5 Years of the Prayut Chan-o-cha Government and the Challenges Ahead as the Global Economy Declines Again

Prime Minister General Prayut Chan-o-cha announced that he would be able to form a new government in his second term under his own democratic framework, marking the longest government formation period, exceeding 100 days after the general election on March 24, 2019.

The key concern that many parties are worried about is the impact on the people's economy, particularly regarding the passage of the 2020 annual budget bill, which must be enacted by October 2019.

Recently, in the first meeting of the Monetary Policy Committee (MPC) of the Bank of Thailand (BOT), it was stated that they would monitor the new government's policies and public spending, as well as the progress of important infrastructure investments, which may affect the economic growth outlook in the future. It is anticipated that the 2020 budget bill will be enforceable in early 2020 or delayed by one quarter from the previous expectation that it could be enacted on time if the government could be formed by June 2019.

Additionally, the BOT has revised down its economic projections for all components of 2019, lowering GDP growth from 3.8% to 3.3%. Exports have been clearly affected by the trade war, thus revised down from 3% to 0%. The number of tourists has also been reduced from 40.4 million to 39.9 million, reflecting concerns and the severity of the trade war and risks from foreign sectors. Meanwhile, the government has reduced public investment growth from 6.1% to only 3.8%.

Thai Publica online news agency surveyed the economic performance of General Prayut's government over the past five years and the challenges ahead as the global economy is entering a downturn again.

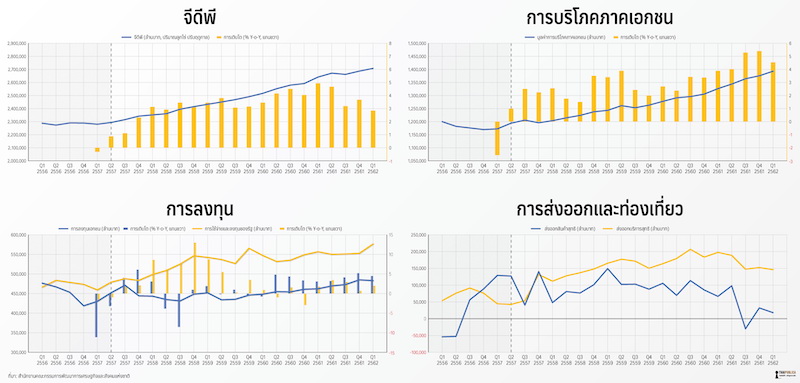

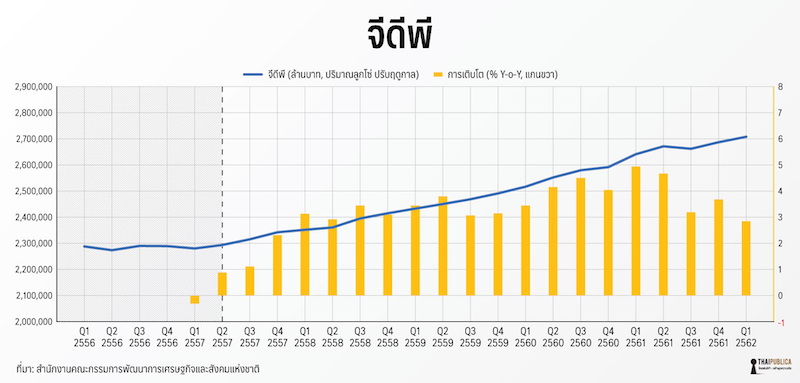

According to the National Economic and Social Development Council (NESDC), the seasonally adjusted real GDP produced in each quarter before the NCPO government took over the Thai economy from the first quarter of 2013 to the second quarter of 2014 averaged 2.29 trillion baht per quarter.

Thus, if we consider the first year (from the second quarter of 2014 to the second quarter of 2015) and the second year of the NCPO government's administration, the country's GDP increased to an average of 2.34 trillion baht per quarter and 2.42 trillion baht per quarter, respectively. In the following two years (from the second quarter of 2016 to the second quarter of 2018), it expanded dramatically to an average of 2.5 trillion baht per quarter and 2.6 trillion baht per quarter, respectively.

