Credit Bureau Does Not Mean Blacklist?

It is believed that many people still misunderstand and harbor fears that being listed in the Credit Bureau is a bad thing, indicating a poor credit history, which will make it difficult to apply for loans or conduct financial transactions. These beliefs may stem from a misinterpretation of the term "Credit Bureau." TerraBKK aims to clarify the basic information about the Credit Bureau and address common questions such as: What is a Credit Bureau? What is a blacklist? And if debts are paid, will the history be erased? The details are as follows.

Understanding What a Credit Bureau Is <\/span><\/strong><\/p>

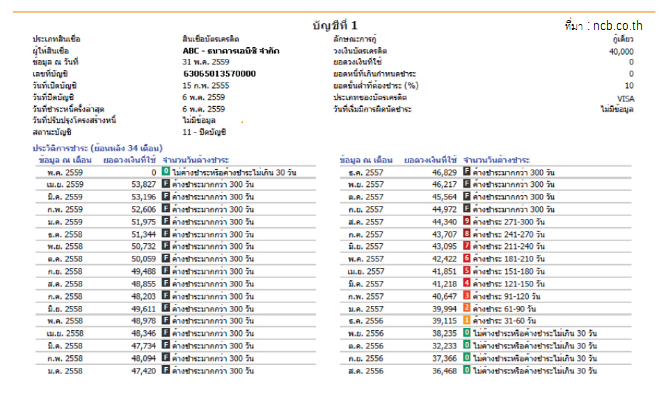

Credit Bureau<\/span> is a credit information company (Credit Bureau)<\/span><\/strong> that serves as a central repository for credit information, processed into a “Credit Report” from financial institutions that are members, such as commercial banks, state-owned specialized banks, leasing companies, credit card issuers, etc. The report displays factual information about the customer applying for the loan, such as basic customer information, approved loan details from financial institutions, and the customer’s loan repayment history. It does not include information about other assets, such as personal property or bank accounts. Accessing a credit report cannot occur without the consent of the data owner. This is why, when applying for a loan, banks require the borrower to sign a consent form allowing the credit information company to disclose their information. In summary, the Credit Bureau can disclose the credit history and repayment information of loan applicants, but it does not play a role in the loan approval decision. The information in the credit report is one of the factors considered by banks in their loan approval process. Credit Bureau Does Not Mean Blacklist? <\/span><\/strong><\/p>

Many people confuse the term “Credit Bureau” with “blacklist.” In reality, as soon as we apply for a loan or open a credit card with a member financial institution, our information is normally stored in the “Credit Bureau,” and our payment history is also recorded in the Credit Bureau. Therefore, whenever we fail to make timely payments, it will be referred to as being on the “blacklist.” Banks will use this information to consider loan approvals. In summary, the credit information company is not a central repository for blacklisted information but is responsible for collecting data on loan applications and repayments, whether they are good or bad. If Debts Are Paid, Will the History Be Erased? <\/span><\/strong><\/p>

Financial mistakes can happen. Therefore, if the incurred debt has been paid off, the information of individuals and legal entities, according to the law, is stipulated to be retained in the processing system for no more than 3 years from the date the member reports the information to the company. The credit report will reflect the actual results that occur and cannot alter the original history but will update information at the end of each month. This means that if we have previously defaulted, the information will show a "default" status for that month. Later, if we have paid off the debt, the new information will reflect a status of “paid” or “account closed.” The information will continue to be updated until the period stipulated by law, which is 3 years. Finally, for those who are afraid they won't be able to manage their debts and fear being blacklisted, it is recommended to negotiate with the bank for a debt restructuring first. If we can repay the debt under the new terms on time without any defaults, the bank will continue to report normally, and the credit information will reflect the repayment history accurately, as long as payments are not missed. The history will not be blacklisted, for sure. ---TerraBKK<\/strong> Article by: TerraBKK <\/span><\/strong> <\/p>

<\/p>

Investment Tips from TerraBKK: Find quality homes, value for money, and affordable prices.<\/strong>