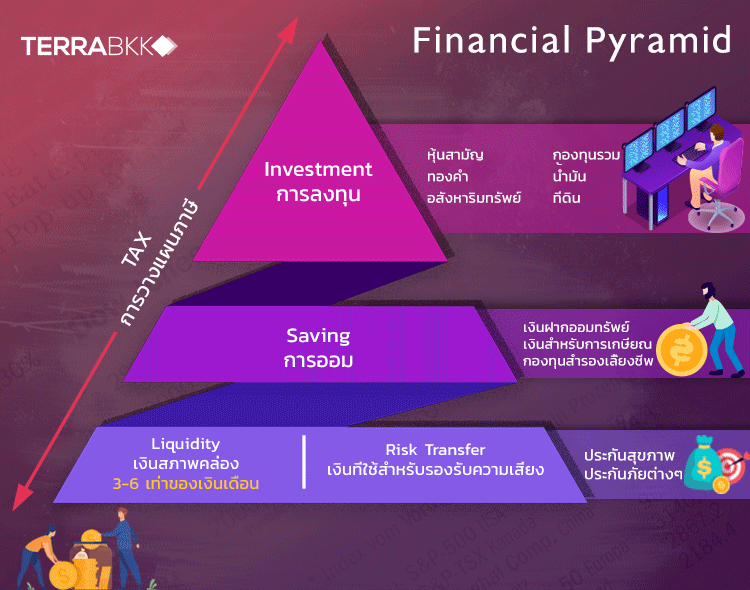

First, let's understand the principles of international financial planning and what the standard for real savings should be. Many people still misunderstand the concept of saving money. We will use the Financial Pyramid principle to illustrate this.

The Financial Pyramid compares saving and planning in a pyramid format to reflect the foundational layers leading to the ultimate goal of financial planning.

Part 1: The base of the pyramid consists of two components: Liquidity (emergency funds) and Risk Transfer (funds for risk management).

Liquidity (emergency funds) is the most crucial amount of money that many people often overlook, assuming that "an emergency is unlikely to happen." Liquidity serves to cover expenses when income stops but daily expenses continue. Having money set aside to sustain life without liquidity issues is essential.

How much should you save to be sufficient?

This should be divided into two criteria: one for salaried employees and one for freelancers.

Criteria for salaried employees:

Typically, salaried employees have a stable monthly income, giving them an advantage in managing their income and savings. It is generally recommended to have emergency savings of about 3-6 months.

For example, if a salaried employee earns 20,000 baht and spends 70% of their salary, their monthly expenses would be 14,000 baht. Therefore, they should have emergency savings of approximately 42,000-84,000 baht.

Criteria for freelancers:

Freelancers often have unstable monthly incomes, making it harder to manage income and savings compared to salaried employees. Therefore, freelancers should aim for emergency savings of about 6 months to 1 year.

For example, if a freelancer earns 20,000 baht and spends 70% of their income, their monthly expenses would be 14,000 baht. Thus, they should have emergency savings of approximately 84,000-168,000 baht.

Risk Transfer (funds for risk management) refers to creating necessary funds that we may not have from the start. A simple way to transfer risk is through insurance, as it provides funds to handle unexpected problems. Funds for risk management protect our larger savings from unforeseen events.

Part 2: Saving involves saving or investing in low-risk options for significant life goals or to meet life needs, such as retirement savings, children's education, buying a house, getting married, etc.

Part 3: Investment occurs when we have funds to cover all life events. The remaining funds are used for investment to continuously build financial wealth. However, investments must be studied and understood well, as all investments carry risks.

Finally, at every stage of the financial pyramid, we should also learn about tax management to reduce tax liabilities in our planning, as reducing taxes equates to increased income and savings.

However, in the current situation where people are affected across all sectors, Terrabkk predicts that most people prioritize investment over saving, both in terms of liquidity (emergency funds) and risk transfer (funds for risk management). This has led to liquidity problems during emergencies, as most assets are tied up in investments, making it impossible to convert them into cash quickly when truly needed.