Choosing the Right Investment: Creating a Financial Plan for Retirement

Currently, the demographic shift towards an “aging society”<\/strong><\/span> has become a significant issue that is being closely monitored and addressed globally. This shift impacts countries in various ways, such as a potential decrease in gross domestic product due to a declining workforce, per capita income, and government spending budgets for the elderly. Therefore, it is crucial for people today to be aware of this issue and prepare plans to cope with the changing social landscape in the future.<\/p>

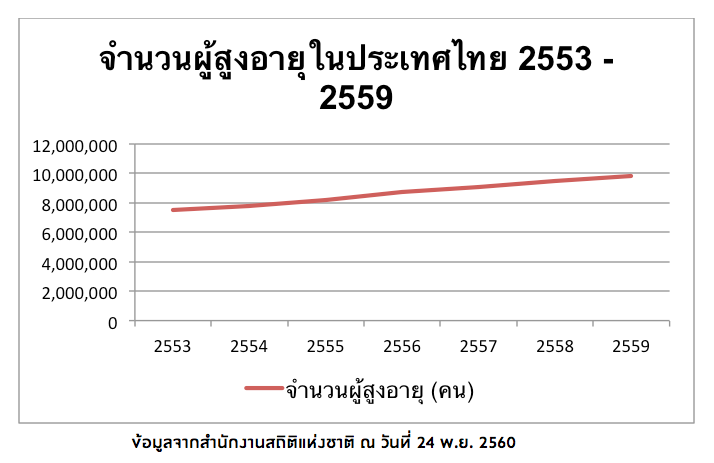

According to data from the National Statistical Office, the trend of the elderly population, or those aged 60 and above, is continuously increasing. Between 2010 and 2016, the number of elderly individuals rose by 3-4% annually, reaching nearly ten million by 2016.<\/p>

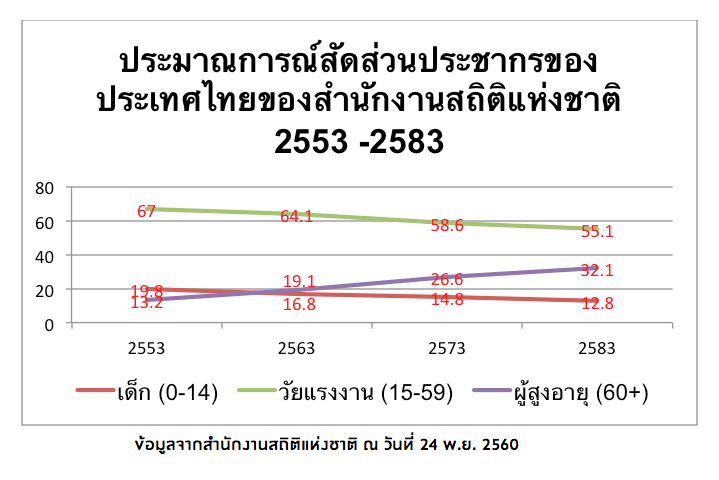

The National Statistical Office has analyzed the entire population data to identify trends in the structural changes of Thailand's population. The results indicate that in the next 10 to 20 years, Thailand is likely to transition into an aging society, with more than 20% of the population being elderly. Additionally, the number of children and working-age individuals is also expected to decline continuously.<\/p>

Financial planning is essential for working individuals to achieve their financial goals in life by the time they retire. It also helps those who will become elderly in the next 20 to 30 years adapt to the changing social and economic situations. A good financial plan consists of:<\/p>

Building Wealth<\/u><\/span><\/strong> – Savings planning, expense planning, debt management.<\/p>

Protecting Wealth<\/u><\/span><\/strong> – Insurance planning, retirement planning.<\/p>

Growing Wealth<\/u><\/span><\/strong> – Investment planning<\/strong>, tax planning.<\/p>

Transferring Wealth<\/u><\/span><\/strong> – Estate planning.<\/p>

The author emphasizes investment planning, as additional investments can help ensure our wealth throughout life. Even when facing uncertain economic conditions, investors should study which investment types align with their needs and financial status to generate returns that meet their financial objectives.<\/p>

