Clearing Up the LTV Measures: How Do They Benefit the Thai Economy in Real Estate?

Currently, a major issue affecting the real estate sector that cannot be overlooked is the LTV measures from the government, which aim to regulate home loans. The key point is the control of borrowing for a second property. For residential properties priced at 10 million baht or more, or for purchasing a second home, a minimum down payment of 20% of the collateral value is required. Previously, for properties priced below 10 million baht, a down payment of at least 5-10% was sufficient, and these measures have been in effect since April 1, 2019.

The aftermath of these measures has seen a 15% decline in overall bookings in both low-rise and high-rise real estate markets, raising questions about whether this downturn is a direct result of the new regulations. What is the true purpose of these measures? Are they beneficial?

Recognizing the significance of changes in financial policy (LTV), which impacts real estate businesses and consumers looking to purchase homes, Terra Media and Consulting Co., Ltd. (TerraBKK) organized a seminar titled LTV and the Thai Economy, supported by the Thai Real Estate Association and the Department of Housing, Faculty of Architecture, Chulalongkorn University. This event provided a platform for stakeholders to present ideas and seek solutions for the real estate sector.

The seminar covered a range of topics, starting from an overview of the Thai economic situation, the home-buying behavior of Thais in the 4.0 era, to the principles, reasons, and solutions regarding LTV measures aimed at stimulating purchasing power and boosting the economy. TerraBKK has summarized key points from the seminar here.

Video Overview of the Seminar on LTV and the Thai Economy

Assoc. Prof. Trairat Jarutatharn, a lecturer at the Department of Housing, Faculty of Architecture, Chulalongkorn University, clarified the real estate situation in 2019, stating it is not akin to the economic crisis of 1997.

"In the past 30 years, Thailand has experienced 2-3 major bubbles, the largest being from 1997 to 1999. The crisis from 1995 to 2008 was caused by a financial crisis, bank failures, currency devaluation, and high debt burdens. If these factors occur simultaneously, it signals a bubble burst."

When looking back at the real estate sector, signs of a crisis can be observed through six indicators:

1. When the housing market expands continuously, with increased construction for sale.

2. When supply exceeds demand, housing prices begin to fall.

3. As housing prices drop, interest rates rise, making it difficult for borrowers to keep up with payments.

4. This leads to accumulated debt exceeding the market value of homes.

5. People abandon their homes easily, causing a rapid increase in non-performing loans (NPL) for financial institutions.

6. As NPLs rise, banks tighten lending, making refinancing more difficult, which further increases NPLs.

Despite the downturn in the Thai real estate market, Assoc. Prof. Trairat concluded that it has not yet reached a crisis level. He emphasized the need to pay attention to the fact that by 2035, Thailand will be a fully aging society, with seniors making up nearly one-third of the population. Therefore, developers should focus on real estate for the elderly to meet future demands.

Assoc. Prof. Trairat Jarutatharn Lecturer at the Department of Housing, Faculty of Architecture, Chulalongkorn University

Ms. Sumitra Wongphakdee, Managing Director of Terra Media and Consulting Co., Ltd., discussed the survey results on the home-buying behavior of Thais in the 4.0 era and analyzed the behavior of Gen Y, a turning point in the real estate market.

"The home-buying behavior of Thais in the 4.0 era has changed significantly, with most people preferring to use digital media as a channel to research and gather information before making purchasing decisions." For the overall real estate market in 2019, it is expected to be in a downturn compared to previous periods, as operators need to adapt to the LTV measures and quickly adjust strategies to produce products that meet customer needs and prices that align with the current economic conditions. They must also prepare for new risks expected to arise in 2020, which will mark the beginning of challenges, especially with Thailand transitioning into an aging society, which will reduce the working-age population and potentially impact the Thai economy.

Additionally, data collected from an online survey of 402 respondents in Bangkok and its vicinity revealed that the Gen X group (ages 36-54) with incomes over 50,000 baht is particularly interesting, as 52% own more than two properties.

When examining the details, it was found that over 55% of the middle Gen Y group (ages 26-30) buy their first property for personal residence, while Gen X (ages 36-54) and Baby Boomers (over 54 years) tend to buy for investment and future asset purposes, accounting for 55%.

This data shows that individuals over 36 years old are planning their finances by investing in real estate, viewing it as a low-risk asset that can appreciate in value and be passed down to their children.

Ms. Sumitra Wongphakdee, Managing Director of Terra Media and Consulting Co., Ltd.

Group Talk: LTV and the Thai Economy

Hosted by Adirek Saengsaikaew, Secretary-General of the Thai Real Estate Association, and Angkanang Naimongkol, TNN News Anchor

Dr. Phisit Phuapan, Director of the Macroeconomic Policy Bureau, Fiscal Policy Office,

discussed the topic "Real Estate from a Fiscal Perspective" and summarized key points:

"In the past 10 years, the government has played a role during periods of slowdown in the real estate sector, implementing measures to support it. Looking at the broader picture over the years, the real estate sector today does not face significant issues, so assistance measures focus more on low-income groups."