However, in the last year (from the second quarter of 2018 to the second quarter of 2019), GDP growth began to slow down significantly, although the average value was still 2.68 trillion baht per quarter.

This aligns with GDP growth, showing that in the first year of administration, the economy grew at an average of 2.36% per quarter, while in the second and third years, it gradually recovered to an average of 3.45% and 3.46%, respectively, before peaking in the fourth year at an average of 4.5% per quarter. In the final year, growth shrank to an average of only 3.21% per quarter.

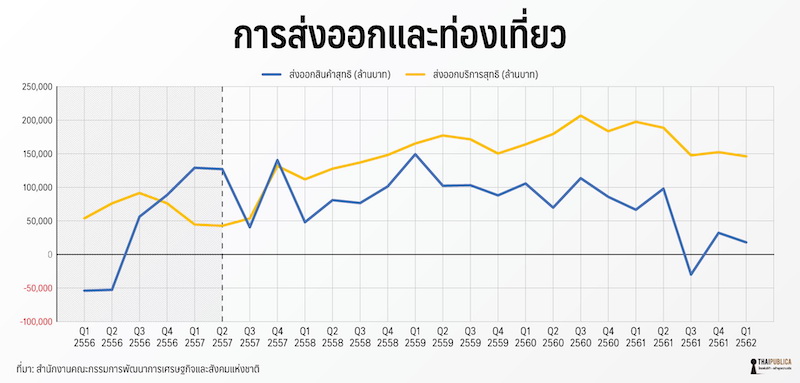

Delving into the components of GDP, it is evident that the Thai economy remains closely tied to foreign sectors. The GDP growth in the last two years aligns clearly with the expansion of the “export of goods and services,” with exports increasing from an average of 1.78 trillion baht per quarter before the NCPO government to an average of 1.80 trillion baht in the first year and 1.84 trillion baht in the second year, before rapidly increasing in line with the global economic situation in the third and fourth years to 1.89 trillion baht and 2.01 trillion baht, respectively. In the fifth year, growth slowed down significantly, maintaining an average export value of 2.03 trillion baht per quarter.

Furthermore, when separating exports into net goods exports and net service exports or tourism, excluding imports that represent the outflow of economic value to foreign countries, it is evident that tourism has been another crucial factor driving Thailand's GDP growth. Tourism has expanded rapidly and continuously over the past five years, while net goods exports remained sluggish in the first two years before recovering in the third and fourth years in line with the global economic situation. In the fifth year, not only did the goods export sector slow down rapidly, but the tourism sector reflected a similar trend, clearly impacting the overall Thai economy.

These economic figures contradict the strategies outlined in the annual budget bill of General Prayut's government, which emphasizes strengthening and sustaining the economy from within to enhance competitiveness and reduce dependence on foreign sectors, such as exports. However, over the past five years, data suggests that the economy has improved, but this recovery has been closely tied to the overall global economic situation. As the world returns to a period of slowdown, the internal Thai economy seems unprepared and weak to cope.

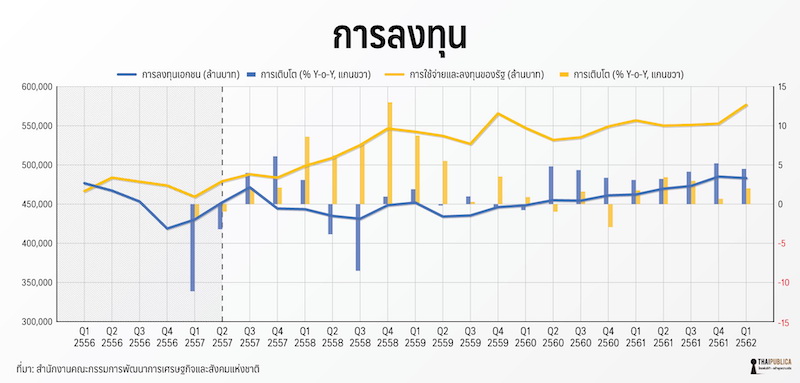

When we look back at what domestic economic factors have driven the Thai economy in the past, it is evident that “government spending and investment” have propped up the economy, aligning with the export sector's cycle that is also dependent on the global economy.

