4 Ways to Refinance Your Home to Save Money

As we know, paying off a home loan consists of “principal repayment”<\/span><\/strong> and “interest payments”<\/span><\/strong>. Typically, home loans offer low interest rates during the first 1-3 years. After this promotional period ends, the monthly payments remain the same, but a larger portion goes towards interest payments, reducing the principal repayment. Many people seek to refinance their homes to secure attractive low interest rates similar to those they initially received.

However, it’s not just about the interest rates when choosing a refinancing option; other costs and conditions should also be considered. Let’s explore 4 ways to refinance your home to save money.

1. Avoid Refinancing Before 3 Years

<\/strong><\/span>

This is the first rule that home borrowers should remember. Otherwise, you may incur a penalty fee of up to 3% of the loan amount<\/span>, not the remaining principal. For example, if you borrowed 5 million baht to buy a house, the penalty would be approximately 150,000 baht, which is quite significant.

2. Compare Interest Rates<\/span>

Whether comparing home loans before and after the promotional interest period or refinancing options from different banks, there are two key points to consider:

- Type of interest rate, such as MLR<\/span> or MRR<\/span>, which typically averages between 6-8% depending on the bank's policy.

- The number after the minus sign<\/span>: The higher the number, the better.

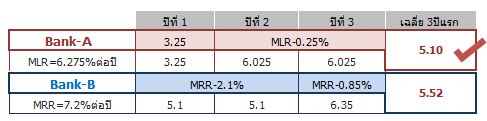

For example:

Bank-A offers an interest rate of 3.25% for the first year, then MLR-0.25%, with MLR=6.275% per year.

Bank-B offers MRR-2.1% for the first two years, then MLR-0.85%, with MRR=7.2% per year.

When considering the average interest rates for the first three years, Bank-A has an average rate of 5.10% per year, while Bank-B has an average rate of 5.52% per year. Although the difference is only 0.42% per year, for a high loan amount, such as 5 million baht, this results in a difference of about 21,000 baht per year, which is significant.

3. Refinancing with the Same Bank Can Reduce Costs<\/span>

Typically, refinancing costs average around 2-3% of the loan amount and can be as high as 4.3%. If you can refinance with the same bank, it can save you various fees, such as:

- Property appraisal fees<\/span>: Typically 0.25-2% of the asset value. If you refinance with the same bank, you may avoid this cost.

- New loan processing fees<\/span>: Most banks charge around 0-3% of the loan amount. Again, refinancing with the same bank may exempt you from this fee.

- Stamp duty: This is the same across all banks at 0.05% of the new loan amount.

- Mortgage registration fees: This is 1% of the loan amount and is a fee payable to the land department. If you refinance with the same bank, you won’t need to register a new mortgage, saving you this cost as well.

- Insurance fees or other service fees depending on the bank's conditions.

4. In Case of Refinancing Along with Personal Loans

Personal loans are not something to fear, but you must understand the purpose of this refinancing first.

- If you want to reduce interest payments: This indicates that you do not need additional personal loans, as personal loans typically have higher interest rates than housing loans and can unnecessarily increase your debt burden.

- If you need additional funds: If you have a necessity for cash, such as buying furniture or renovating your home, accepting a personal loan can be a good opportunity to use that money for your intended purpose.

All of this shows that refinancing a home is not out of reach for home buyers. As long as we understand and choose the right refinancing options, we can not only ease our debt burden but also save money from unnecessary expenses. For more information on housing loans, visit www.gsb.or.th<\/a><\/span>

Thank you for the information from  Follow more updates at www.gsb.or.th

Follow more updates at www.gsb.or.th