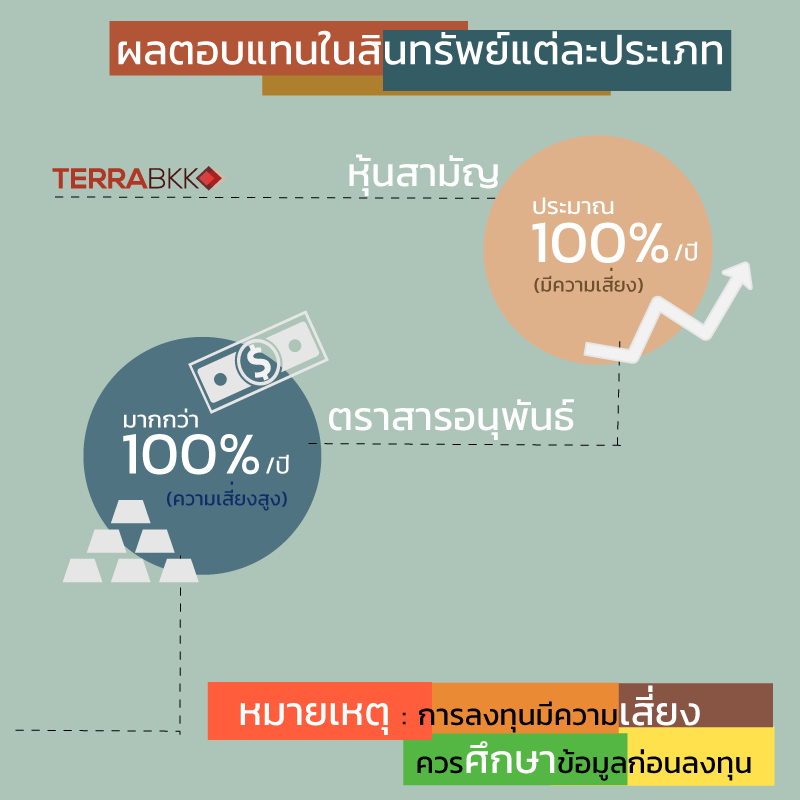

Returns from Different Asset Types<\/strong><\/span><\/p>

Different investment types yield varying returns, depending on the risk level of each asset. Low-risk assets provide lower returns, while higher-risk assets offer greater returns, following the financial principle of High Risk - High Return.<\/p>

Bank Deposits<\/strong><\/span><\/p>

<\/strong>Bank deposits are the most familiar investment form for the general public, as opening a deposit account is easy, with high liquidity for deposits and withdrawals, and the lowest investment risk. The returns from bank deposits come in the form of interest, which varies by deposit type and duration. Savings accounts, which allow for deposits and withdrawals at any time, typically have the lowest interest rates, currently at only 0.5% per year. In contrast, fixed deposits for 3 months, 6 months, 1 year, 2 years, or 3 years offer interest rates ranging from 0.9% to approximately 1.6% per year, which is relatively low compared to Thailand's inflation rate of 1.5 - 2% per year. Therefore, deposits are suitable for those who do not wish to take any risks, as they hardly create additional financial wealth for investors.<\/p>

Bonds<\/strong><\/span><\/p>

<\/strong>Bonds are assets that provide higher returns and carry more risk than bank deposits. The risk arises from the possibility of default by the borrower, whether it be the government, state enterprises, or private companies. Government-issued bonds are considered the lowest-risk assets within the bond category, while bonds issued by private companies carry the highest risk. The returns from bonds correlate with their risk level; the higher the risk of the issuing company, the higher the potential returns. Additionally, returns depend on whether the bonds are secured, subordinated, and their credit ratings. Higher-rated bonds are considered lower risk and thus offer lower interest rates, with government bonds yielding approximately 2% per year.<\/p>

Mutual Funds<\/strong><\/span><\/p>

<\/strong>Mutual funds come in various types, including those that invest solely in bonds, common stocks, or a mix of both in different proportions. Therefore, the returns from mutual funds vary based on asset type, investment proportions, and the fund manager's management capabilities. Over a period of 5 years or more, mutual funds with relatively good performance compared to all funds yield approximately 10 - 15% per year. Mutual funds are suitable for those who can tolerate a certain level of risk and seek clear financial growth.<\/p>

Common Stocks<\/strong><\/span><\/p>

<\/strong>Common stocks are assets that can yield relatively high returns in a short period, but they also come with significant risks. Investing in common stocks can generate returns from price appreciation of up to 100% or 200% per year if invested in the right company at the right time. This level of return is unattainable from low-risk financial assets like bank deposits or bonds. Additionally, there are opportunities for other returns, such as dividends. However, the risk level is also high, as losses can reach up to 100% due to price declines or risks associated with the invested company. Therefore, common stocks are suitable for those who can accept high risks and have the ability to research, understand, and monitor the performance of the invested companies and the economic situation.<\/p>

Derivatives<\/strong><\/span><\/p>

<\/strong>Investing in derivatives is considered the highest-risk investment, as it involves speculation on indices or commodity prices, such as rice, rubber, oil, gold, or stock indices. Originally, derivatives were designed to manage risks from price fluctuations for those holding commodities, such as farmers, shareholders, or gold holders, to hedge against future price volatility. However, with advancements in communication and financial technology, derivatives are now also used for speculative purposes. The returns from derivatives can occur much faster and at a higher magnitude than common stocks, but the risk is also significantly greater, as this investment type can lead to unlimited losses.<\/p>

Article by: TerraBKK Investment Tips <\/span><\/strong><\/p>

TerraBKK Find Good, Valuable, Affordable Homes<\/span><\/strong> <\/p>

<\/p>

Creating a Good Financial Plan<\/strong><\/span><\/p>

<\/strong><\/span><\/p>

<\/strong><\/span><\/p>

<\/strong><\/span><\/p>

<\/strong><\/span><\/p>

<\/p>