- The structure of Thailand's economy relies heavily on exports for the past 25 years and is currently experiencing a slowdown.

- The production economy comes from the service sector, followed by industry and agriculture. However, labor statistics reflect a mismatch, as 8% of labor is in agriculture, contributing only 6.2% to GDP.

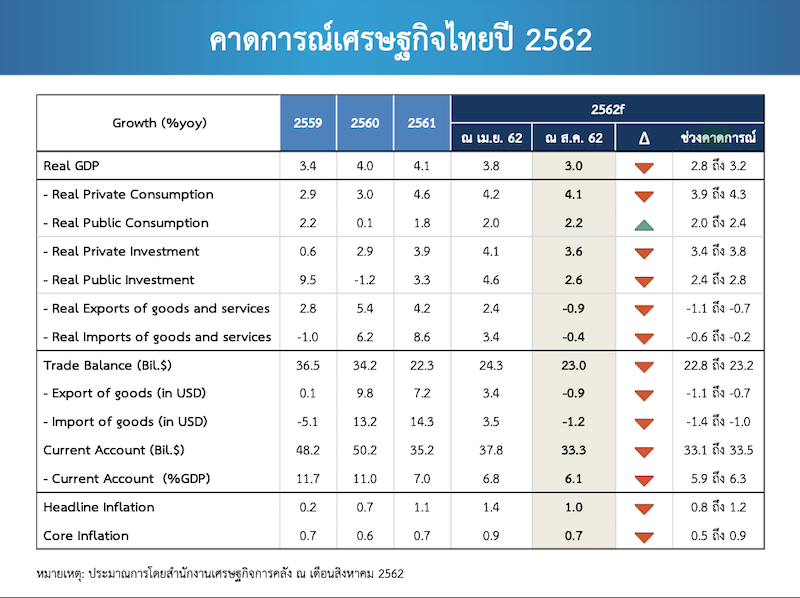

- Currently, Thailand's economy is growing at a rate of 2.3%, down from 2.8% in Q1 2019, primarily due to a slowdown in domestic demand and exports, following the global economic slowdown.

- While the service and trade sectors remain strong, the industrial sector is expected to slow down, aligning with domestic consumption.

- Exports have contracted by 2% since the beginning of the year (over the past seven months), which is not too severe compared to many countries worldwide. Conversely, the tourism sector has improved with an influx of tourists from Japan, India, Malaysia, and a return of Chinese tourists in July.

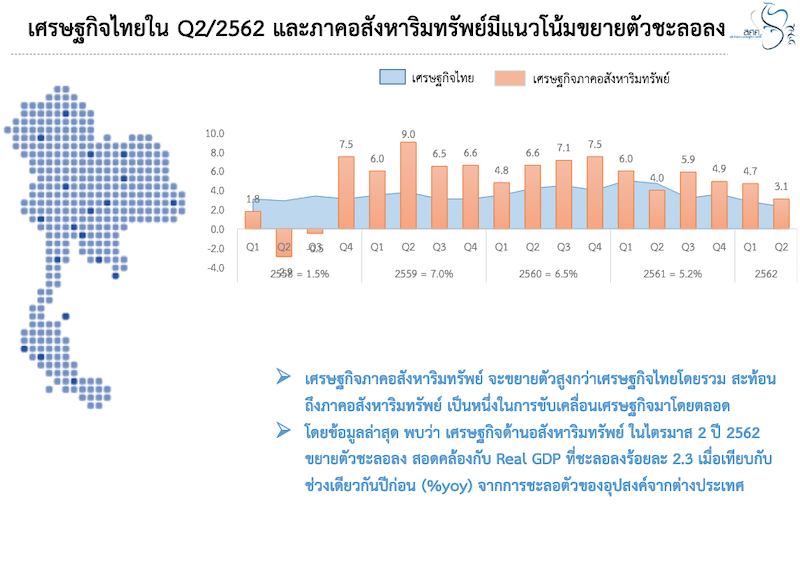

- The real estate economy is expected to grow faster than the overall Thai economy, reflecting its role as a driver of economic growth. Recent data shows that the real estate sector in Q2 2019 has slowed down, consistent with a 2.3% decline in Real GDP compared to the same period last year (%yoy), due to a slowdown in foreign demand.

- For the Thai economy in 2019, there are supportive factors to watch, including continuous global economic growth led by the US, China, and ASEAN economies, low-interest rates conducive to domestic consumption and investment, and increased public investment in major infrastructure projects, which will positively impact various economic activities. However, there are also risk factors that pose challenges, such as a decline in Chinese tourist arrivals and Russian tourists opting for Turkey, as well as US trade policies that may affect global economic and financial volatility, along with overall trade conditions.