Government spending and investment from the previous period averaged 472.638 billion baht per quarter, increasing to 487.473 billion baht, 530.811 billion baht, and 544.201 billion baht in the first three years, respectively, before slightly slowing down in the fourth year to an average of 543.270 billion baht, as the economy grew relying on the benefits of the export sector and the recovering global economy. In the fifth year, government spending and investment increased to an average of 555.546 billion baht per quarter, clearly aligning with the slowdown of the global economy.

Similarly, the growth of government spending and investment grew rapidly in the first two years at an average of 14% per quarter, partly due to a very low base in the previous year, which experienced a political crisis. However, in the third and fourth years, growth slowed down but began to turn positive again in the final year.

Certainly, government spending and investment in economic terms usually aim to 1) restore confidence and investment from the private sector and 2) stimulate private consumption. Regarding “private investment,” which is considered a key factor for long-term growth, it initially contracted, and although it has shown signs of recovery, it has only recently returned to the investment levels seen before the NCPO government. Before the administration, private investment averaged 449.627 billion baht per quarter, before stabilizing or contracting in the first and second years to 452.870 billion baht and 441.665 billion baht, respectively, and gradually increasing to 441.077 billion baht and 458.218 billion baht in the third and fourth years.

In the fifth year, although private investment maintained momentum at an average of 477.731 billion baht per quarter, in the first quarter of 2019, private investment began to show signs of contraction compared to the previous quarter, marking the first contraction in six quarters. This may signal a slowdown from foreign sectors affecting demand for goods and private investment directly. Even if the government guides domestic investment, it is uncertain whether it can withstand this trend.

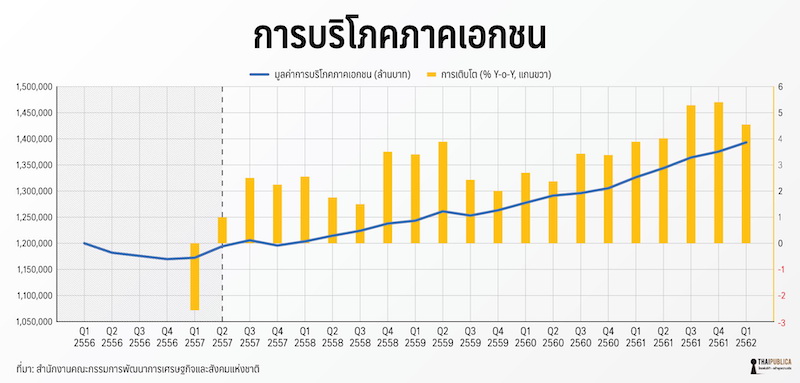

Finally, “private consumption” has been directly affected by economic stimulus measures in the second year and aligns with the economic stimulus through government spending and investment. However, as we entered the third year, when government spending began to wane, private consumption immediately slowed down. On the other hand, when the export sector recovered sufficiently, it transmitted benefits to consumption, allowing it to recover strongly in the fourth and fifth years. Nevertheless, similar to private investment, consumption began to show signs of contraction in the first quarter of 2019 as well.

Thus, the challenges ahead under the global trade war that significantly impacts Thailand are expected to result in Thai exports this year being at 0%.

Moreover, Thailand is facing limitations in fiscal policy or government spending and investment, which has been in deficit throughout the past five years, leading to an increase in the country's public debt. How long can this sustain the economy without building internal strength?

How will the “Prayut” government, which comes from an election, make Thailand prosperous and sustainable again?

SOURCE: www.thaipublica.org