Dr. Phisit Phuapan, Director of the Macroeconomic Policy Bureau, Fiscal Policy Office

Dr. Phisit Phuapan, Director of the Macroeconomic Policy Bureau, Fiscal Policy Office

Dr. Sakkapob Phanyanukul, Director of the Financial Stability Group, Bank of Thailand, highlighted the macroeconomic reasons for the LTV measures:

"The speculative situation in real estate with more than two contracts has increased from 14-15% five to six years ago to 22% at the end of last year. Our concern is that housing prices have risen by 6%, while the income of low-income individuals has not increased at the same rate. This disparity is a result of speculative buying driving up property prices due to both internal and external factors."

"The LTV measures were implemented to control speculation in the real estate sector, reduce speculation in the market for multiple contracts, and ensure the quality of loans in the long term. At the same time, we do not want to see households over-indebted, promoting financial discipline, and most importantly, we do not want to impact first-time homebuyers. It is noticeable that the measures are structured in a tiered manner."

From the latest figures, since the beginning of the year until July, the overall new loan disbursement has still grown by 13.3%, with a loan disbursement rate of 27.9% in Q1, driven by accelerated transfers and borrowing. However, after these measures took effect, new loan disbursement growth dropped to only 2.4% compared to the same period last year. Those affected are borrowers with two or more contracts. Looking at the overall figures from April to July, loan disbursement for single contracts in both low-rise and high-rise properties still grew by 11.8%. However, for second contracts, low-rise loans remained stagnant at 1.8%, a 30% decrease compared to the same period last year, which has understandably led to complaints from high-rise property developers.

This measure will lead to a decrease in condominium prices, allowing first-time homebuyers to access lower-priced homes. However, the government has listened to various parties and has relaxed these measures to allow joint borrowing. As a result, the latest figures show that 23% of loans are joint, with most joint borrowers being low-income individuals and first-time borrowers.

Dr. Phisit Phuapan, Director of the Macroeconomic Policy Bureau, Fiscal Policy Office

Mr. Surapol Opassethi, Managing Director of the National Credit Bureau, provided insights into the current debt situation of Thais in simple terms.

"Looking back to 1997, Thailand's NPL soared to 47.7%, but today it stands at 2-3%. The current household debt in Thailand is 12.9% of GDP, which translates to 16.48%. This means, simply put, if Thailand were a company with an annual income of 16.5 million baht, it would have a debt of 12.9 million baht per year, plus interest payments. The question is, is this company struggling? Because debt is growing faster than income."

Where does this debt come from? This debt has accumulated over time, starting from loans taken to repair homes after the 2011 floods, the first car scheme, the rice pledging scheme, and business loans, resulting in 28 million Thais being in debt, with 3 million in bad debt. It is noted that Thais over 30 years old are all in debt, and by the age of 55, they carry significant debt. It can be said that Thais are getting into debt faster, for longer, and in larger amounts compared to the past.

"The age group with the highest debt is between 35-50 years (midlife), with most debt being car installment debt. From the data, it can be observed that those who fail to secure home loans are often those who default on car payments and personal loans, while those who succeed are typically Gen Y individuals aged 22-29 with repayment capacities not exceeding 2-2.5 million baht." In summary, those facing borrowing issues primarily struggle with car payments.

Mr. Surapol Opassethi, Managing Director of the National Credit Bureau

After hearing the government's overview, let's turn to the opinions of the business sector, which is directly affected by these measures, and how they are adapting.

Mr. Pornariss Chuanchaisit, President of the Thai Real Estate Association

"We must admit that the Thai real estate sector is currently tight and sales are poor. From a developer's perspective, developing a project takes several years, and we can only hope that the situation improves by the time it is completed. If the government is concerned that low-income individuals will not have access to affordable housing, it should implement alternative measures."

"Another noteworthy aspect is that new cities will emerge and expand significantly in the future, and these cities will have potential that local people want to develop themselves. As a real estate developer, I believe that building cities will drive the economy and provide housing that low-income individuals can access."

Mr. Pornariss Chuanchaisit, President of the Thai Real Estate Association

Mr. Komkrit Hongdilokkul, Assistant Managing Director of the Condo Business Division at Pruksa Real Estate Public Company Limited, shared insights on the increasing business factors they must navigate.

"Looking back 12-14 years ago, 40% of condo buyers purchased out of necessity at different life stages, but now, the percentage has risen to 60%, indicating a greater need. Meanwhile, the cost of land near the BTS has skyrocketed from 400,000-500,000 baht to 1.2 million baht in just five years, even for locations 200 meters away from the station. It is evident that the rising cost of housing is driven by land costs, while buyers' purchasing power has not kept pace with the continually rising prices."

As a real estate developer, Komkrit agrees with the government's measures to promote financial discipline and household debt management, but he emphasizes that the government should address the issues correctly and effectively.

Mr. Komkrit Hongdilokkul, Assistant Managing Director of the Condo Business Division at Pruksa Real Estate Public Company Limited

All of these individuals are stakeholders, both from the policymakers and those affected by the LTV measures. Although there is no definitive conclusion yet, it is believed that this will lead to finding alternatives, solutions, and collaborations to drive the Thai economy effectively and sustainably.